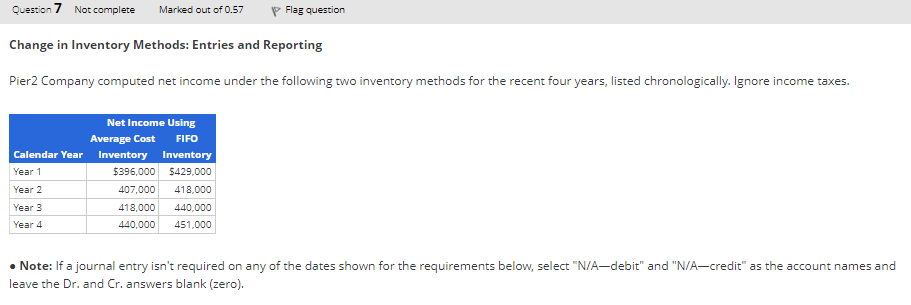

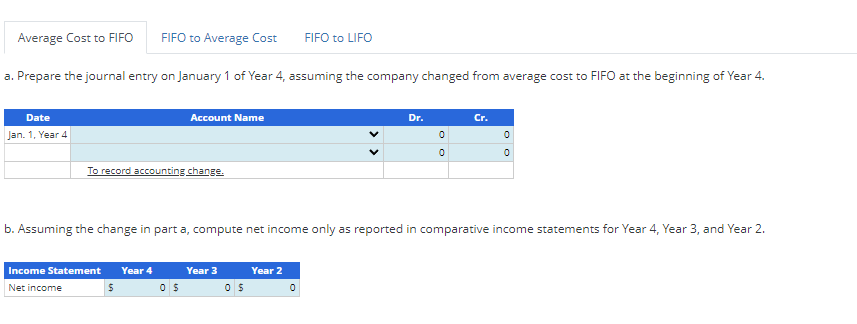

Change in Inventory Methods: Entries and Reporting Pier2 Company computed net income under the following two inventory methods for the recent four years, listed chronologically. Ignore income taxes. - Note: If a journal entry isn't required on any of the dates shown for the requirements below, select "N/A-debit" and "N/A-credit" as the account names and leave the Dr. and Cr. answers blank (zero). a. Prepare the journal entry on January 1 of Year 4 , assuming the company changed from average cost to FIFO at the beginning of Year 4 . b. Assuming the change in part a, compute net income only as reported in comparative income statements for Year 4, Year 3, and Year 2. E. Prepare the journal entry on January 1 of Year 4, assuming the company changed from FIFO to average cost at the beginning of Year 4. 8. Assuming the change in part c, compute net income only as reported in comparative income statements for Year 4, Year 3, and Year 2. Instead, assume that the company changes from FIFO to LIFO at the beginning of Year 4 . The company is unable to estimate the LIFO amounts for earlier :ars. What entry does the company record for the change in accounting method on January 1 of Year 4 ? Change in Inventory Methods: Entries and Reporting Pier2 Company computed net income under the following two inventory methods for the recent four years, listed chronologically. Ignore income taxes. - Note: If a journal entry isn't required on any of the dates shown for the requirements below, select "N/A-debit" and "N/A-credit" as the account names and leave the Dr. and Cr. answers blank (zero). a. Prepare the journal entry on January 1 of Year 4 , assuming the company changed from average cost to FIFO at the beginning of Year 4 . b. Assuming the change in part a, compute net income only as reported in comparative income statements for Year 4, Year 3, and Year 2. E. Prepare the journal entry on January 1 of Year 4, assuming the company changed from FIFO to average cost at the beginning of Year 4. 8. Assuming the change in part c, compute net income only as reported in comparative income statements for Year 4, Year 3, and Year 2. Instead, assume that the company changes from FIFO to LIFO at the beginning of Year 4 . The company is unable to estimate the LIFO amounts for earlier :ars. What entry does the company record for the change in accounting method on January 1 of Year 4