Case brief: CHEEK v. UNITED STATES Supreme Court of the United States 498 U.S. 192 (1991) Use the provided format. CASE BRIEFING FORMAT PROF. DOBSON

Case brief: CHEEK v. UNITED STATES Supreme Court of the United States 498 U.S. 192 (1991)

Use the provided format.

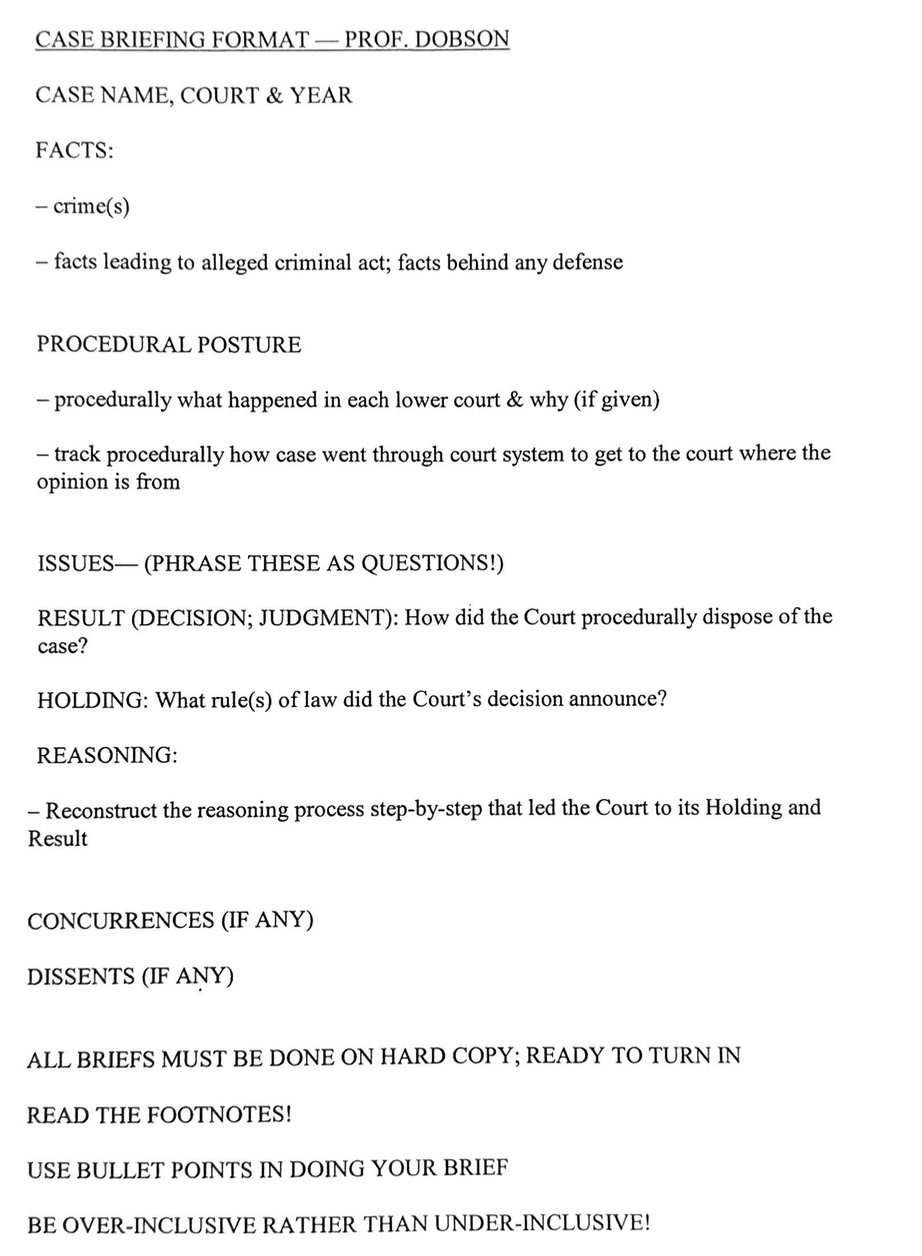

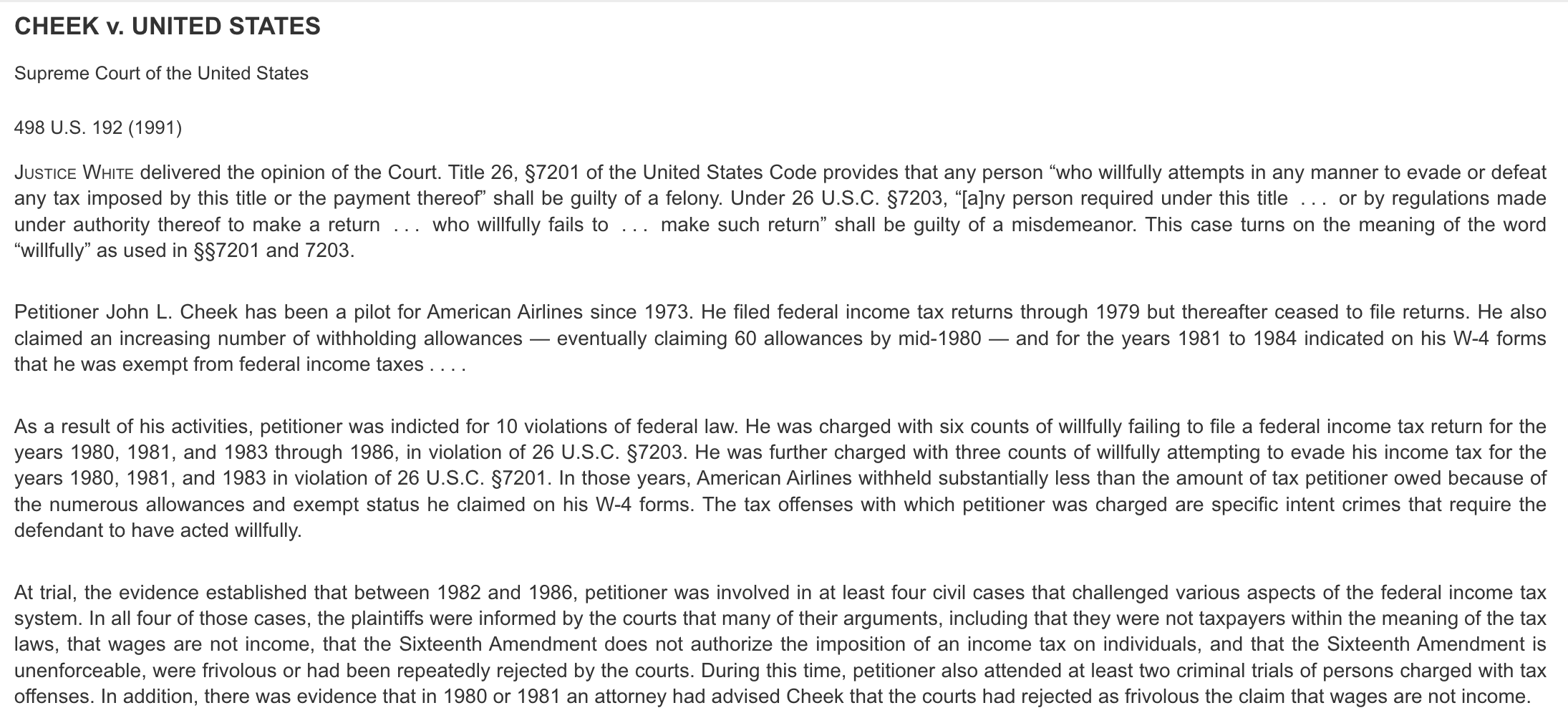

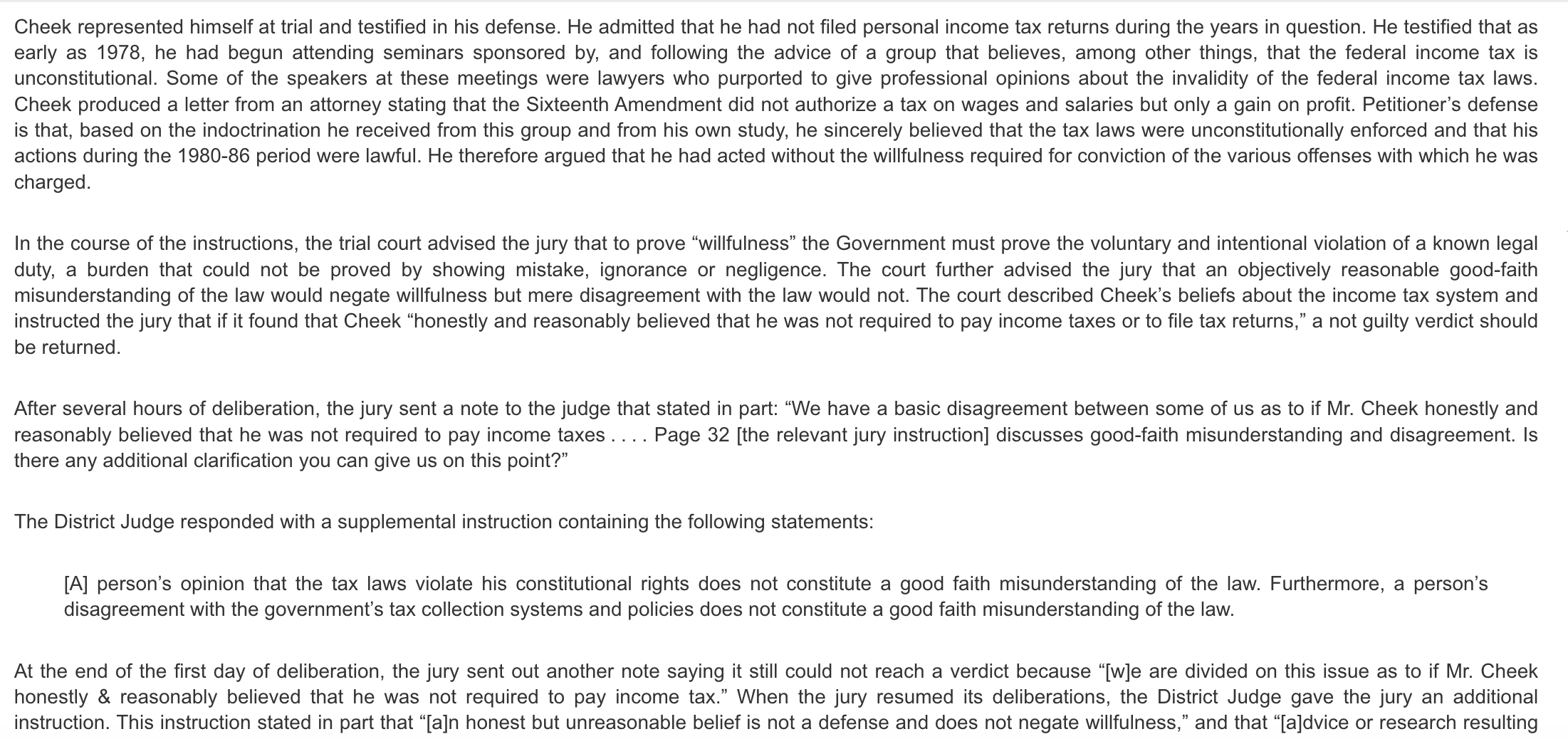

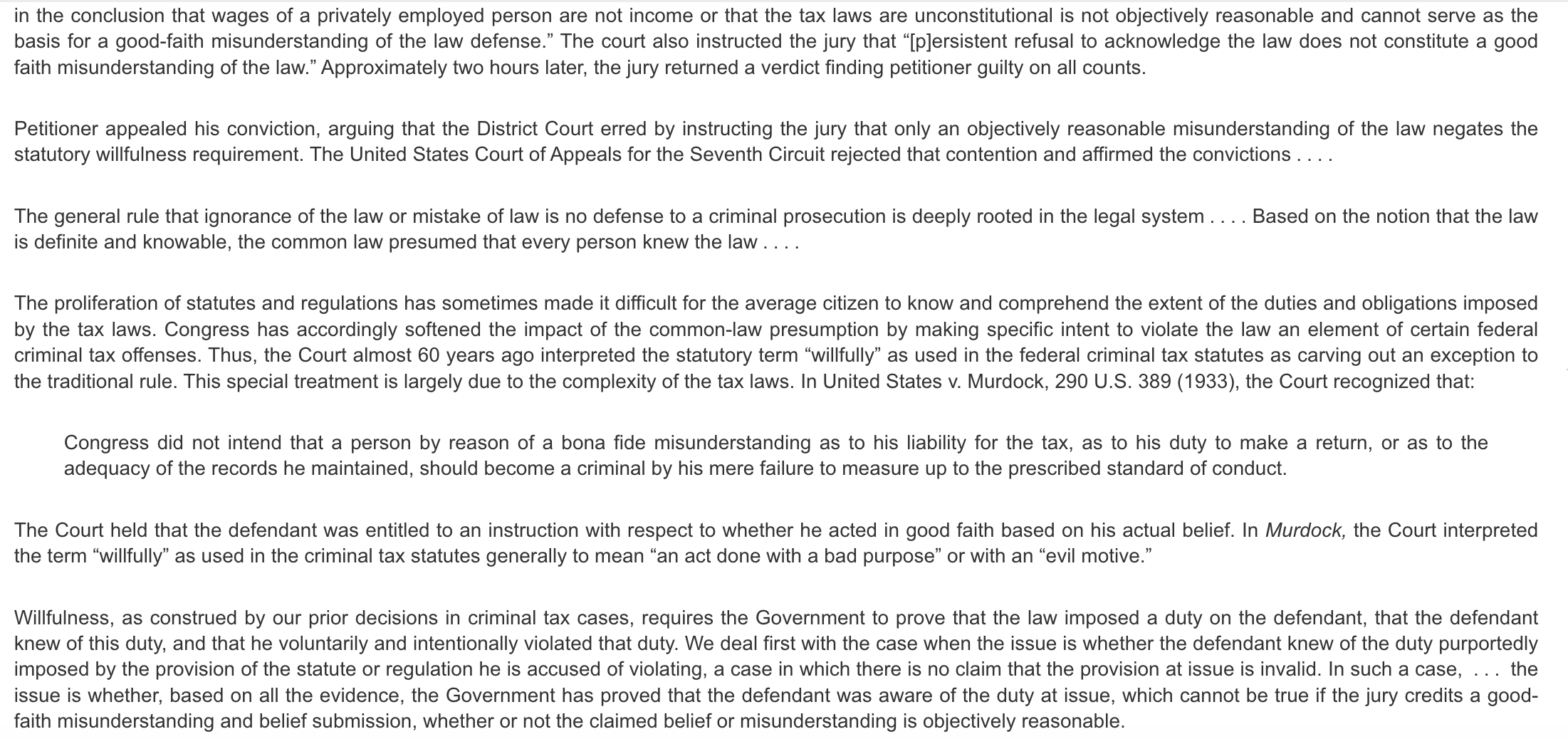

CASE BRIEFING FORMAT PROF. DOBSON CASE NAME, COURT & YEAR FACTS: crime(s) facts leading to alleged criminal act; facts behind any defense PROCEDURAL POSTURE procedurally what happened in each lower court & why (if given) track procedurally how case went through court system to get to the court where the opinion is from ISSUES (PHRASE THESE AS QUESTIONS!) RESULT (DECISION; JUDGMENT): How did the Court procedurally dispose of the case? HOLDING: What rule(s) of law did the Court's decision announce? REASONING: Reconstruct the reasoning process step-by-step that led the Court to its Holding and Result CONCURRENCES (IF ANY) DISSENTS (IF ANY) ALL BRIEFS MUST BE DONE ON HARD COPY; READY TO TURN IN READ THE FOOTNOTES! USE BULLET POINTS IN DOING YOUR BRIEF BE OVER-INCLUSIVE RATHER THAN UNDER-INCLUSIVE! CHEEK v. UNITED STATES Supreme Court of the United States 498 U.S. 192 (1991) JusTice WHITE delivered the opinion of the Court. Title 26, 7201 of the United States Code provides that any person \"who willfully attempts in any manner to evade or defeat any tax imposed by this title or the payment thereof\" shall be guilty of a felony. Under 26 U.S.C. 7203, \"[a]ny person required under this title ... or by regulations made under authority thereof to make a return ... who willfully fails to ... make such return\" shall be guilty of a misdemeanor. This case turns on the meaning of the word \"willfully\" as used in 7201 and 7203. Petitioner John L. Cheek has been a pilot for American Airlines since 1973. He filed federal income tax returns through 1979 but thereafter ceased to file returns. He also claimed an increasing number of withholding allowances eventually claiming 60 allowances by mid-1980 and for the years 1981 to 1984 indicated on his W-4 forms that he was exempt from federal income taxes . . .. As a result of his activities, petitioner was indicted for 10 violations of federal law. He was charged with six counts of willfully failing to file a federal income tax return for the years 1980, 1981, and 1983 through 1986, in violation of 26 U.S.C. 7203. He was further charged with three counts of willfully attempting to evade his income tax for the years 1980, 1981, and 1983 in violation of 26 U.S.C. 7201. In those years, American Airlines withheld substantially less than the amount of tax petitioner owed because of the numerous allowances and exempt status he claimed on his W-4 forms. The tax offenses with which petitioner was charged are specific intent crimes that require the defendant to have acted willfully. At trial, the evidence established that between 1982 and 1986, petitioner was involved in at least four civil cases that challenged various aspects of the federal income tax system. In all four of those cases, the plaintiffs were informed by the courts that many of their arguments, including that they were not taxpayers within the meaning of the tax laws, that wages are not income, that the Sixteenth Amendment does not authorize the imposition of an income tax on individuals, and that the Sixteenth Amendment is unenforceable, were frivolous or had been repeatedly rejected by the courts. During this time, petitioner also attended at least two criminal trials of persons charged with tax offenses. In addition, there was evidence that in 1980 or 1981 an attorney had advised Cheek that the courts had rejected as frivolous the claim that wages are not income. Cheek represented himself at trial and testified in his defense. He admitted that he had not filed personal income tax returns during the years in question. He testified that as early as 1978, he had begun attending seminars sponsored by, and following the advice of a group that believes, among other things, that the federal income tax is unconstitutional. Some of the speakers at these meetings were lawyers who purported to give professional opinions about the invalidity of the federal income tax laws. Cheek produced a letter from an attorney stating that the Sixteenth Amendment did not authorize a tax on wages and salaries but only a gain on profit. Petitioner's defense is that, based on the indoctrination he received from this group and from his own study, he sincerely believed that the tax laws were unconstitutionally enforced and that his actions during the 1980-86 period were lawful. He therefore argued that he had acted without the willfulness required for conviction of the various offenses with which he was charged. In the course of the instructions, the trial court advised the jury that to prove \"willfulness\" the Government must prove the voluntary and intentional violation of a known legal duty, a burden that could not be proved by showing mistake, ignorance or negligence. The court further advised the jury that an objectively reasonable good-faith misunderstanding of the law would negate willfulness but mere disagreement with the law would not. The court described Cheek's beliefs about the income tax system and instructed the jury that if it found that Cheek \"honestly and reasonably believed that he was not required to pay income taxes or to file tax returns,\" a not guilty verdict should be returned. After several hours of deliberation, the jury sent a note to the judge that stated in part: \"We have a basic disagreement between some of us as to if Mr. Cheek honestly and reasonably believed that he was not required to pay income taxes . ... Page 32 [the relevant jury instruction] discusses good-faith misunderstanding and disagreement. Is there any additional clarification you can give us on this point?\" The District Judge responded with a supplemental instruction containing the following statements: [A] person's opinion that the tax laws violate his constitutional rights does not constitute a good faith misunderstanding of the law. Furthermore, a person's disagreement with the government's tax collection systems and policies does not constitute a good faith misunderstanding of the law. At the end of the first day of deliberation, the jury sent out another note saying it still could not reach a verdict because \"[w]e are divided on this issue as to if Mr. Cheek honestly & reasonably believed that he was not required to pay income tax.\" When the jury resumed its deliberations, the District Judge gave the jury an additional instruction. This instruction stated in part that \"[a]n honest but unreasonable belief is not a defense and does not negate willfulness,\" and that \"[a]dvice or research resulting in the conclusion that wages of a privately employed person are not income or that the tax laws are unconstitutional is not objectively reasonable and cannot serve as the basis for a good-faith misunderstanding of the law defense.\" The court also instructed the jury that \"[p]ersistent refusal to acknowledge the law does not constitute a good faith misunderstanding of the law.\" Approximately two hours later, the jury returned a verdict finding petitioner guilty on all counts. Petitioner appealed his conviction, arguing that the District Court erred by instructing the jury that only an objectively reasonable misunderstanding of the law negates the statutory willfulness requirement. The United States Court of Appeals for the Seventh Circuit rejected that contention and affirmed the convictions . . . . The general rule that ignorance of the law or mistake of law is no defense to a criminal prosecution is deeply rooted in the legal system . . .. Based on the notion that the law is definite and knowable, the common law presumed that every person knew the law . . . . The proliferation of statutes and regulations has sometimes made it difficult for the average citizen to know and comprehend the extent of the duties and obligations imposed by the tax laws. Congress has accordingly softened the impact of the common-law presumption by making specific intent to violate the law an element of certain federal criminal tax offenses. Thus, the Court almost 60 years ago interpreted the statutory term \"willfully\" as used in the federal criminal tax statutes as carving out an exception to the traditional rule. This special treatment is largely due to the complexity of the tax laws. In United States v. Murdock, 290 U.S. 389 (1933), the Court recognized that: Congress did not intend that a person by reason of a bona fide misunderstanding as to his liability for the tax, as to his duty to make a return, or as to the adequacy of the records he maintained, should become a criminal by his mere failure to measure up to the prescribed standard of conduct. The Court held that the defendant was entitled to an instruction with respect to whether he acted in good faith based on his actual belief. In Murdock, the Court interpreted the term \"willfully\" as used in the criminal tax statutes generally to mean \"an act done with a bad purpose\" or with an \"evil motive.\" Willfulness, as construed by our prior decisions in criminal tax cases, requires the Government to prove that the law imposed a duty on the defendant, that the defendant knew of this duty, and that he voluntarily and intentionally violated that duty. We deal first with the case when the issue is whether the defendant knew of the duty purportedly imposed by the provision of the statute or regulation he is accused of violating, a case in which there is no claim that the provision at issue is invalid. In such a case, ... the issue is whether, based on all the evidence, the Government has proved that the defendant was aware of the duty at issue, which cannot be true if the jury credits a good- faith misunderstanding and belief submission, whether or not the claimed belief or misunderstanding is objectively reasonable. In this case, It Cheek asserted that he truly believed that the Internal Revenue Code did not purport to treat wages as income, and the jury believed him, the Government would not have carried its burden to prove willfulness, however unreasonable a court might deem such a belief . . . . We thus disagree with the Court of Appeals' requirement that a claimed good-faith belief must be objectively reasonable if it is to be considered as possibly negating the Government''s evidence purporting to show a defendant's awareness of the legal duty atissue. . .. Cheek asserted in the trial court that he should be acquitted because he believed in good faith that the income tax law is unconstitutional as applied to him and thus could not impose any legal duty upon him of which he should have been aware . . .. [Some cases have] construed the willfulness requirement in the criminal provisions of the Internal Revenue Code to require proof of knowledge of the law. This was because in \"our complex tax system, uncertainty often arises even among taxpayers who earnestly wish to follow the law\" and \"[i]t is not the purpose of the law to penalize frank difference of opinion or innocent errors made despite the exercise of reasonable care,\" United States v. Bishop, 412 U.S. 346. Claims that some of the provisions of the tax code are unconstitutional are of a different order. They do not arise from innocent mistakes caused by the complexity of the Internal Revenue Code. Rather, they reveal full knowledge of the provisions at issue and a studied conclusion, however wrong, that those provisions are invalid and unenforceable . . . . We do not believe that Congress contemplated that such a taxpayer, without risking criminal prosecution, could ignore the duties imposed on him by the Internal Revenue Code and refuse to utilize the mechanisms provided by Congress to present his claims of invalidity to the courts and to abide by their decisions. There is no doubt that Cheek, from year to year, was free to pay the tax that the law purported to require, file for a refund, and if denied, present his claims of invalidity, constitutional or otherwise, to the courts. Also, without paying the tax, he could have challenged claims of tax deficiencies to the Tax Court, with the right to appeal to a higher court if unsuccessful. Cheek took neither course in some years, and when he did he was unwilling to accept the outcome. As we see it, he is in no position to claim that his good-faith belief about the validity of the Internal Revenue Code negates willfulness or provides a defense to criminal prosecution under 7201 and 7203 . . . . We thus hold that in a case like this, a defendant's views about the validity of the tax statutes are irrelevant to the issue of willfulness, need not be heard by the jury, and if they are, an instruction to disregard them would be proper. For this purpose, it makes no difference whether the claims of invalidity are frivolous or have substance. It was therefore not error in this case for the District Judge to instruct the jury not to consider Cheek's claims that the tax laws were unconstitutional. However, it was error for the court to instruct the jury that petitioner's asserted beliefs that wages are not income and that he was not a taxpayer within the meaning of the Internal Revenue Code should not be considered by the jury in determining whether Cheek had acted willfully. [Case remanded.]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance