CASE STUDY Kooistra Autogroep When he took over as CEO of the Kooistra Autogroep in dealership, one Suzuki dealership, one Saab dealer- 2002, Tom Kooistra

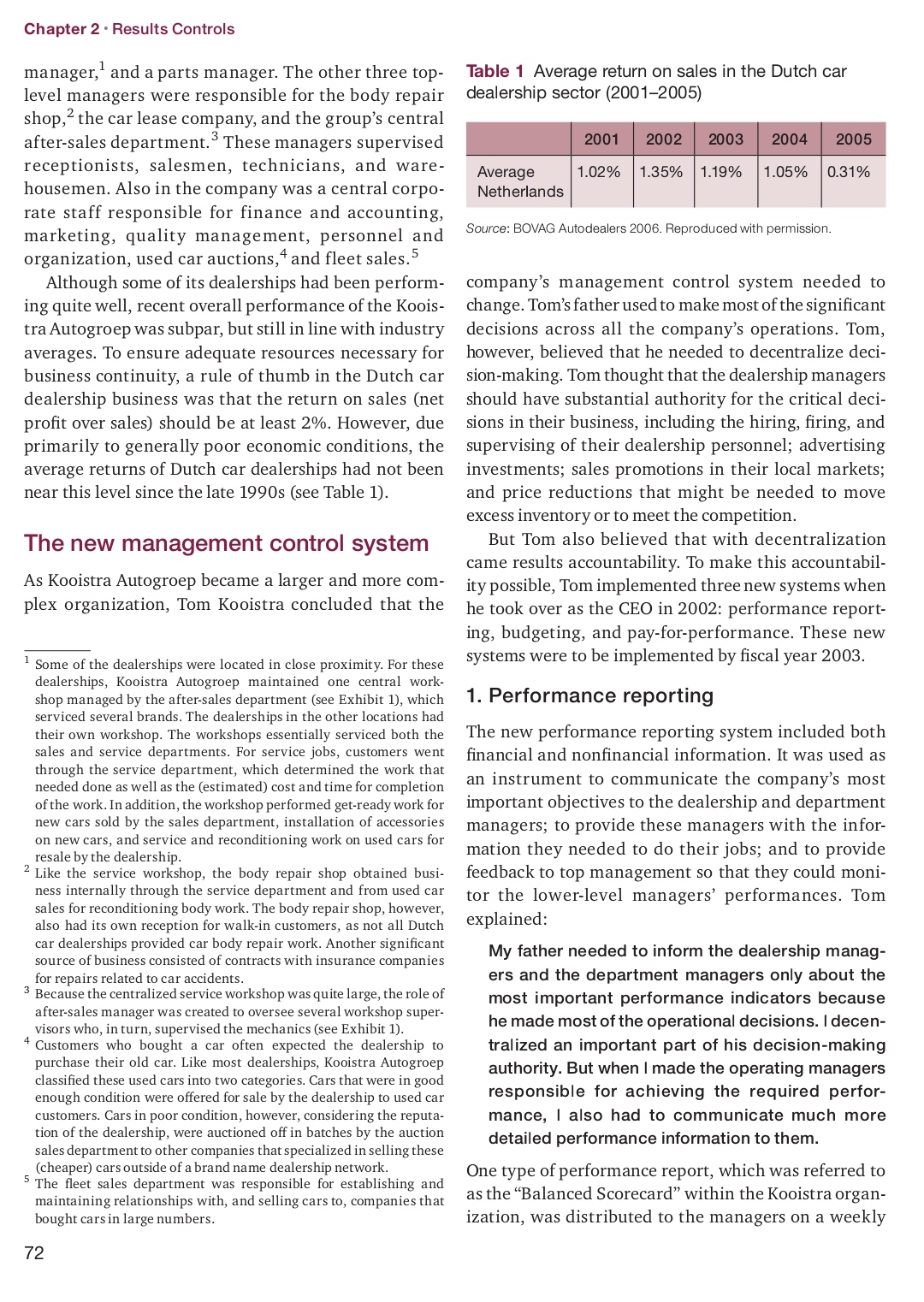

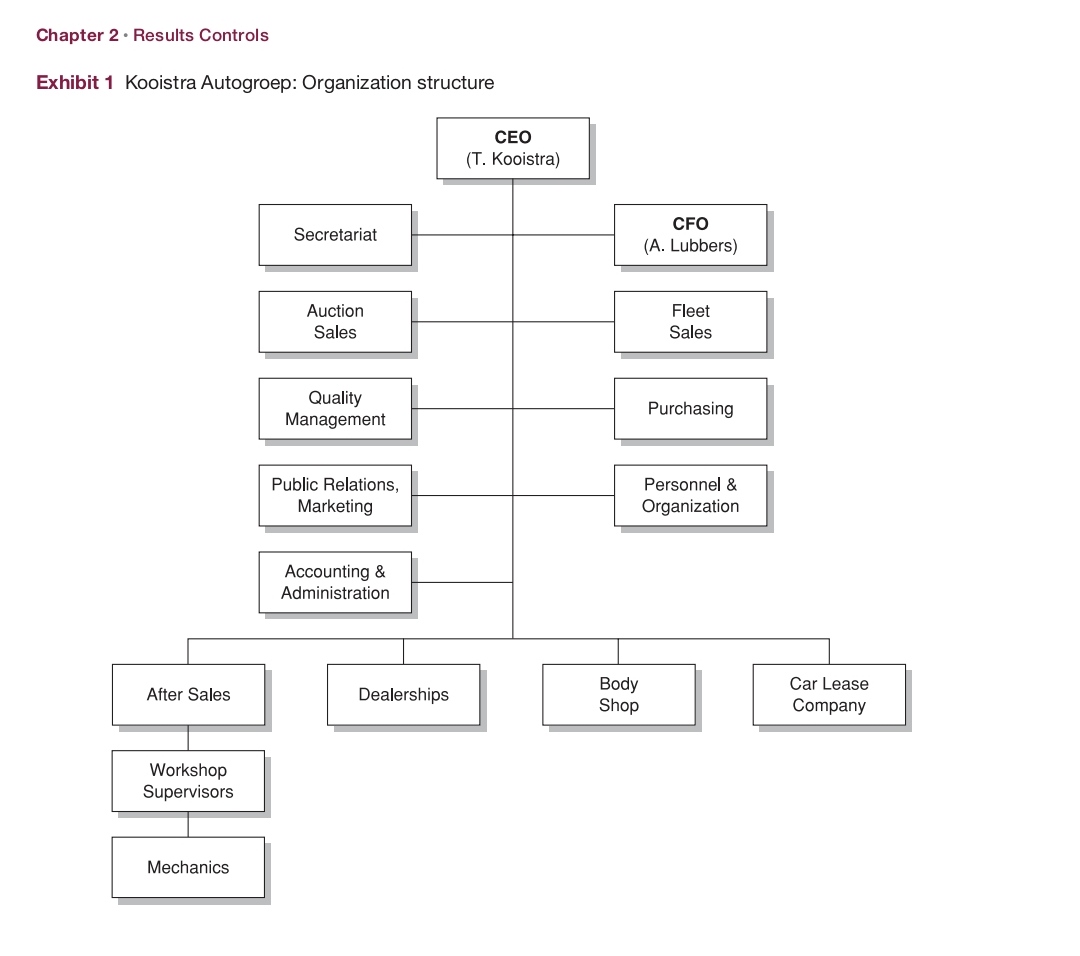

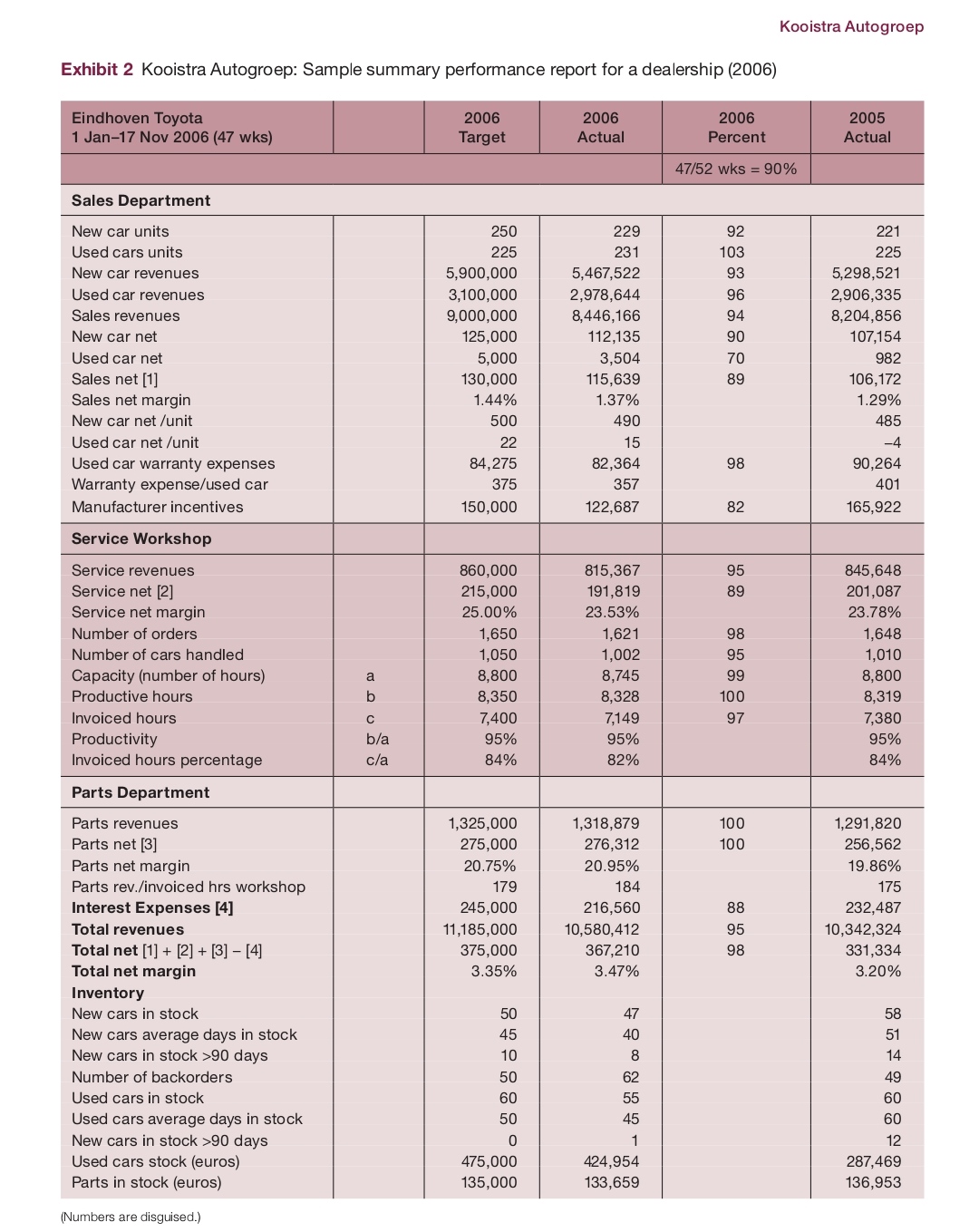

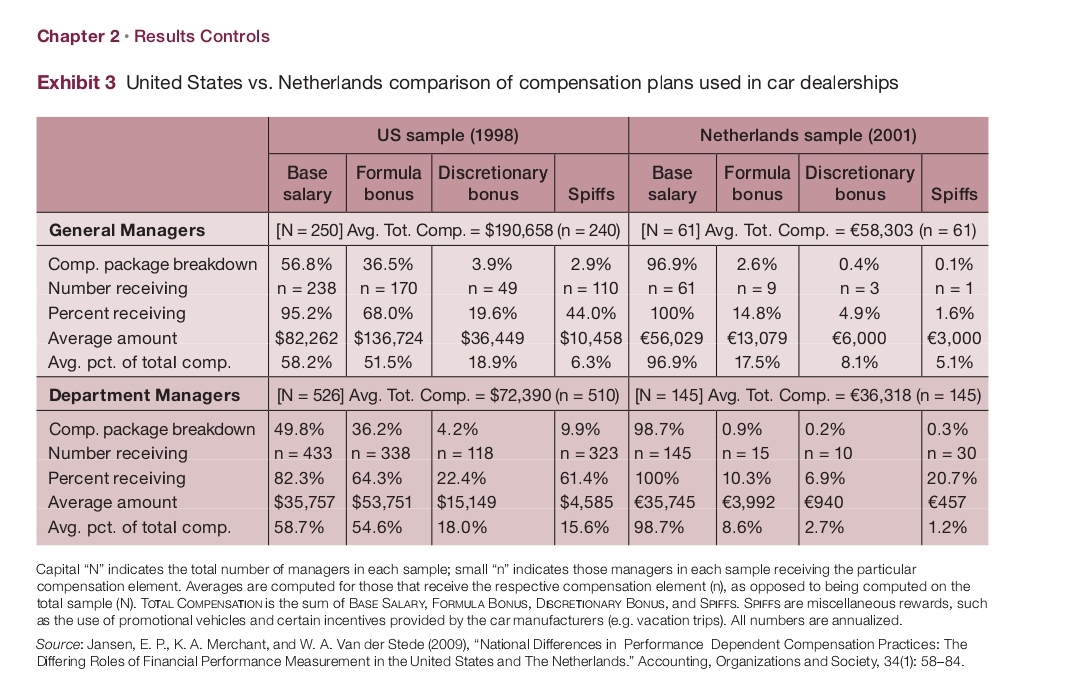

CASE STUDY Kooistra Autogroep When he took over as CEO of the Kooistra Autogroep in dealership, one Suzuki dealership, one Saab dealer- 2002, Tom Kooistra made significant changes to his com- ship, one Alfa Romeo dealership, and one combined pany's management control system. Most significantly, Chevrolet, Cadillac, Corvette, and Hummer dealer- he decentralized decision-making authority, developed ship. Opel (a brand of General Motors) had been the a performance reporting system that included both market leader in the Netherlands since the 1970s, financial and nonfinancial information, and introduced with a market share of almost 10% in 2006. Toyota a pay-for-performance system for the company's dealer- was the sixth-largest brand, with a 7% market share. ship and department managers. Tom explained: Citroen had a market share of 4%, and Suzuki and My father had been running this company like a Chevrolet had market shares of about 2-3%. The family, but we've become too big to operate like other brands sold by Kooistra - Saab, Alfa Romeo, this. Besides, we need to be more competitive to Cadillac, Corvette, and Hummer - all had market survive. That's why I am so keen on implementing shares of less than 1%. For these smaller brands, the the new pay-for-performance plan. With decentrali- nearest competing dealership was typically located zation comes accountability for performance. If our far away. In addition to the car dealerships, the Koois- people are willing to accept that accountability, tra Autogroep also owned a body repair shop and a car lease company. then I am quite willing to share with them a fair pro- In the context of Dutch automobile retailers, Koois- portion of the company's success. tra was large. Even in 2007, the typical Dutch car deal- But while the company's managers seemed to value ership sold and serviced cars of only one brand from a the increased authority and performance-related infor- single location. Most dealerships were family-owned, mation, their feelings regarding the pay-for-perfor- with about 20 employees on average. mance system were mixed. In 2007, Tom was considering In the early 2000s, as a consequence of the weak whether he should try to reinforce the system by telling economic conditions and increased competition, the the managers that the system was here to stay and that financial performance of most Dutch car dealers dete- they needed to learn how to make it work, or whether he riorated. This performance deterioration gave rise to should revise, or possibly even abandon, the system. many changes in the industry. One important change was industry consolidation. Many larger car dealer- The company ships expanded through acquiring several formerly family-owned dealerships. Kooistra Autogroep was Kooistra Autogroep was a family-owned automobile among the first to expand the number of brands sold, retailing company founded in 1953. Over the years, standardize operating procedures, and exploit econo- Kooistra grew from a small company that sold and ser- mies of scale. viced cars of only one or two brands from a single location In 2002, Tom Kooistra's father retired, and Tom to a top-20 player in the Dutch car dealership market. took over as the company's CEO. Tom chaired the In early 2007, it owned and operated 13 dealership loca- company's top-management team (see Exhibit 1). tions selling 10 brands of automobiles and employed Also on the top-management team were Anna Lub- approximately 325 people. bers, CFO, and eight managers. Five of the managers The Kooistra dealerships were located in the city of were dealership managers; each responsible for sev Tilburg and in smaller surrounding towns in the eral dealership locations selling between one and southern part of the Netherlands. Kooistra owned five five brands. Each dealership location employed a Opel dealerships, three Toyota dealerships, one Citroen sales manager, a service manager, a workshop 71Chapter 2 - Results Controls manager,1 and a parts manager. The other three top- level managers were responsible for the body repair shop,2 the car lease company, and the group's central after-sales department.3 These managers supervised receptionists, salesmen, technicians, and ware- housemen. Also in the company was a central corpo- rate staff responsible for finance and accounting, marketing, quality management, personnel and organization, used car auctions,4 and fleet sales.5 Although some of its dealerships had been perform- ing quite well, recent overall performance of the Koois- tra Autogroep was subpar, but still in line with industry averages. To ensure adequate resources necessary for business continuity, a rule of thumb in the Dutch car dealership business was that the return on sales (net prot over sales] should be at least 2%. However, due primarily to generally poor economic conditions, the average returns of Dutch car dealerships had not been near this level since the late 1990s (see Table 1]. The new management control system As Kooistra Autogroep became a larger and more com- plex organization, Tom Kooistra concluded that the Some of the dealerships were located in close proximity. For these dealerships, Kooistra Autogroep maintained one central work- shop managed by the after-sales department (see Exhibit 1), which serviced several brands. The dealerships in the other locations had their own workshop. The workshops essentially serviced both the sales and service departments. For service jobs, customers went dirough the service department, which determined the work that needed done as well as the (estimated) cost and time for completion ofthe work. In addition, the workshop performed get-readywork for new cars sold by the sales department, installation of accessories on new cars, and service and reconditioning work on used cars for resale by the dealership. Like the service workshop, the body repair shop obtained busi- ness internally through the service department and from used car sales for reconditioning body work. The body repair shop, however, also had its own reception for walk-in customers, as not all Dutch car dealerships provided car body repair work. Another signicant source of business consisted of contracts with insurance companies for repairs related to car accidents. Because the centralized service workshop was quite large, the role of after-sales manager was created to oversee severalworkshop super- visors who, inturn, supervised the mechanics (see Exhibit 1). Customers who bought a car often expected the dealership to purchase their old car. Like most dealerships, Kooistra Autogroep classied these used cars into two categories. Cars that were in good enough condition were offered for sale by the dealership to used car customers. Cars in poor condition, however, considering the reputa- tion of the dealership, were auctioned offin batches by the auction sales department to other companies that specialized in selling these (cheaper) cars outside of a brand name dealership network. The eet sales department was responsible for establishing and maintaining relationships with, and selling cars to, companies that bought cars in large numbers. 72 Table 1 Average return on sales in the Dutch car dealership sector (20012 005) 1.02% 1.35% 1.19% 1.05% 0.31% Average Netherlands Source: BOVAG Autodealers 2005. Reproduced with permission. company's management control system needed to change. Tom's father used to make most ofthe signicant decisions across all the company's operations. Tom, however, believed that he needed to decentralize deci- sion-making. Tom thought that the dealership managers should have substantial authority for the critical deci- sions in their business, including the hiring, ring, and supervising of their dealership personnel; advertising investments; sales promotions in their local markets; and price reductions that might be needed to move excess inventory or to meet the competition. But Tom also believed that with decentralization came results accountability. To make this accountabil- ity possible, Tom implemented three new systems when he took over as the CEO in 2002: performance report- ing, budgeting, and pay-for-performance. These new systems were to be implemented by scal year 2003. 1. Performance reporting The new performance reporting system included both nancial and nonnancial information. It was used as an instrument to communicate the company's most important objectives to the dealership and department managers; to provide these managers with the infor- mation they needed to do theirjobs; and to provide feedback to top management so that they could moni- tor the lowerlevel managers' performances. Tom explained: My father needed to inform the dealership manag- ers and the department managers only about the most important performance indicators because he made most of the operational decisions. Idecen- tralized an important part of his decision-making authority. But when I made the operating managers responsible for achieving the required perfor- mance, I also had to communicate much more detailed performance information to them. One type of performance report, which was referred to as the \"Balanced Scorecard\" within the Kooistra organ- ization, was distributed to the managers on a weekly basis. It reported year-to-date summary performance on key metrics for each individual manager's opera- tions (e.g. a dealership] with an indication ofprogress towards budget target accomplishment. Exhibit 2 shows this socalled Balanced Scorecard for the Toyota dealership. In addition to the weekly balanced score- cards, the managers also received far more detailed monthly reports, with sometimes up to hundreds of line items pertaining to their areas ofoperation. The dealership and department managers apparently used the performance reports actively. Tom explained: Every Thursday at 2 o'clock, the dealership and department managers receive their Balanced Scorecards by email. When I walk through the company on Thursday afternoon and the reports have not yet been emailed, department managers ask me what's up. The department managers are interested in their performance and, particularly, in comparing their performance v'r's-a-vfs target. 2. Budgeting At the same time, Tom introduced a formal annual budg- eting process. Although various types of financial and nonnancial information were considered during the budgeting process, the main focus was on determining net prot targets for the forthcoming year. Net prot was dened as revenues minus controlla- ble expenses, which in practice meant that most corporate overhead allocations were \"below the line\" on which the operating managers focused. However, Tom felt that continued decentralization would eventu- ally lead the company to improve its methods of allo- cating shared service costs to obtain more inclusive net prot numbers and, thus, to allow even better account- ability at lower organizational levels. The budgeting process was intended to be bottom- up. The responsible managers prepared their own budget proposals. The budget proposals were then reviewed by Tom and the CFO, Anna Lubbers, followed by what they both described as \"rather tough, some- times vociferous, discussions\" with each manager. Tom and Anna decided the nal budgets. The budget discussions served several useful pur- poses. Most managers were inexperienced with budg- eting and only few ofthem had had any formal business education. Anna noted that, For these and other reasons we can't always trust the initial budget proposals, so we have to have a Kooistra Autogroep very hard look at them. In the end, however, I believe that we find the proverbial happy medium for targets thatwe feel the manager should be will- ing to commit to. But not only did the budgeting discussions serve a training role, they also were avaluable communication tool to focus discussions about the business, which allowed Tom and Anna to solicit information from those who were closest to the day-to-day operations from which they themselves had become farther removed. Tom and Anna monitored performance through weekly reviews ofthe Balanced Scorecards. When they saw performance patterns that were of concern to them because they were not consistent with the budget tar- gets and/or the performance ofother company entities, they had conversations with the managers. The entire top-management team also held monthly meetings to review performance issues and discuss other company- wide business matters. The net prot budget targets were believed to be achievable with considerable effort. As Exhibit 2 shows, the Toyota dealership had almost achieved its 20 06 net prot target even though there were still ve weeks to go in the budget year. When asked, the Toyota dealer- ship manager estimated that at the time his budget was approved, his likelihood ofachieving the net prot tar- get was around 90%.1Ie also pointed out that \"Although I've made my budget in each ofthe past three years, it was rather close. But not all of my department manag- ers met their budget each year. My workshop depart- ment had some cost control issues and did not always achieve its net prot targets.\" The Toyota dealership was among the best-performing entities in the Kooistra Autogroep. Some of the other dealership managers, however, complained that they had trouble meeting their budget targets due to factors outside of their control. For exam ple, the combined Chevrolet, Cadillac, Corvette, and Hummer dealership complained that recent hikes in fuel prices had negatively impacted car sales beyond what could have been foreseen at budget time. He wasn't sure, however, that Tom would be sympathetic ifhe failed to meet his budget, which he likely would this year. But Tom also could sometimes \"help\" the dealerships make their target. Kooistra Autogroep had a sizable con- tract with a big rental car company that specied the number and type of cars (e.g. small cars, medium-sized family cars, vans), but not the brand, that the rental car 73 Chapter 2 - Results Controls company purchased. Thus, when the Opel dealership was close to making its target but needed \"a little help,\" Tom could offer the Opel Astra model to the rental car company. Alternatively, if the Toyota dealership needed some help, he could propose the Toyota Corolla instead. Tom noted that, because of this leverage, he faced con- siderable lobbying from the dealership managers to go with their brand. He said, \"I never hear any complaints when good fortune comes their way. It's onlywhen they miss their targets that I hear them grumbling.\" 3. Pay-for-perform an so A third major change was the expansion of a pay-for- performance system for salespeople and the implemen- tation of a payforperformance system for dealership and department managers. Some salespeople already received a bonus. But now Tom introduced a pay-for- performance bonus plan for the managers. Traditionally, compensation for nearly all personnel in the Netherlands was not performance-dependent. It was based on ajob rating, an assessment of the training and experience needed for executing a job, rather than on the individual performance of the employee. Thejob ratings were linked to preestablished salary increases. Hence, the relationship between levels of compensation and actual employee performance was usually weak. To bypass the limits of salary increases for a certain job grade, topperforming individuals often were promoted to jobs with a higher job rating when those positions became available. For example, sometimes, excellent car salespeople were promoted to sales man ager positions. These promotions sometimes happened even when the dealership would have benefited more from the individual's continued selling efforts than it would from their management skills. For years at Kooistra, salespeople had had monthly sales targets, defined in terms of the number of (new and used) cars sold. Some of the salespeople were eligi- ble for bonus payouts. In 2007, these bonus-eligible salespeople earned 18.50 per car sold. In addition, when the salesperson met his or her monthly sales tar- get, the bonus amount was doubled to 37.00 per car for the month. On average, bonus payments were about 25% of salary for salespeople who met their targets. However, not all salespeople were yet eligible for bonuses. Of the 45 salespeople at Kooistra Autogroep, only 25 were bonus-eligible because some of them had negotiated a compensation package without a bonus contingency when they were hired, sometimes at a dealership that had been acquired. These contracts could not easily be renegotiated. Considering these fac- tors, Kooistra's top managers admitted that the sales bonus plan was limited in scope. It also was still subject to change. Anna Lubbers, CFO, explained that manage- ment was considering fine-tuning the sales bonus plan by incorporating other performance criteria perhaps gross, or even net, profit per car. Tom's new pay-forperformance system for managers added a bonus element to the managers' compensation package. The bonuses were added on top of the manag- ers' salaries. Target bonuses for dealership managers were set between 10% and 20% of annual salary. Target bonuses for department managers were set at 8% of annual salary. For dealership and department manag- ers, the bonuses were based on the extent to which the managers met their annual net profit targets as set dur- ing the budgeting process. Only managers who met their net profit target earned their target bonus. No bonuses were paid for below- or abovetarget performance. Both Tom and Anna believed that the bonus plan specifically, and the idea of pay-forperformance more generally, was putting the company on the right track. Tom explained: I introduced bonuses primarily to make managers conscious of the fact that something had changed [...] that department managers were not only given more decision-making authority but that their responsibilities to meet expected performance also had changed. I think the plan had that desired effect. Management also had the authority to reduce any or allbonus awards. However, in the first three years since implementation of the system, such discretion had never been applied. Moreover, the criteria that might justify a bonus reduction were not yet clear, as Tom explained: Theoretically we might reduce bonuses because, for example, administrative procedures were not followed or customer satisfaction ratings were too low. But a bonus reduction would be a very subjec- tive decision. We need to articulate the criteria for such decisions more clearly. This is a priority for the coming year. Issues Pay-for-performance was a relatively unknown phe- nomenon in Dutch companies. For example, one study showed that in 2001, only 10% of the department man agers in Dutch car dealerships received a formula bonus, and only 7% received a "discretionary\" (subjec- tively assigned) bonus (see Exhibit 3]. For sales manag ers, these percentages were somewhat higher: 20% and 7%, respectively (not tabulated in Exhibit 3). However, several studies had shown that Dutch companies (not just car dealerships) were increasingly relying on pay-for-performance practices, which was commonly attributed to increased international com petition. One study concluded that although only a minority of Dutch companies applied some form of pay- for-performance, the trend towards doing so was upward, with 33%, 36%, and 40% ofa sample of Dutch firms using some form of pay-forperformance in 1997, 1999, and 2001, respectively.6 Because such systems were rare in Dutch dealer- ships, perhaps not surprisingly, Kooistra Autogroep faced considerable skepticism from its employees when it first introduced its payforperformance sys tem. A survey conducted by a consultant showed that the vast majority of Kooistra employees preferred a salary raise over a bonus, even if the raise was signifi- cantly lower than the expected bonus. To illustrate this point, Edwin Vliering, a dealership manager, recounted the following conversation he had had with one of his salesmen: In terms of profit and sales volume, the last threefour years were generally bad years for Dutch car dealer- ships. At the beginning of 2006, one of my top sales- men asked for a salary raise. I offered her a bonus instead. In her situation the bonus would have resulted in more money than the raise she had asked for, even in the poor last couple of years. Nevertheless, she was unhappy. She clearly valued the security of a fixed income. I'd say that she is quite representative of the vast majority of employees around here. 6 For example, see 5. Bckker, D. Fouarge, M. Kerkhofs, A. Romain, M. de Voogd-Hamelink, T. Wilthagen, and C. de Wolff, endrapport: Wrmgnaw'm'beid2002 [Tilburg, August 2003, ISBN 906566 0623). Did the payforperformance system provide a sig nicant motivational boost? Edwin thought the answer to this question was no: Due to the economic situation, the last couple of years were not good years. Consequently, my dealership and some of my department managers did not make their targets and did not receive their bonus. In my opinion, however, this has not affected the motivation of any of us. We are all still working hard. On the other hand, even in good years the level of the bonuses is, lthink, too low to motivate, particularly for the department managers. In all truth, I wouldn't mind if we abolished the bonuses for department managers. On the other hand, Tom Kooistra and Anna Lubbers were convinced that the bonuses could, and did, affect motivation. Tom explained: Our managers are certainly highly motivated. This was true in recent years even though, due to the poor economic situation, some of them were una- ble to realize their performance targets. But I am convinced that they make considerable extra effort when they have a chance to meet their targets. For example, they organize extra sales activities when realization of the target is possible. I also know that they feel good when they achieve their targets. That is part of the motivation. But the money is obviously important as well. Anna Lubbers agreed that the bonuses could provide strong motivational effects, although she believed that that depended strongly on the likelihood that the man agers can meet their targets: It is important to set realistic targets. Only bonuses that are based on realistic targets have a motivat- ing effect. Setting realistic targets is particularly important in years of an economic slump, like in recent years. When the target is a pie in the sky, the bonus will not work. Chapter 2 . Results Controls Exhibit 1 Kooistra Autogroep: Organization structure CEO (T. Kooistra) CFO Secretariat (A. Lubbers) Auction Fleet Sales Sales Quality Purchasing Management Public Relations, Personnel & Marketing Organization Accounting & Administration Body Car Lease After Sales Dealerships Shop Company Workshop Supervisors MechanicsKooistra Autogroep Exhibit 2 Kooistra Autogroep: Sample summary performance report for a dealership (2006) Sales Department New car units 250 229 92 221 Used cars units 225 231 103 225 New car revenues 5,900,000 5,467,522 93 5,298,521 Used car revenues 3,100,000 2,978,644 96 2,906,335 Sales revenues 9,000,000 8,446,166 94 8,204,856 New car net 125,000 112,135 90 107,154 Used car net 5,000 3,504 70 982 Sales net [1] 130,000 115,639 89 106,172 Sales net margin 1.44% 1.37% 1.29% New car net r'unit 500 490 485 Used car net {unit 22 15 4 Used car warranty expenses 84,275 82,364 98 90,264 Warranty expenselused car 375 357 401 Ma nufactu rer incentives 150,000 122,687 82 165,922 ooooowoooooo Service revenues 860,000 815,367 95 845,648 Service net [2} 215,000 191,819 89 201,087 Service net margin 25.00% 23.53% 23.78% Number of orders 1,650 1,621 98 1,648 Number o1 cars handled 1,050 1,002 95 1,010 Capacity {number of hours) a 8,800 8,745 99 8,800 Productive hours b 8,350 8,328 100 8,319 Invoiced hours c 7,400 7,149 97 7,380 Productivity bfa 95% 95% 95% Invoiced hours percentage cz'a 84% 82% 84% Parts Department Parts revenues 1,325,000 1,318,879 100 1,291,820 Parts net [3] 275,000 276,312 100 256,562 Parts net margin 20.75% 20.95% 19.86% Parts reinnvoiced hrs workshop 179 184 175 Interest Expenses [4] 245,000 216,560 88 232,487 Total revenues 11,185,000 10,580,412 95 10,342,324 Total net [1] + [2] + [3] [4] 375,000 337,210 93 331,334 Total net margin 3.35% 3.47% 3.20% lnventciryr New cars in stock 50 47 58 New cars average days in stock 45 40 51 New cars in stock >90 days 10 8 14 Number of backorders 50 62 49 Used cars in stock 60 55 60 Used cars average days in stock 50 45 60 New cars in stock >90 days 0 1 12 Used cars stock (euros) 475,000 424,954 287,469 Parts in stock (euros) 135,000 133,659 136,953 [Numbers are disguised.) Chapter 2 - Results Controls Exhibit 3 United States vs. Netherlands comparison of compensation plans used in car dealerships General Managers [N = 250] Avg. Tot. Comp. = $190,658 (n = 240) [N = 61] Avg. Tot. Comp. = 58,303 (n = 61) Comp. package breakdown N umber receiving Percent receiving Average amount Avg. pct. of total comp. Department Managers Comp. package breakdown Number receiving Percent receiving Average amount Avg. pct. of total comp. 56.8% 36.5% 3.9% 2.9% 96.9% 2.6% 0.4% 0.1% n=238 n=170 n=49 n=110 n=61 n=9 n=3 n=1 95.2% 68.0% 19.6% 44.0% 100% 14.8% 4.9% 1.6% $32,232 $133,724 $33,449 $10,453 50,029 13,079 0,000 3,000 58.2% 51.5% 18.9% 6.3% 96.9% 17.5% 8.1% 5.1% [N = 526] Avg. Tot. Comp. = $72,390 (n = 510] [N = 145] Avg. Tot. Comp. = 36,313 {n = 145) 49.3% 36.2% 4.2% 9.9% 93.7% 0.9% 0.2% 0.3% n=433 n=333 n=113 n=323 n=145 n=15 n=10 n=30 32.3% 64.3% 22.4% 61.4% 100% 10.3% 6.9% 20.7% $35,757 $53,751 $15,149 $4,535 35,745 3,992 940 457 53.7% 54.6% 13.0% 15.6% 93.7% 3.6% 2.7% 1.2% Capital "N" indicates the total number of managers in each sample; small "n" indicates those managers in eac 1 sample receiving the particular compensation element. Averages are computed for those that receive the respective compensation element [n], as opposed to being computed on the total sample {N}. TOTAL COMPENSATION is the sum of ElAsE SALARY, FORMLLA Dome, DECRETIONAR'Y Borne, and SPlFFS. SPIFFS are miscellaneous rewards, such as the use of promotional vehicles and certain incentives provided by the car manufacturers [e.g. vacation trips]. All numbers are annualized. Source: Jansen, E. P., K. A. Merchant, and W. A. Van derStede 2009), " National Differences in Performance Dependent Compensation Practices: The Differing Roles of Financial Performance Measurement in the United States and The Netherlands." Accounting, Organizations and Society, 34(1): 5884. 1. Did Kooistra Autogroep management go too far in decentralizing the organization? Did they not go far enough? Or did they get it just right? Why? Explain thoroughly 2. Evaluate the budgeting used at Kooistra Autogroep. What are the problems/issue encountered by the company. What changes would you recommend, if any? Explain thoroughly 3. Evaluate the performance measurement used at Kooistra Autogroep. What are the problems/issue encountered by the company. What changes would you recommend, if any? Explain thoroughly 4. Evaluate the incentive systems used at Kooistra Autogroep. What are the problems/ issue encountered by the company. What changes would you recommend, if any? Explain thoroughly 5. What can you say about the company's organisation structure? Is it effective? If not what is your recommendation? Explain 6. Based on the case study, what do you think the advantages and disadvantages of decentralization? 7." Of the 45 salespeople at Kooistra Autogroep, only 25 were bonus-eligible\" does this create "equity\" issues

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance