Answered step by step

Verified Expert Solution

Question

1 Approved Answer

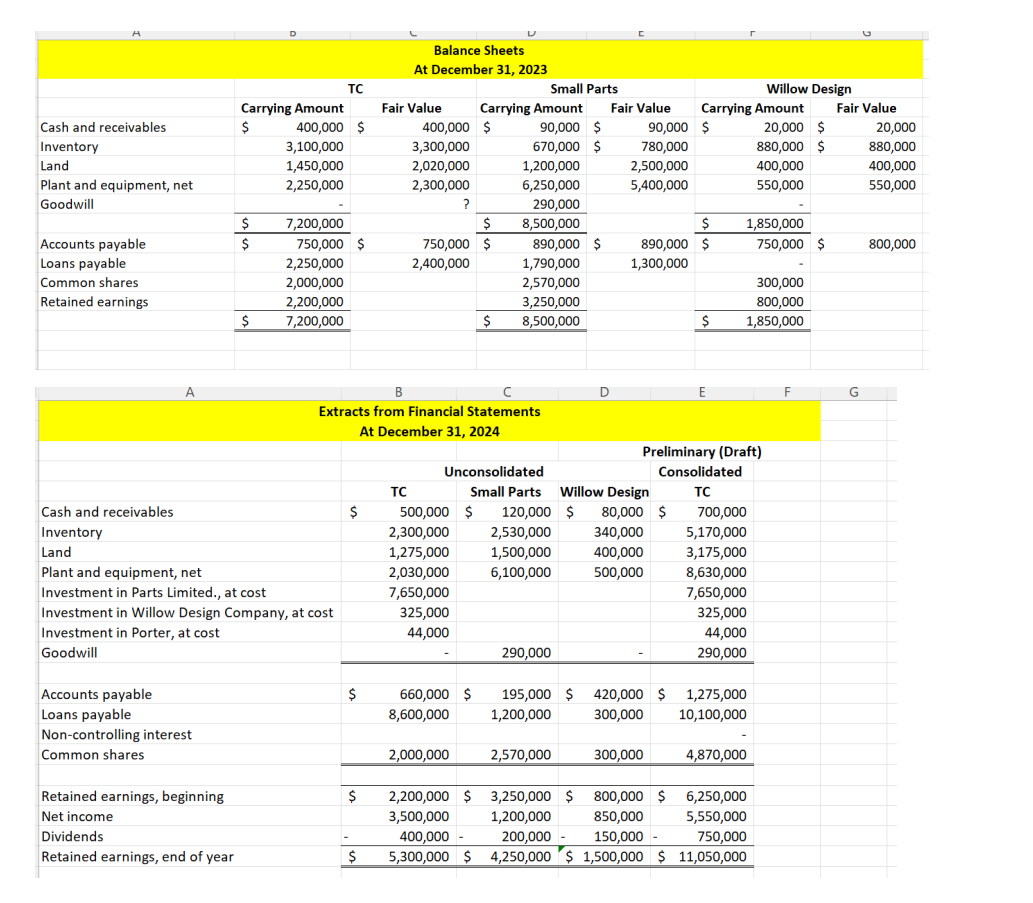

Case Facts: Background TC prepared its 2 0 2 3 financial statements in accordance with ASPE but now requires that its 2 0 2 4

Case Facts:

Background

TC prepared its financial statements in accordance with ASPE but now requires that its financial statements be prepared pursuant to IFRS in anticipation of going public.

TC is planning to engage in foreign currency transactions in What effect, if any, will these transactions have on TCs financial statements?

I really appreciate the time and effort needed to prepare this memo and the huge impact your decisions will have on our future as a public company. Please do not hold back on your analysis or comments. The detail is absolutely needed for us to understand the accounting requirements under IFRS and how they differ from ASPE.

Additional Facts Provided by Elizabeth Turner mother bookkeeper:

Elizabeth said to you if my memory serves me correctly, you need to add together the financial statements of any equity investments that TC controls or has significant influence over. My financial accounting instructor said consolidated financial statements are required for public companies but not private companies. I could be wrong though. Also, I have no idea how to account for the shares we did not acquire in Small Parts. Someone mentioned noncontrolling interest so I included it on the preliminary consolidated financial statement but that is as far as I got. This was not covered in the financial accounting courses I took.

On January TC acquired in separate transactions an controlling interest in Small Parts Limited Small Parts a interest in Willow Design Company Willow Design and shares of Zed Corporation Zed

With the exception of Zed, the companies are involved with product manufacturing or design for luxury trailers. These investments create the necessary synergies for TCs operations.

TC financed the acquisition of the voting common shares of Small Parts with a bank loan. The Small Parts shares were trading for $ in the few days prior to the acquisition and a few days after the acquisition; however, to gain control of Small Parts, TC also paid a premium of $ per share. The total amount paid was $

TC acquired the shares of Zed for $ as a shortterm, nonstrategic investment with the expectation that the shares would be sold at some point in the future depending on market conditions.

TC acquired the voting common shares interest in Willow Design for a cash payment of $

On June TC acquired all of the net assets of Princess Trailers Ltd for a cash payment of $ Princess Trailers had been operating a retail RV sales business and the owneroperator retired. This transaction has not yet been recorded. The valuators determined the plant and equipment had a remaining useful life of years on this date. The details of the acquisition are as follows:

Total cash paid $

Carrying valueNBV Fair value

Land $ $

Inventory

Plant and equipment

On December the shares of Small Parts, Willow Design and Zed were trading at $ $ and $ per share, respectively.

When TC acquired Small Parts, the plant and equipment had a remaining useful life of years and the note payable matured on December

On June TC loaned Willow Design $ at an annual interest rate of $ The amount of the loan and interest remains unpaid on December

During Willow Design sold $ of inventory to TC This inventory originally cost Willow Design, $ The majority of the inventory acquired from Willow Design was used by TC for the luxury trailers which were sold in The remaining inventory amounted to as at December

On December TC sold equipment to Small Parts for $ On the date of sale, the equipment had a net book value of $ and a remaining useful life of years.

A goodwill impairment test in for the goodwill acquired in the Small Parts acquisition amounted to $

TC Small Parts, and Willow Design pay income tax at the rate of

REQUIRED:

Based on the information provided in the case, prepare a detailed memo for the shareholders of TC Corporation. The following should be included in the comments:

A detailed explanation of the importantsignificant financial accounting issues of TC Small Parts, Willow Design, and the nonstrategic investment in Zed. Provide a detailed explanation of the optionsalternatives available for the reporting of the investments, your recommendations based on the information that is available to you and the necessary IFRS reporting requirements to support your decision or recommendation. In some cases, you will need to explain the available alternatives with a recommendation. The shareholders will need this detailed explanation to decide whether the recommendation you have made is acceptable. Note: The shareholders ar

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Forest Management Auditing

Authors: Lucio Brotto

1st Edition

0367605872, 978-0367605872