Question

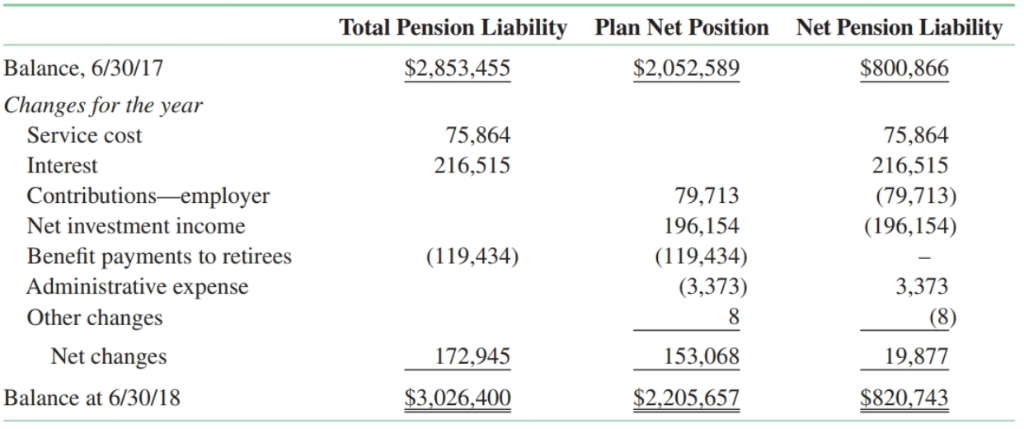

Changes in the net pension liability affect amounts reported on both balance sheets and statements of resource flows. The following was taken from a pension

Changes in the net pension liability affect amounts reported on both balance sheets and statements of resource flows. The following was taken from a pension note of Geffen County.

During the year there were no changes to employees benefits, no changes in actuarial assumptions, no difference between expected and actual experience, and no differences between actual and projected earnings.

During the year there were no changes to employees benefits, no changes in actuarial assumptions, no difference between expected and actual experience, and no differences between actual and projected earnings.

1. What is the amount that the county should report as a pension liability on its government-wide balance sheet?

2. What is the amount that it should report as a pension expense/expenditure on its

a. Government-wide statement of activities

b. Governmental-fund statement of revenues and expenditures and changes in fund balances.

3. Suppose instead that the countys actuary determined that owing to changes in estimates of future salaries, the total pension liability had increased by $50,000. The average expected service life of pen-sion plan members, including retirees, is 10 years. What impact would the change have on the citys reported pension expense in the year of the change? Be as specific as possible.

4. The June 30, 2018, balance sheet of the pension plan reported total assets of $2,305,657 and total liabilities of $100,000 (and hence a net position of $2,205,657). How could the plan report liabilities of only $100,000 when the preceding schedule indicates that the present value of obligations to employees and retirees was over $3 million?

Net Pension Liability Total Pension Liability Plan Net Position $800,866 $2,853,455 $2,052,589 Balance, 6/30/17 Changes for the year Service cost 75,864 75,864 216,515 Interest 216,515 Contributions-employer 79,713 (79,713) Net investment income 196,154 (196,154) Benefit payments to retirees Administrative expense (119,434) (119,434) (3,373) 3,373 Other changes (8) Net changes 153,068 172,945 19,877 $3,026.400 $2,205,657 $820,743 Balance at 6/30/18 Net Pension Liability Total Pension Liability Plan Net Position $800,866 $2,853,455 $2,052,589 Balance, 6/30/17 Changes for the year Service cost 75,864 75,864 216,515 Interest 216,515 Contributions-employer 79,713 (79,713) Net investment income 196,154 (196,154) Benefit payments to retirees Administrative expense (119,434) (119,434) (3,373) 3,373 Other changes (8) Net changes 153,068 172,945 19,877 $3,026.400 $2,205,657 $820,743 Balance at 6/30/18Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Information Systems Audit In Banking Sector A Study Of SBI And ICICI Banks

Authors: C. Mallesha, M. Sulochana

1st Edition

6200254397, 978-6200254399