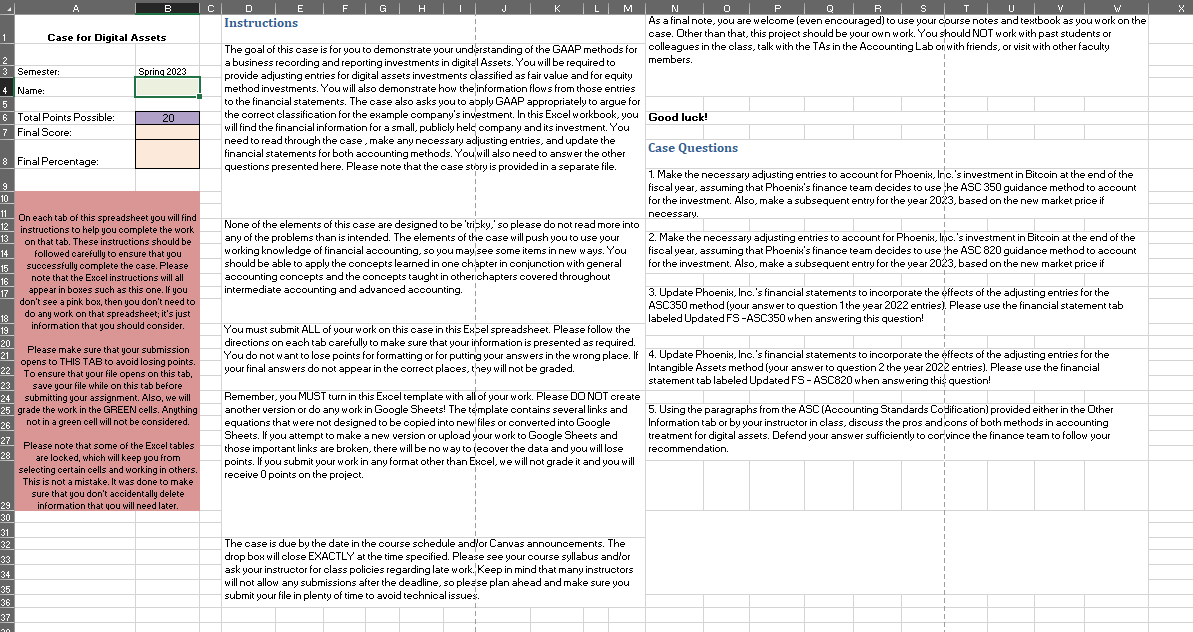

Case for Digital Assets Semester: 5 rln 2023 Name: I II Total Points Possible: 20 FinalScore- Final Percentage: On each tab of this spreadsheet you

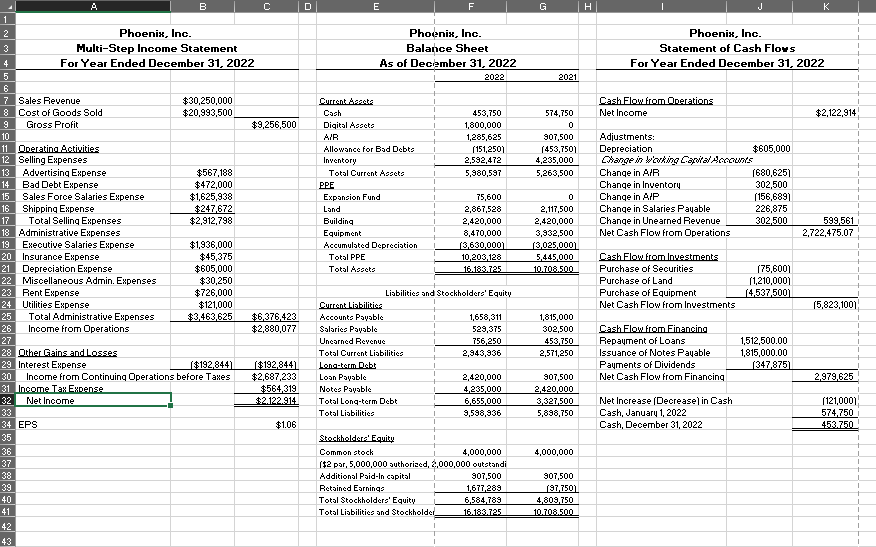

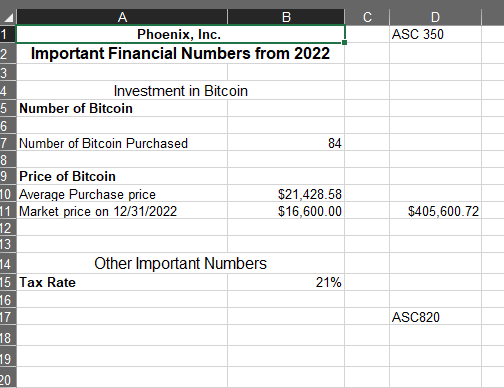

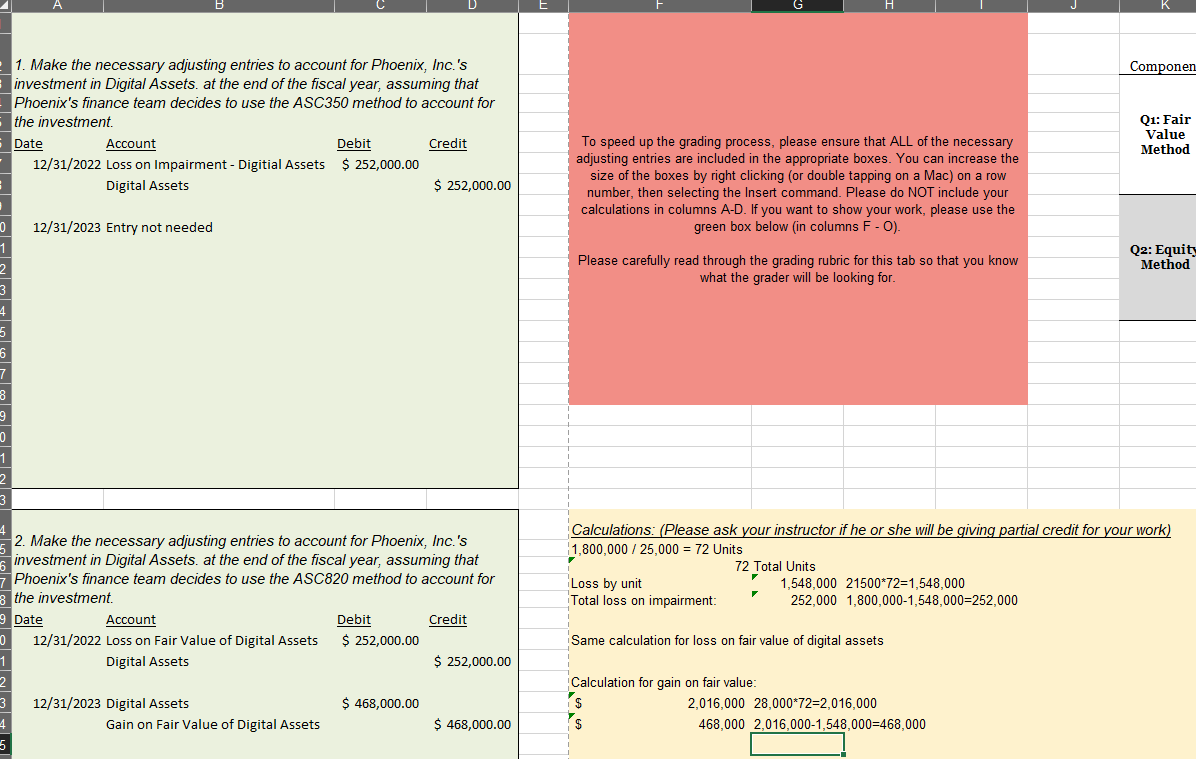

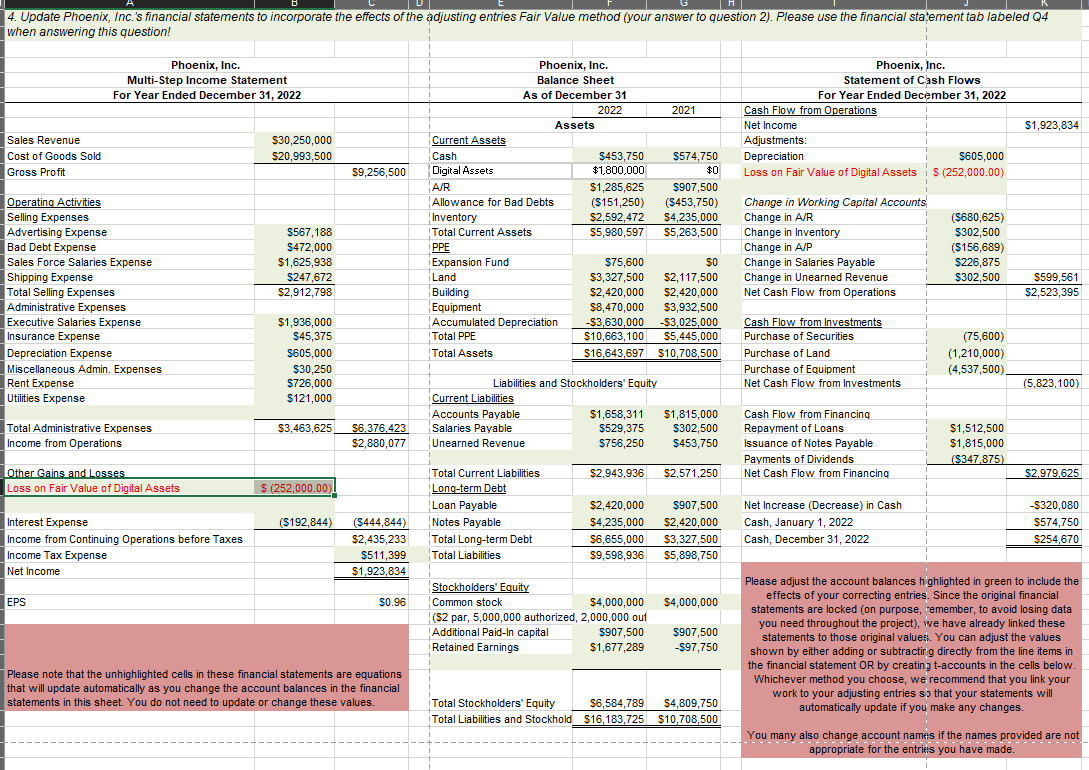

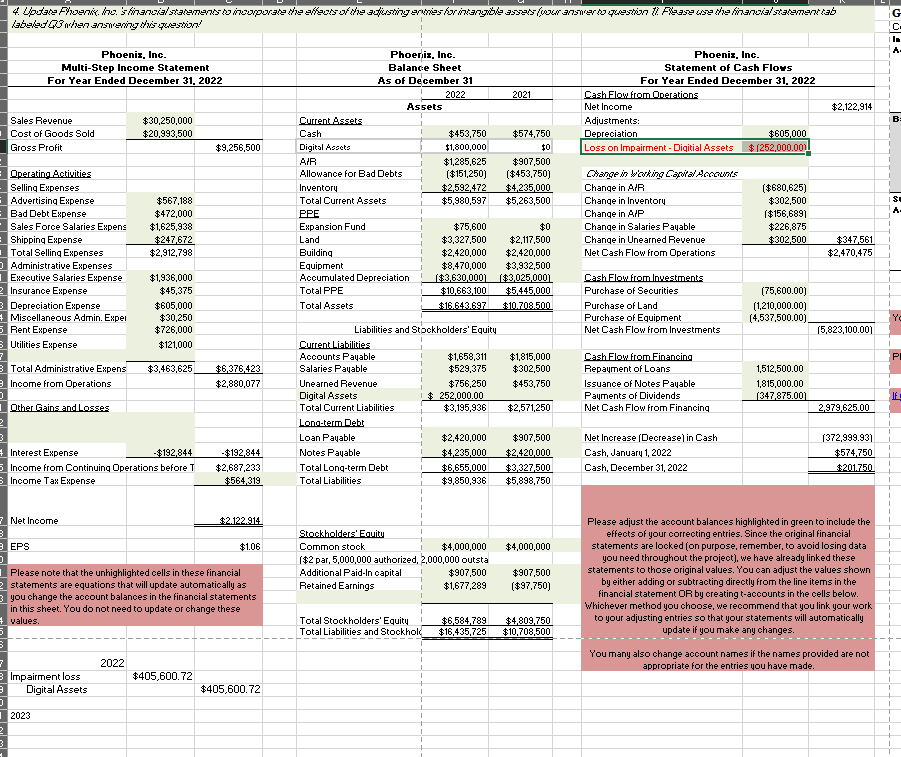

Case for Digital Assets Semester: 5 rln 2023 Name: I II Total Points Possible: 20 FinalScore- Final Percentage: On each tab of this spreadsheet you will find instructions to help you complete the work on that tab. These instructions should be followed carefully to ensure that you successfully complete the case. Please note that the Excel instructions will all appear in boxes such as this one. If you don't see a pink box. then you don't need to do any work on that spreadsheet: it's iust information that you should consider. Please make sure that your submission opens to THIS TAB to avoid losing points. To ensure that your file opens on this tab. save your file while on this tab before submitting your assignment Also, we will grade the work in the GREEN cells. Anything not in a green cell will not be considered Please note that some of the Excel tables are locked. which will keep you from selecting certain cells and working in others. This is not a mistake. It was done to make sure that you don't accidentally delete information that you will need later. Instr ucrrons The goal of this case is for you to demonstrate your understanding of the GAAP methods for a business recording and reporting investments in digital Assets. You will be required to provide adiusting entries for digital assets investments classified as fair value and for equity method investments. You will also demonstrate how the information flows from those entries to the financial statements. The case also asks you to aziply GAAP appropriately to argue for the correct classification for the example company's investment. ln this Excel workbook. you will find the financial information for a small, publicly helc company and its investment. You need to read through the case , make any necessary acliusting entries, and update the financial statements for both accounting methods. You will also need to answer the other questions presented here. Please note that the case story is prouided in a separate file. None of the elements of this case are designed to be 'tri:ky,' so please do not read more into any of the problems than is intended. The elements of the case will push you to use your working knowledge of financial accounting, so you may see some items in new ways. You should be able to apply the concepts learned in one chapter in coniunctlon with general accounting concepts and the concepts taught in other chapters covered throughout intermediate accounting and advanced accounting. You must submit ALL of your work on this case in this Excel spreadsheet. Please follow the directions on each tab carefully to make sure that your information is presented as required You do not want to lose points for formatting or for putting your answers in the wrong place. lf your final answers do not appear in the correct places, t'iey will not be graded. Remember, you MUST turn in this Excel template with all of your work. Please DD NUT create another version or do any work in Google Sheets! The template contains several links and equations that were not designed to be copied into new files or converted into Google Sheets. If you attempt to make a new version or upload your work to Google Sheets and those important links are broken, there will be no way to recover the data and you will lose points. If you submit your work in any format other than Excel, we will not grade it and you will receive 0 points on the proiect. The case is due by the date in the course schedule andr'or Canvas announcements. The drop box will close EXACTLY at the time specified. Please see your course syllabus andr'or ask your instructor for class policies regarding late work. Keep in mind that many instructors will not allow any submissions aiter the deadline, so please plan ahead and make sure you submit your file in plenty of time to avoid technical issues: As a f al note, you are welcome [even encouraged] to use your course notes and textbook as you work on the case. Other than that, this proiect should be your own work You should NOT work with past students or colleagues in the class, talk with the TAs in the Accounting Lab or with friends, or visit with other faculty members. Good luck! Case Questions 1. Make the necessary adiusting entries to account for Phoenix, lr c.'s investment in Bitcoin at the end of the fiscal year, assuming that Phoenix's finance team decides to use :he ASE 350 guidance method to account for the investment. Also, make a subsequent entry for the year 2023, based on the new market price if necessary. 2. Make the necessary adiusting entries to account for Phoenix, |nc.'s investment in Bltcoln at the end of the fiscal year, assuming that Phoenix's finance team decides to use :he ASE 820 guidance method to account for the investment. Also, make a subsequent entry for the year 2023, based on the new market price if 3. Update Phoenix, |nc.'s financial statements to incorporate the effects of the adiusting entries for the ASCSSU method [your answer to question 1 the year 2022 entries]. Please use the financial statement tab labeled Updated F5 ASC350 when answering this question! 4. Update Phoenix, |nc.'s linancial statements to incorporate the effects of the adiusting entries for the Intangible Assets method [your answer to question 2 the year 2022 entries]. Please use the financial statement tab labeled Updated FS ASCSZD when answering this: question! 5. Using the paragraphs from the ASC [Accounting Standards Codification] provided either in the Other Information tab or by your instructor in class, discuss the pros and cons of both methods in accounting treatment for digital assets. Defend your answer sufficiently to cor vince the finance team to follow your recommendation. A B C E F G H K Phoenix, Inc. Phoenix, Inc. Phoenix, Inc. 3 Multi-Step Income Statement Balance Sheet Statement of Cash Flows For Year Ended December 31, 2022 As of December 31, 2022 For Year Ended December 31. 2022 2022 2021 7 Sales Revenue $30,250,000 Current Agents Cash Flow from Operations 8 Cost of Goods Sold $20,993,500 Cash 453,750 574,750 Net Income $2,122,914 9 Gross Profit $9,256,500 Digital Assets 1,800,000 AIR 1,285,625 307,500 Adjustments: 11 Operating Activities Allowance for Bad Debts (151,250) (453,750) Depreciation $605,000 12 Selling Expenses Inventory 2,592,472 4,235,000 13 Advertising Expense $567,188 Total Current Assets 5,380,597 5,263,500 Change in A/F (680,625) 14 Bad Debt Expense $472,000 PPE Change in Inventory 302,500 15 Sales Force Salaries Expense $1,625,938 Expansion Fund 75,600 Change in A/F (156,689 16 Shipping Expense $247.672 Land 2,867,528 2,117,500 Change in Salaries Payable 226,875 Total Selling Expenses $2,912,798 Building 2,420,000 2,420,000 Change in Unearned Revenue 302,500 599,561 Administrative Expenses Equipment 8,470,000 3,932,500 Net Cash Flow from Operations 2,722,475.07 19 Executive Salaries Expense $1,936,000 Accumulated Depreciation (3,630,000) (3,025,000] 20 Insurance Expense $45,375 Total PPE 10 203 128 5,445,000 Cash Flow from Investments Depreciation Expense $605,000 Total Assets 16.183.725 10.708.500 Purchase of Securities (75,600) Miscellaneous Admin. Expenses $30,250 Purchase of Land [1,210,000 Rent Expense $726,000 Liabilities and Stockholders' Equity Purchase of Equipment [4,537,500) Utilities Expense $121,000 Current Liabilities Net Cash Flow from Investments (5,823,1001 25 Total Administrative Expenses $3.463.625 $6,376,423 Accounts Payable 1,658,311 1,815,000 26 Income from Operations $2,880,077 Salaries Payable 529,375 302,500 Cash Flow from Financing 27 Unearned Revenue 156,250 153,750 Repayment of Loans 1,512,500.00 28 [Other Gains and Losses Total Current Liabilities 2,343,936 2,571,250 Issuance of Notes Payable 1,815,000.00 29 Interest Expense ($192,8441 $192,8441 Long-term Debt Payments of Dividends 1347,875 30 Income from Continuing Operations before Takes $2,687,233 Loan Payable 2,420,000 907,500 Net Cash Flow from Financing 2,979,625 31 Income Tax Expense $564,319 Notes Payable 1 235,000 2,420,000 32 Net Income $2.122.914 Total Long-term Debt 5655,000 3,327,500 Net Increase [ Decrease] in Cash [121,000) 33 Total Liabilities 3,596,936 ,898,750 Cash, January 1, 2022 574,750 34 EPS $1.06 Cash, December 31, 2022 53.750 35 Stockholders' Equity 36 Common stock 4,000,000 4,000,000 37 ($2 par, 5,000,000 authorized, 2,000,000 outstand 38 Additional Paid-In capital 907,500 307,500 39 Retained Earnings 1,677,283 (87,7501 40 Total Stockholders' Equity 5 584,789 4,809 750 41 Total Liabilities and Stockholder_ 16.183.125 10.708.500 42 43A B C D Phoenix, Inc. ASC 350 2 Important Financial Numbers from 2022 + Investment in Bitcoin 5 Number of Bitcoin 6 7 Number of Bitcoin Purchased 84 8 9 Price of Bitcoin 10 Average Purchase price $21,428.58 1 Market price on 12/31/2022 $16,600.00 $405,600.72 12 13 14 Other Important Numbers 5 Tax Rate 21% 6 17 ASC820 18 201. Make the necessary adjusting entries to account for Phoenix, Inc.'s Compone investment in Digital Assets. at the end of the fiscal year, assuming that Phoenix's finance team decides to use the ASC350 method to account for the investment. Q1: Fair Value Date Account Debit Credit To speed up the grading process, please ensure that ALL of the necessary Method 12/31/2022 Loss on Impairment - Digitial Assets $ 252,000.00 adjusting entries are included in the appropriate boxes. You can increase the Digital Assets $ 252,000.00 size of the boxes by right clicking (or double tapping on a Mac) on a row number, then selecting the Insert command. Please do NOT include your calculations in columns A-D. If you want to show your work, please use the 12/31/2023 Entry not needed green box below (in columns F - O). Q2: Equit Please carefully read through the grading rubric for this tab so that you know Method what the grader will be looking for. Calculations: (Please ask your instructor if he or she will be giving partial credit for your work) 2. Make the necessary adjusting entries to account for Phoenix, Inc.'s 1,800,000 / 25,000 = 72 Units investment in Digital Assets. at the end of the fiscal year, assuming that 72 Total Units Phoenix's finance team decides to use the ASC820 method to account for Loss by unit 1,548,000 21500*72=1,548,000 the investment. Total loss on impairment: 252,000 1,800,000-1,548,000=252,000 Date Account Debit Credit 12/31/2022 Loss on Fair Value of Digital Assets $ 252,000.00 Same calculation for loss on fair value of digital assets Digital Assets $ 252,000.00 Calculation for gain on fair value: 12/31/2023 Digital Assets $ 468,000.00 2,016,000 28,000*72=2,016,000 Gain on Fair Value of Digital Assets $ 468,000.00 468,000 2,016,000-1,548,000=468,000Discuss the pros and cons of using ASC350 based on your two years' entries. Discuss pros and cons of using .480 820 based on your two year's entries 4. Update Phoenix, Inc.'s financial statements to incorporate the effects of the adjusting entries Fair Value method (your answer to question 2). Please use the financial statement tab labeled Q4 when answering this question! Phoenix, Inc. Phoenix, Inc. Phoenix, Inc. Multi-Step Income Statement Balance Sheet Statement of Cash Flows For Year Ended December 31, 2022 As of December 31 For Year Ended December 31, 2022 2022 2021 Cash Flow from Operation Assets Net Income $1,923,834 Sales Revenue $30,250,000 Current Assets Adjustments: Cost of Goods Sold $20,993,500 Cash $453,750 $574,750 Depreciation $605,000 Gross Profi 59,256,500 Digital Assets $1,800,000 Loss on Fair Value of Digital Assets $ (252,000.00) A/R $1,285,625 $907,500 Operating Activities Allowance for Bad Debts ($151,250) ($453,750) Change in Working Capital Accounts Selling Expenses Inventory $2,592,472 $4,235,000 Change in A/R (5680,625) Advertising Expense $567, 188 Total Current Assets $5,980,597 $5,263,500 Change in Inventory $302,500 Bad Debt Expense $472,000 PPE Change in A/P ($156,689) Sales Force Salaries Expense $1,625,938 Expansion Fund $75,600 SO Change in Salaries Payable $226,875 Shipping Expense $247,672 Land $3,327,500 52,117,500 Change in Unearned Revenue $302.500 $599,561 Total Selling Expenses $2,912,798 Building $2,420,000 $2,420,000 Net Cash Flow from Operations $2,523,395 Administrative Expenses Equipment $8,470,000 53,932,500 Executive Salaries Expense $1,936,000 Accumulated Depreciation -$3,630,000 $3,025,000 Cash Flow from Investments Insurance Expense $45,375 Total PPE $10,663, 100 $5,445,000 Purchase of Securities (75,600) Depreciation Expense $605,000 Total Assets $16,643,697 $10,708,500 Purchase of Land (1,210,000) Miscellaneous Admin. Expenses $30,250 Purchase of Equipment (4,537,500 Rent Expense $726,000 Liabilities and Stockholders' Equity Net Cash Flow from Investments (5,823,100) Utilities Expense $121,000 Current Liabilities Accounts Payable 51,658,311 $1,815,000 Cash Flow from Financing Total Administrative Ex $3,463,625 56,376,423 Salaries Payable $529,375 $302,500 Repayment of Loans $1,512,500 Income from Operations $2,880,077 Unearned Revenue $756,250 $453,750 Issuance of Notes Payable $1,815,000 Payments of Dividends ($347.875) Other Gains and Losses Total Current Liabilities 52,943,936 52,571,250 Net Cash Flow from Financing $2,979.625 Loss on Fair Value of Digital Assets $ (252,000.00) Long-term Debt Loan Payable $2,420,000 5907,500 Net Increase (Decrease) in Cash $320,080 Interest Expense ($192,844) (5444,844) Notes Payable $4,235,000 $2,420,000 Cash, January 1, 2022 $574,750 Income from Continuing Operations before Taxes 52,435,233 Total Long-term Debt $6,655,000 $3,327,500 Cash, December 31, 2022 $254,670 Income Tax Expense $511,399 Total Liabilities 59,598,936 $5,898,750 Net Income $1,923,834 Stockholders Equity Please adjust the account balances highlighted in green to include the EPS $0.96 Common stock $4,000,000 $4,000,000 effects of your correcting entries. Since the original financial statements are locked (on purpose, remember, to avoid losing data ($2 par, 5,000,000 authorized, 2,000,000 out you need throughout the project), we have already linked these Additional Paid-In capital $907,500 $907,500 statements to those original values. You can adjust the values Retained Earnings $1,677,289 -$97,750 shown by either adding or subtracting directly from the line items in the financial statement OR by creating t-accounts in the cells below Please note that the unhighlighted cells in these financial statements are equations Whichever method you choose, we recommend that you link your that will update automatically as you change the account balances in the financial work to your adjusting entries so that your statements will statements in this sheet. You do not need to update or change these values. Total Stockholders' Equity $6,584,789 $4,809,750 automatically update if you make any changes. Total Liabilities and Stockhold $16,183,725 $10,708,500 You many also change account names if the names provided are not appropriate for the entries you have made.4. Update Phoeni. The. Shandra/statements to incorporate the effects of the existing entes forintangible assets (your answerto question 1/ Rease use the financial statement135 labeled 43 when answering this question' Phoenix, Inc. Phoenix, Inc. Phoenix, Inc. Multi-Step Income Statement Balance Sheet Statement of Cash Flows For Year Ended December 31. 2022 As of December 31 For Year Ended December 31. 2022 2022 2021 Cash Flow from Operations Assets Net Income $2,122.914 Sales Revenue $30,250,000 Current Assets Adjustments: Cost of Goods Sold $20,993,500 Cast $453,750 $574,750 Depreciation $605,000 Gross Prof $9,256,500 Digital Assets $1,800,000 Loss on Impairment - Digitial Assets |$ (252,000.00) A/R $1,285.625 $907 500 Operating Activities Allowance for Bad Debts ($151,250) [$453,750 Change in Working Capital Accounts Selling Expenses Inventory $2,592472 $4,235,000 Change in A/R $680,625) Advertising Expense $567,188 tal Current Assets $5,980,597 $5,263,500 Change in Inventory $302,500 Bad Debt Expense $472,000 PPE Change in A/F ($ 156,6891 Sales Force Salaries Expens $1,625,938 Expansion Fund $75,600 $O Change in Salaries Payable $226,875 Shipping Expense $247,672 Land $3,327,500 $2,117,50 Change in Unearned Revenue $302,500 $347,561 Total Selling Expenses $2,912,798 Building $2,420,000 $2.420,000 Net Cash Flow from Operations $2,470,475 Administrative Expenses Equipment $8,470,000 $3,932,500 Executive Salaries Expense $1,936,000 Accumulated Depreciation $3,630,000 [$3,025,000] Cash Flow from Investments Insurance Expense $45,375 Total PPE $10.663,100 $5,445,000 Purchase of Securities (75,600.00) Depreciation Expense $605,000 Total Assets $16 643.697 $10.708.500 Purchase of Land (1,210,000.00) Miscellaneous Admin. Expel $30,250 Purchase of Equipment (4,537,500.00) Rent Expens $726,000 Liabilities and Stockholders' Equity Net Cash Flow from Investments (5,823,100.00) Utilities Expense $121,000 Current Liabilities Accounts Payable $1,658,31 $1,815,000 Cash Flow from Financing Total Administrative Expens $3,463,625 $6,376,423 Salaries Payable $529,375 $302.500 Repayment of Loans 1,512,500.00 Income from Operations $2,880,077 Unearned Revenue $756,250 $453.750 Issuance of Notes Payable 1,815,000.00 Digital Assets $252,000.0 Payments of Dividend (347,875.00 Other Gains and Losses Total Current Liabilities $3,195,936 $2,571,250 Net Cash Flow from Financing 2,979.625.00 Long-term Deb Loan Payable $2,420,000 $907.500 Net Increase (Decrease) in Cash (372,999.931 Interest Expense -$192,844 -$192,844 Notes Payable $4,235,000 2,420,000 Cash, January 1, 2022 574,750 Income from Continuing Operations before T $2,687,233 Total Long-term Debt 6 655,000 $3,327,500 Cash, December 31, 2022 $201750 Income Tax Expense $564,319 Total Liabilities $9,850,936 $5,898,750 Net Income $2 122.914 Please adjust the account balances highlighted in green to include the Stockholders Equity effects of your correcting entries. Since the original financial EPS $1.06 Common stock $4,000,000 $4,000,000 statements are locked (on purpose, remember, to avoid losing data ($2 par, 5,000,000 authorized, 2,000,000 outsta you need throughout the project), we have already linked these Please note that the unhighlighted cells in these financial Additional Paid-In capital $907,500 $907,500 statements to those original values. You can adjust the values shown statements are equations that will update automatically as Retained Earnings $1,677,28 [$97.750) by either adding or subtracting directly from the line items in the you change the account balances in the financial statements inancial statement OR by creating t-accounts in the cells below in this sheet. You do not need to update or change these Whichever method you choose, we recommend that you link your work values. Total Stockholders' Equity $6,584,789 $4,809,750 to your adjusting entries so that your statements will automatically Total Liabilities and Stockholm $16,435,725 $10.708,500 update if you make any changes. You many also change account names if the names provided are not 2022 appropriate for the entries you have made Impairment loss $405,600.72 Digital Assets $405,600. 72 2023Determining How to Treat Digital Assets: The case of Pheonix, Inc. Background Pheonix, Inc. is an IT services company specializing in providing IT solutions to its clients. While headquartered in the Texas U.S., they do business globally, providing analytical programs to various industries, including education, healthcare, government, etc. Overall, the company has been very successful, especially within the U.S. Besides being successful in its industry, the CEO of Pheonix, Inc. is also expanding its business to cryptocurrencies. Starting in 2022, Phoenix, Inc started to acquire Bitcoin from the market for a total of 1,800.000 dollars for multiple purchases with an average cost per Bitcoin of $25,000. However, the market of cryptocurrencies went south during the year 2022. By the end of 2022, the Bitcoin price was down to $21,500. By the end of 2023, the Bitcoin price was up to $28,000. Pheonix, Inc.'s accounting team has held a meeting to discuss how to report its company's investment in digital assets. Digital assets are a relatively new phenomenon, and accounting rules for recording transactions regarding cryptocurrencies are not well interpreted. Thus, the meeting was heated with some debate on how to report such assets in its 2022 financial reports. Generally, two main opinions exist on how to report cryptocurrencies in its annual report. One is to report as intangible assets by following the ASC 350, and the other opinion is to report as marketable securities by following the ASC 820. Case Questions 1. Make the necessary adjusting entries to account for Pheonix, Inc.'s investment in Bitcoin at the end of the fiscal year 2022, assuming that Pheonix's finance team decides to use the ASC 350 method to account for the investment. Also, make subsequent entries for the year-end of 2023 if necessary. 2. Make the necessary adjusting entries to account for Pheonix, Inc.'s investment in Bitcoin at the end of the fiscal year 2022, assuming that Pheonix's finance team decides to use the ASC 820 method to account for the investment. Also, make subsequent entries for the year-end of 2023 if necessary. 3. Update Pheonix, Inc.'s financial statements to incorporate the effects of the adjusting entries for the ASC 350 method only based on 2022. 4. Update Pheonix, Inc.'s financial statements to incorporate the effects of the adjusting entries for the ASC 350 method only based on 2022. 5. Write a page of essay to explain the benefits of using the two methods for reporting purposes. Also, conduct some research on current and future proposal US GAAP updates

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance