Answered step by step

Verified Expert Solution

Question

1 Approved Answer

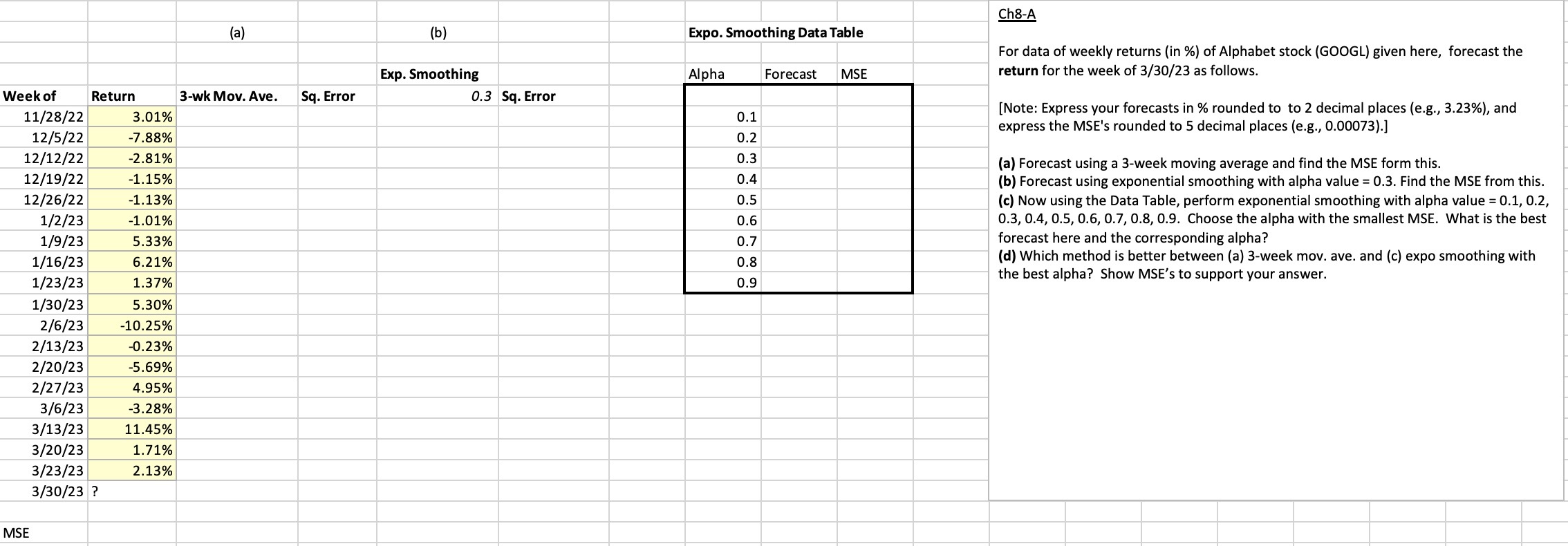

Ch8-A For data of weekly returns (in %) of Alphabet stock (GOOGL) given here, forecast the return for the week of 3/30/23 as follows. [Note:

Ch8-A For data of weekly returns (in \%) of Alphabet stock (GOOGL) given here, forecast the return for the week of 3/30/23 as follows. [Note: Express your forecasts in \% rounded to to 2 decimal places (e.g., 3.23\%), and express the MSE's rounded to 5 decimal places (e.g., 0.00073).] (a) Forecast using a 3-week moving average and find the MSE form this. (b) Forecast using exponential smoothing with alpha value =0.3. Find the MSE from this. (c) Now using the Data Table, perform exponential smoothing with alpha value =0.1,0.2, 0.3,0.4,0.5,0.6,0.7,0.8,0.9. Choose the alpha with the smallest MSE. What is the best forecast here and the corresponding alpha? (d) Which method is better between (a) 3-week mov. ave. and (c) expo smoothing with the best alpha? Show MSE's to support your

Ch8-A For data of weekly returns (in \%) of Alphabet stock (GOOGL) given here, forecast the return for the week of 3/30/23 as follows. [Note: Express your forecasts in \% rounded to to 2 decimal places (e.g., 3.23\%), and express the MSE's rounded to 5 decimal places (e.g., 0.00073).] (a) Forecast using a 3-week moving average and find the MSE form this. (b) Forecast using exponential smoothing with alpha value =0.3. Find the MSE from this. (c) Now using the Data Table, perform exponential smoothing with alpha value =0.1,0.2, 0.3,0.4,0.5,0.6,0.7,0.8,0.9. Choose the alpha with the smallest MSE. What is the best forecast here and the corresponding alpha? (d) Which method is better between (a) 3-week mov. ave. and (c) expo smoothing with the best alpha? Show MSE's to support your Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Globalization Gating And Risk Finance

Authors: Unurjargal Nyambuu, Charles S. Tapiero

1st Edition

1119252652, 978-1119252658