Answered step by step

Verified Expert Solution

Question

1 Approved Answer

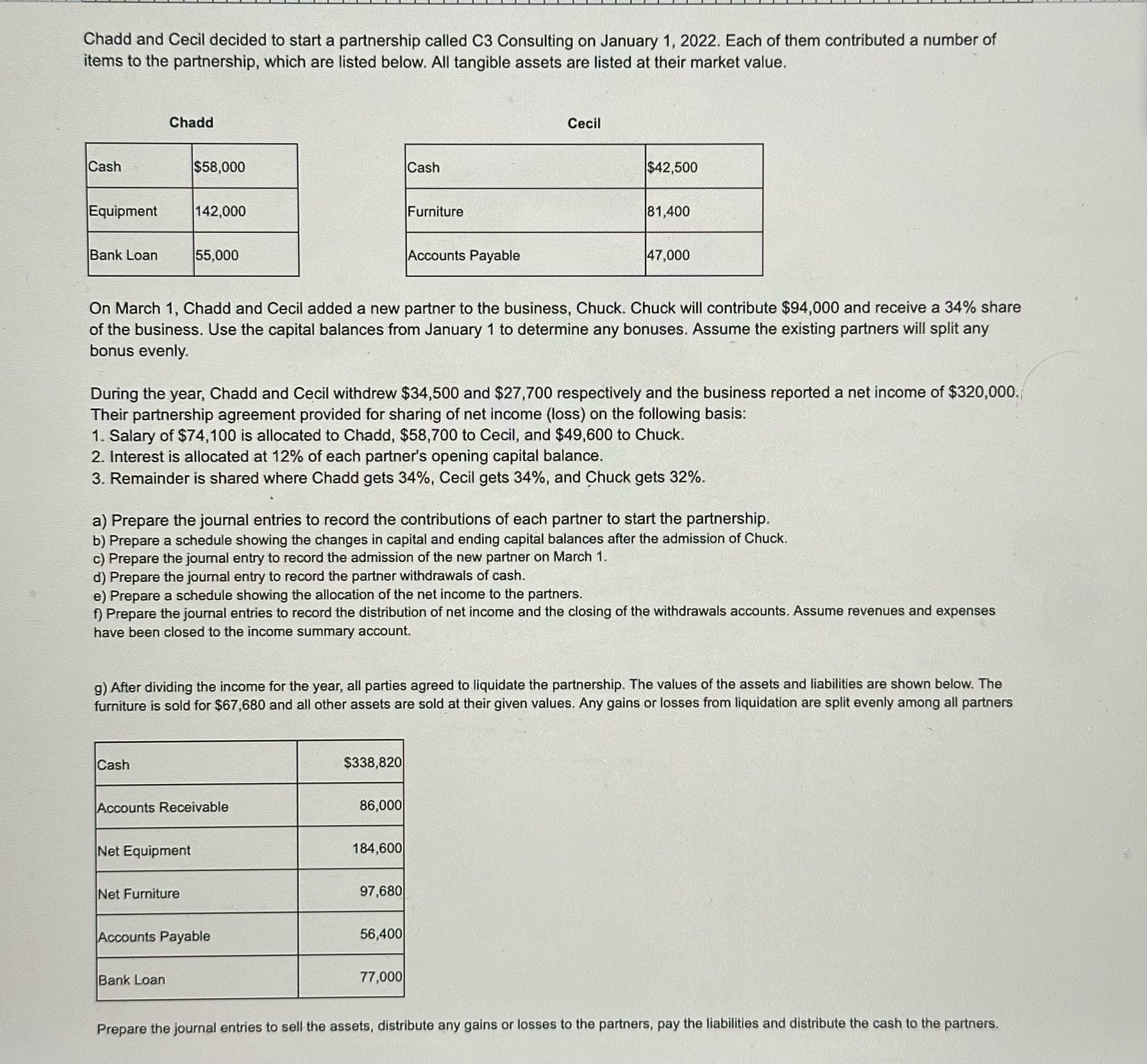

Chadd and Cecil decided to start a partnership called C3 Consulting on January 1, 2022. Each of them contributed a number of items to

Chadd and Cecil decided to start a partnership called C3 Consulting on January 1, 2022. Each of them contributed a number of items to the partnership, which are listed below. All tangible assets are listed at their market value. Chadd Cash $58,000 Cash Equipment 142,000 Bank Loan 55,000 Furniture Accounts Payable Cecil $42,500 81,400 47,000 On March 1, Chadd and Cecil added a new partner to the business, Chuck. Chuck will contribute $94,000 and receive a 34% share of the business. Use the capital balances from January 1 to determine any bonuses. Assume the existing partners will split any bonus evenly. During the year, Chadd and Cecil withdrew $34,500 and $27,700 respectively and the business reported a net income of $320,000. Their partnership agreement provided for sharing of net income (loss) on the following basis: 1. Salary of $74,100 is allocated to Chadd, $58,700 to Cecil, and $49,600 to Chuck. 2. Interest is allocated at 12% of each partner's opening capital balance. 3. Remainder is shared where Chadd gets 34%, Cecil gets 34%, and Chuck gets 32%. a) Prepare the journal entries to record the contributions of each partner to start the partnership. b) Prepare a schedule showing the changes in capital and ending capital balances after the admission of Chuck. c) Prepare the journal entry to record the admission of the new partner on March 1. d) Prepare the journal entry to record the partner withdrawals of cash. e) Prepare a schedule showing the allocation of the net income to the partners. f) Prepare the journal entries to record the distribution of net income and the closing of the withdrawals accounts. Assume revenues and expenses have been closed to the income summary account. g) After dividing the income for the year, all parties agreed to liquidate the partnership. The values of the assets and liabilities are shown below. The furniture is sold for $67,680 and all other assets are sold at their given values. Any gains or losses from liquidation are split evenly among all partners Cash $338,820 Accounts Receivable 86,000 Net Equipment 184,600 Net Furniture 97,680 Accounts Payable 56,400 Bank Loan 77,000 Prepare the journal entries to sell the assets, distribute any gains or losses to the partners, pay the liabilities and distribute the cash to the partners.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting

Authors: Jonathan E. Duchac, James M. Reeve, Carl S. Warren

23rd Edition

978-0324662962