Chapter 18 Take Home Packet

1) Solve ALL problems with a financial calculator (NO annuity formulas) - SHOW ALL WORK!!

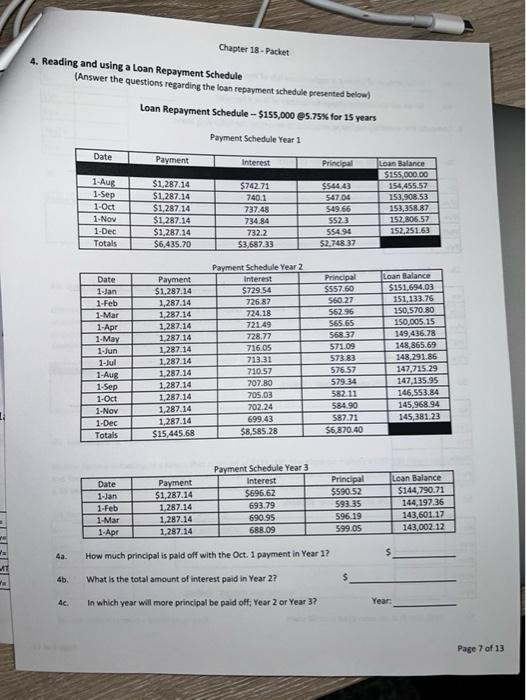

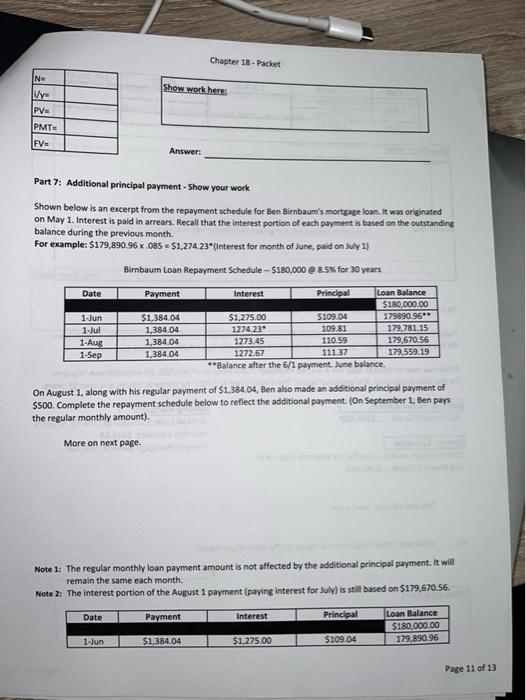

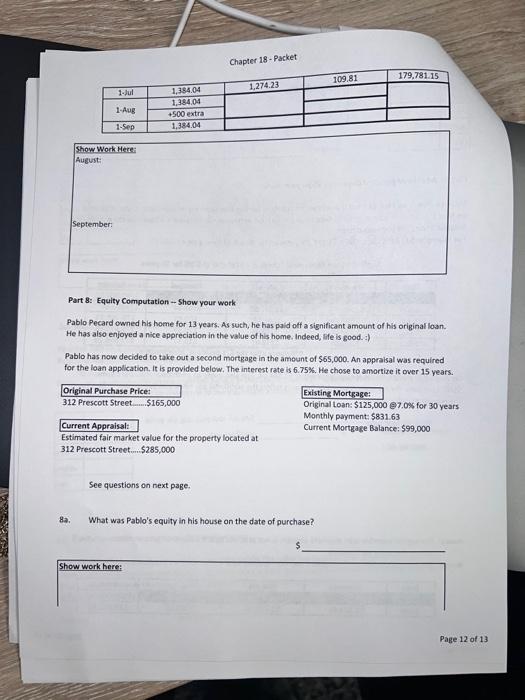

Chapter 18 - Packet a Chapter 18 Take Home Packet 1) Solve ALL. problems with a financial calculator (NO annuity formulas) - SHOW ALL WORKI! I recommend printing this document so that you can easily see everything. Then you can enter your answers to submit 2) Read the WORD document first. There are examples in your textbook and the WORD document to help you with this Packet. 3) Please show your work including HOW you calculate the financial keys. No credit can be given if the work is not correct. 4) Be sure to carry all decimals to at least 5 places. Example: Plia has a new mortgage loan for $150,000 at 3.2% for 30 years. How much is her monthly payment? Mortgages in this class are always monthly IN i/v= PV= PMT= FV 30*12=360 3.2/12.26667 150,000 ?? This is how to show your work." Fill in the blanks with the information you know, then solve the problem with your calculator. Finish by typing in your answer in the provided place. Please initial that you have read and understand the instructions Initial in Box 1. 1a. Loan Repayment schedule -- $250,000 @ 7.0% with a 30 year amortization PMT # Monthly Payment Interest Portion Principal Reduction Loan Balance $250,000.00 1 2 N. i/y PV- PMT FV- Page 1 of 13 Chapter 18 - Packet 1b. Loan Repayment schedule -- $250,000 @ 7.0% with a 15 year amortization Principal Reduction PMT Monthly Payment Interest Portion Loan Balance $250,000.00 1 2 Show how you calculated interest, Principal and Loan Balance N. Vy PV PMT= FV 1c. Loan Repayment Schedule - $250,000 @ 7.0% with interest only payments PMT # Monthly Payment Interest Portion Principal Reduction Loan Balance $250,000.00 1 2 INS na Show how you calculated interest. Principal and Loan Balance We na PV- Ina PMT na FV Ina 2. Comparison of a 30-year Amortization vs. 15-year Amortization (3 Parts) Page 2 of 13 Chapter 18 - Packet Repayment Schedule: $250,000 7% for 30 Years Monthly Payment Interest Portion Principal Reduction PMT # 1 204.93 1,663.26 1,663.26 1,663.26 2 Loan Balance $250,000.00 249.795.07 249,588.95 249,381.63 1,458.33 1,457.14 1,455.94 206.12 3 207.32 359 19.21 1,663.26 1,663.26 $598,774 360 1.649.11 0 1,644.05 1649.11 250,000 9.62 Totals 348,774 Repayment Schedule: $250,000 7% for 15 Years Monthly Payment Interest Portion Principal Reduction PMT Loan Balance 1 788.74 2,247.07 2,247.07 2,247.07 2 $250,000.00 249,211.26 248,417.92 247,619.95 1,458,33 1,453.73 1,449.10 793.34 797.97 3 359 2,247.07 2,247.07 25.99 13.03 154,473 360 Totals 2,221.08 2,234.37 250,000 2,234.37 0 $404,473 2a. What is the difference in the monthly payment amount for each loan? Show work here: 2b. What is the difference in the amount of principal paid off with the first payment of each loan? Page 3 of 13 Chapter 18 - Packet VE PV PMT Show work here FV 20 What is the savings, in total interest, over the life of the loan due to the shorter, 15-year amortization vs. WOW!!! $ the 30-year term? Show work here NOTE: Rather than lock into the higher payment required by a 15-year term (that they might have trouble making some borrowers instead opt for the smaller payment of a 30-year amortization and make additional principal payments whenever possible. However, as will be evident In the next problem, they then lose the advantage of lower rates on the shorter-term mortgage. An error message may result if certain inputs are not entered as a negative, meaning you must show your cash out. REMEMBER: In multi-step problems, an intermediate answer is any answer other than the final answer. Never round an intermediate answer unless that amount is to be paid out or it is recorded in the accounting records. For practical reasons, such amounts are then rounded to the nearest cent. Mortgages are always monthly for this class 3. Comparison of a 30-year Amortization vs. a 15-year Amortization (Manual) - 3 parts Part 1: A local bank offers a 7.5% 30-year foued rate mortgage. Assuming a 15% down payment, compute the following for the buyer of a $215,000 house. Amount of the loan (principal amount) Show work here b. Monthly payment amount (P87) N Page 4 of 13 Wye Chapter 18 - Packet PS PMT FVE c. Number of PMT's to be made full term of loan? Show work here d. Total dollar amount of the payments to be made over the full term of the loan? (amount to be paid back) $ Show work here: e. Total amount of principal to be paid back? f. Total amount of Interest to be paid over the full term of the loan? $ Show work here Part 2: Now, shorten the amortization term of the loan to 15 years. Compute: a. New monthly payment amount: N= Vy PV: PMT FV b. Number of PMT's to be made (full term of the loan)? Page 5 of 13 Chapter 18 - Packet R Show work here: c. Describe the relationship between the amortization term and the monthly PMT amount d. Total dollar amount of the payments to be made over the full term of the loan? Show work here: e. Total amount of principal to be paid back 1. Total amount of interest to be paid over the full term of the loan? Show work here Part 3: Compute the savings in TOTAL interest enjoyed by selecting a 15-year amortization rather than a 30-year amortization Show work here: NOTE: This is not to say that a homeowner will keep their mortgage for the duration of the term few do The purpose is to illustrate the benefits of a shorter amortization regardless of the actual loan term Page 6 of 13 3 Chapter 18-Packet 4. Reading and using a Loan Repayment Schedule (Answer the questions regarding the loan repayment schedule presented below) Loan Repayment Schedule - $155,000 5.75% for 15 years Payment Schedule Year 1 Date Payment Interest Principal 1-Aug 1-Sep 1-Oct 1-Nov 1-Dec Totals $54443 547.00 549.66 $1,287.14 $1,287.14 $1,287.14 $1,287.14 $1,287.14 $6,435.70 $742.71 740.1 737.48 734.84 732.2 $3,687.33 Loan Balance 5155,000.00 154,455.57 153,508.53 153,358.87 152 806.57 152,251.63 5523 55494 $2.748 37 Date 1-Jan 1-Feb 1-Mar 1-Apr 1. May 1.Jun 1.Jul 1-Aug 1-Sep 1-Oct 1-Nov 1-Dec Totals Payment $1,287.14 1,287.14 1,287.14 1,287.14 1.287.14 1.287.14 1.287.14 1.287.14 1.287.14 1,287.14 1,287.14 1,287.14 $15.445.68 Payment Schedule Year 2 Interest $729.54 726.87 724.18 721.49 728.77 716.05 713 31 710.57 707.80 705.03 70224 699.43 $8,585.28 Principal $557.60 560.27 562.96 565.65 568.37 571.09 573.83 576 57 579.34 582.11 584.90 587.71 $6.870.40 Loan Balance $151,694,03 151,133.76 150.570.80 150,005.15 149,436.78 148,865.69 148,291.86 147,715.29 147,135.95 146,553.84 145,968.94 145,381.23 Date 1-Jan 1-Feb 1-Mar 1. Apr Payment $1,287.14 1,287.14 1,287.14 1,287.14 Payment Schedule Year 3 Interest $696.62 693.79 690.95 688.09 Principal $590.52 59335 596.19 599.05 Loan Balance $144,790.71 144,197.36 143,601.17 143,002.12 $ 4a. How much principal is paid off with the Oct. 1 payment in Year 1? -11 4b. What is the total amount of interest paid in Year 2? $ 4. In which year will more principal be paid off; Year 2 or Year 3? Year Page 7 of 13 Chapter 18 - Packet 4d. What amount of interest is applicable to July of Year 2? When will the interest charge for January of Year 3 be paid? 5. Compute the monthly payment required to amortize the following loans: 4e. Sa $60,000 4.75% amortized over 15 years. N wy PV PMT FV 5b. $60,000 4.75% amortized over 30 years. IN PV PMT- FV 5c. $112,500 e 5.0% amortized over 15 years. IN Vy PVE PMT- FV 5d. 5535.000 8.0% amortized over 30 years. N Vy PV- PMTS PV- 5e. $535.000 8.0% amortized over 50 years. Page 8 of 13 Chapter 18 - Packet IN Vy PV: PMT FV 51, $535,000 8.0% with interest only payments. Show work here (think of the interest formulasi 6a. Loan Eligibility Show your work S/S15 Britney and Barney Berceau are seeking a mortgage loan to buy their first home. Barney earns $2,800 per month as a chef. Britney's salary as a payroll accountant is $41.520 per year. Their lender's policy is to limit the monthly principal and interest payment to 28% of the borrower's gross pay. What is the maximum monthly P& 1 payment amount for which Britney and Barney can qualify? Round to whole dollars. Show work here: Pep 6b. Loan Eligibilty --Show your work Pauline Pasteur is looking at a house that is priced at $178,000. She plans on making a $30,000 down payment and feels that her absolute maximum monthly payment for principal and interest is $1,200. Ms. Pasteur seeks a 15-year mortgage which she has seen advertised at 6.25%. Based on her stated limit,can she afford this house? 1st Part: N 2nd Part: Show work here: WY- PV PMT FV Answer: Explain your answer. 6. Monthly Payment -Show your work Page 9 of 13 Chapter 18 - Packet Berdine and Beau Bourgeois have found a house they want to buy. They will need to borrow $169.000 and are now shopping around for a loan. Beau found a 30-year loan at 6.75%, but thinks he can do better. By how much would their monthly payment drop if they could find a loan at a rate that is one-half percentage point lower? 1st Part IN 2nd Part N wy IPV PV PMT PMT FV FV Show work here Answer: 6d. Solve for i-Show your work Find the APR on a $165,000 loan which is amortized over 30 years with a monthly payment of $1,042.91. Round to the nearest 10th of a percent Note: W represents the rote per period (which in this case is monthly). However, since an annual rate is called for, the monthly rate must be converted to the equivalent annuat rate IN What did you calculate for ly? Vy- Annual Rate: rounded to nearest 10th percent PMT- FV: PV 6. Compute the down payment -- Show your work Claire Comeaux wants to buy a house listed at $190,000. The seller has accepted her offer of 5182,000. She plans to amortize the loan over 15 years. Current rates are 8%. How much will Claire have to put down on this house in order to keep her monthly P&I payment at approximately $1,350? Hint: Think in reverse. First find the loan amount (PV). Ist Part: 2nd Part Page 10 of 13 Chapter 18 - Packet Show work here N- Vy PV PMTE FV Answer: Part 7: Additional principal payment - Show your work Shown below is an excerpt from the repayment schedule for Ben Birnbaum's mortgage loan. It was originated on May 1. Interest is paid in arrears. Recall that the interest portion of each payment is based on the outstanding balance during the previous month. For example: $179,890.96 x 085 - $1,274.23"(Interest for month of June, paid on July 1) Birnbaum Loan Repayment Schedule - $180,000 @ 8.5% for 30 years Date Payment 1.Jun 1.Jul 1-Aug 1.Sep $1,384.04 1,384.04 1,384.04 1,384.04 Interest Principal Loan Balance $180,000.00 $1,275.00 $109.06 179890.96** 1274 23 109.81 179,781.15 1273.45 110.59 179,670.56 1272.67 11137 179,559.19 **Balance after the 6/1 payment. June balance. On August 1, along with his regular payment of $1,384.04, Ben also made an additional principal payment of $500. Complete the repayment schedule below to reflect the additional payment. (On September 1, Ben pays the regular monthly amount). More on next page. Note 1: The regular monthly loan payment amount is not affected by the additional principal payment. It will remain the same each month. Note 2: The interest portion of the August 1 payment (paying interest for July) is still based on $179,670.56. Date Payment Interest Principal Loan Balance $180,000.00 1-Jun $1,384.04 $1,275.00 $109.04 179,890-96 Page 11 of 13 Chapter 18 - Packet 109.81 179,781.15 1,27423 1 Aug 1,384.04 1,384.00 +500 extra 1,384.04 1-Sep Show Work Here August: September Part 8: Equity Computation - Show your work Pablo Pecard owned his home for 13 years. As such, he has paid off a significant amount of his original loan. He has also enjoyed a nice appreciation in the value of his home. Indeed, life is good. :) Pablo has now decided to take out a second mortgage in the amount of $65,000. An appraisal was required for the loan application. It is provided below. The interest rate is 6.75%. He chose to amortize it over 15 years. Original Purchase Price: Existing Mortgage: 312 Prescott Street......$165,000 Original Loan: $125,000 7.0% for 30 years Monthly payment: $831.63 Current Appraisal: Current Mortgage Balance: $99,000 Estimated fair market value for the property located at 312 Prescott Street.....$285,000 See questions on next page. 8a. What was Pablo's equity in his house on the date of purchase? NOK Show work here: Page 12 of 13 Chapter 18 - Packet Sb. What is his current equity (before taking the second mortgage)? $ Show work here: 8c. How much equity will he have in the house after taking out the second mortgage? Show work here: Page 13 of 13 Chapter 18 - Packet a Chapter 18 Take Home Packet 1) Solve ALL. problems with a financial calculator (NO annuity formulas) - SHOW ALL WORKI! I recommend printing this document so that you can easily see everything. Then you can enter your answers to submit 2) Read the WORD document first. There are examples in your textbook and the WORD document to help you with this Packet. 3) Please show your work including HOW you calculate the financial keys. No credit can be given if the work is not correct. 4) Be sure to carry all decimals to at least 5 places. Example: Plia has a new mortgage loan for $150,000 at 3.2% for 30 years. How much is her monthly payment? Mortgages in this class are always monthly IN i/v= PV= PMT= FV 30*12=360 3.2/12.26667 150,000 ?? This is how to show your work." Fill in the blanks with the information you know, then solve the problem with your calculator. Finish by typing in your answer in the provided place. Please initial that you have read and understand the instructions Initial in Box 1. 1a. Loan Repayment schedule -- $250,000 @ 7.0% with a 30 year amortization PMT # Monthly Payment Interest Portion Principal Reduction Loan Balance $250,000.00 1 2 N. i/y PV- PMT FV- Page 1 of 13 Chapter 18 - Packet 1b. Loan Repayment schedule -- $250,000 @ 7.0% with a 15 year amortization Principal Reduction PMT Monthly Payment Interest Portion Loan Balance $250,000.00 1 2 Show how you calculated interest, Principal and Loan Balance N. Vy PV PMT= FV 1c. Loan Repayment Schedule - $250,000 @ 7.0% with interest only payments PMT # Monthly Payment Interest Portion Principal Reduction Loan Balance $250,000.00 1 2 INS na Show how you calculated interest. Principal and Loan Balance We na PV- Ina PMT na FV Ina 2. Comparison of a 30-year Amortization vs. 15-year Amortization (3 Parts) Page 2 of 13 Chapter 18 - Packet Repayment Schedule: $250,000 7% for 30 Years Monthly Payment Interest Portion Principal Reduction PMT # 1 204.93 1,663.26 1,663.26 1,663.26 2 Loan Balance $250,000.00 249.795.07 249,588.95 249,381.63 1,458.33 1,457.14 1,455.94 206.12 3 207.32 359 19.21 1,663.26 1,663.26 $598,774 360 1.649.11 0 1,644.05 1649.11 250,000 9.62 Totals 348,774 Repayment Schedule: $250,000 7% for 15 Years Monthly Payment Interest Portion Principal Reduction PMT Loan Balance 1 788.74 2,247.07 2,247.07 2,247.07 2 $250,000.00 249,211.26 248,417.92 247,619.95 1,458,33 1,453.73 1,449.10 793.34 797.97 3 359 2,247.07 2,247.07 25.99 13.03 154,473 360 Totals 2,221.08 2,234.37 250,000 2,234.37 0 $404,473 2a. What is the difference in the monthly payment amount for each loan? Show work here: 2b. What is the difference in the amount of principal paid off with the first payment of each loan? Page 3 of 13 Chapter 18 - Packet VE PV PMT Show work here FV 20 What is the savings, in total interest, over the life of the loan due to the shorter, 15-year amortization vs. WOW!!! $ the 30-year term? Show work here NOTE: Rather than lock into the higher payment required by a 15-year term (that they might have trouble making some borrowers instead opt for the smaller payment of a 30-year amortization and make additional principal payments whenever possible. However, as will be evident In the next problem, they then lose the advantage of lower rates on the shorter-term mortgage. An error message may result if certain inputs are not entered as a negative, meaning you must show your cash out. REMEMBER: In multi-step problems, an intermediate answer is any answer other than the final answer. Never round an intermediate answer unless that amount is to be paid out or it is recorded in the accounting records. For practical reasons, such amounts are then rounded to the nearest cent. Mortgages are always monthly for this class 3. Comparison of a 30-year Amortization vs. a 15-year Amortization (Manual) - 3 parts Part 1: A local bank offers a 7.5% 30-year foued rate mortgage. Assuming a 15% down payment, compute the following for the buyer of a $215,000 house. Amount of the loan (principal amount) Show work here b. Monthly payment amount (P87) N Page 4 of 13 Wye Chapter 18 - Packet PS PMT FVE c. Number of PMT's to be made full term of loan? Show work here d. Total dollar amount of the payments to be made over the full term of the loan? (amount to be paid back) $ Show work here: e. Total amount of principal to be paid back? f. Total amount of Interest to be paid over the full term of the loan? $ Show work here Part 2: Now, shorten the amortization term of the loan to 15 years. Compute: a. New monthly payment amount: N= Vy PV: PMT FV b. Number of PMT's to be made (full term of the loan)? Page 5 of 13 Chapter 18 - Packet R Show work here: c. Describe the relationship between the amortization term and the monthly PMT amount d. Total dollar amount of the payments to be made over the full term of the loan? Show work here: e. Total amount of principal to be paid back 1. Total amount of interest to be paid over the full term of the loan? Show work here Part 3: Compute the savings in TOTAL interest enjoyed by selecting a 15-year amortization rather than a 30-year amortization Show work here: NOTE: This is not to say that a homeowner will keep their mortgage for the duration of the term few do The purpose is to illustrate the benefits of a shorter amortization regardless of the actual loan term Page 6 of 13 3 Chapter 18-Packet 4. Reading and using a Loan Repayment Schedule (Answer the questions regarding the loan repayment schedule presented below) Loan Repayment Schedule - $155,000 5.75% for 15 years Payment Schedule Year 1 Date Payment Interest Principal 1-Aug 1-Sep 1-Oct 1-Nov 1-Dec Totals $54443 547.00 549.66 $1,287.14 $1,287.14 $1,287.14 $1,287.14 $1,287.14 $6,435.70 $742.71 740.1 737.48 734.84 732.2 $3,687.33 Loan Balance 5155,000.00 154,455.57 153,508.53 153,358.87 152 806.57 152,251.63 5523 55494 $2.748 37 Date 1-Jan 1-Feb 1-Mar 1-Apr 1. May 1.Jun 1.Jul 1-Aug 1-Sep 1-Oct 1-Nov 1-Dec Totals Payment $1,287.14 1,287.14 1,287.14 1,287.14 1.287.14 1.287.14 1.287.14 1.287.14 1.287.14 1,287.14 1,287.14 1,287.14 $15.445.68 Payment Schedule Year 2 Interest $729.54 726.87 724.18 721.49 728.77 716.05 713 31 710.57 707.80 705.03 70224 699.43 $8,585.28 Principal $557.60 560.27 562.96 565.65 568.37 571.09 573.83 576 57 579.34 582.11 584.90 587.71 $6.870.40 Loan Balance $151,694,03 151,133.76 150.570.80 150,005.15 149,436.78 148,865.69 148,291.86 147,715.29 147,135.95 146,553.84 145,968.94 145,381.23 Date 1-Jan 1-Feb 1-Mar 1. Apr Payment $1,287.14 1,287.14 1,287.14 1,287.14 Payment Schedule Year 3 Interest $696.62 693.79 690.95 688.09 Principal $590.52 59335 596.19 599.05 Loan Balance $144,790.71 144,197.36 143,601.17 143,002.12 $ 4a. How much principal is paid off with the Oct. 1 payment in Year 1? -11 4b. What is the total amount of interest paid in Year 2? $ 4. In which year will more principal be paid off; Year 2 or Year 3? Year Page 7 of 13 Chapter 18 - Packet 4d. What amount of interest is applicable to July of Year 2? When will the interest charge for January of Year 3 be paid? 5. Compute the monthly payment required to amortize the following loans: 4e. Sa $60,000 4.75% amortized over 15 years. N wy PV PMT FV 5b. $60,000 4.75% amortized over 30 years. IN PV PMT- FV 5c. $112,500 e 5.0% amortized over 15 years. IN Vy PVE PMT- FV 5d. 5535.000 8.0% amortized over 30 years. N Vy PV- PMTS PV- 5e. $535.000 8.0% amortized over 50 years. Page 8 of 13 Chapter 18 - Packet IN Vy PV: PMT FV 51, $535,000 8.0% with interest only payments. Show work here (think of the interest formulasi 6a. Loan Eligibility Show your work S/S15 Britney and Barney Berceau are seeking a mortgage loan to buy their first home. Barney earns $2,800 per month as a chef. Britney's salary as a payroll accountant is $41.520 per year. Their lender's policy is to limit the monthly principal and interest payment to 28% of the borrower's gross pay. What is the maximum monthly P& 1 payment amount for which Britney and Barney can qualify? Round to whole dollars. Show work here: Pep 6b. Loan Eligibilty --Show your work Pauline Pasteur is looking at a house that is priced at $178,000. She plans on making a $30,000 down payment and feels that her absolute maximum monthly payment for principal and interest is $1,200. Ms. Pasteur seeks a 15-year mortgage which she has seen advertised at 6.25%. Based on her stated limit,can she afford this house? 1st Part: N 2nd Part: Show work here: WY- PV PMT FV Answer: Explain your answer. 6. Monthly Payment -Show your work Page 9 of 13 Chapter 18 - Packet Berdine and Beau Bourgeois have found a house they want to buy. They will need to borrow $169.000 and are now shopping around for a loan. Beau found a 30-year loan at 6.75%, but thinks he can do better. By how much would their monthly payment drop if they could find a loan at a rate that is one-half percentage point lower? 1st Part IN 2nd Part N wy IPV PV PMT PMT FV FV Show work here Answer: 6d. Solve for i-Show your work Find the APR on a $165,000 loan which is amortized over 30 years with a monthly payment of $1,042.91. Round to the nearest 10th of a percent Note: W represents the rote per period (which in this case is monthly). However, since an annual rate is called for, the monthly rate must be converted to the equivalent annuat rate IN What did you calculate for ly? Vy- Annual Rate: rounded to nearest 10th percent PMT- FV: PV 6. Compute the down payment -- Show your work Claire Comeaux wants to buy a house listed at $190,000. The seller has accepted her offer of 5182,000. She plans to amortize the loan over 15 years. Current rates are 8%. How much will Claire have to put down on this house in order to keep her monthly P&I payment at approximately $1,350? Hint: Think in reverse. First find the loan amount (PV). Ist Part: 2nd Part Page 10 of 13 Chapter 18 - Packet Show work here N- Vy PV PMTE FV Answer: Part 7: Additional principal payment - Show your work Shown below is an excerpt from the repayment schedule for Ben Birnbaum's mortgage loan. It was originated on May 1. Interest is paid in arrears. Recall that the interest portion of each payment is based on the outstanding balance during the previous month. For example: $179,890.96 x 085 - $1,274.23"(Interest for month of June, paid on July 1) Birnbaum Loan Repayment Schedule - $180,000 @ 8.5% for 30 years Date Payment 1.Jun 1.Jul 1-Aug 1.Sep $1,384.04 1,384.04 1,384.04 1,384.04 Interest Principal Loan Balance $180,000.00 $1,275.00 $109.06 179890.96** 1274 23 109.81 179,781.15 1273.45 110.59 179,670.56 1272.67 11137 179,559.19 **Balance after the 6/1 payment. June balance. On August 1, along with his regular payment of $1,384.04, Ben also made an additional principal payment of $500. Complete the repayment schedule below to reflect the additional payment. (On September 1, Ben pays the regular monthly amount). More on next page. Note 1: The regular monthly loan payment amount is not affected by the additional principal payment. It will remain the same each month. Note 2: The interest portion of the August 1 payment (paying interest for July) is still based on $179,670.56. Date Payment Interest Principal Loan Balance $180,000.00 1-Jun $1,384.04 $1,275.00 $109.04 179,890-96 Page 11 of 13 Chapter 18 - Packet 109.81 179,781.15 1,27423 1 Aug 1,384.04 1,384.00 +500 extra 1,384.04 1-Sep Show Work Here August: September Part 8: Equity Computation - Show your work Pablo Pecard owned his home for 13 years. As such, he has paid off a significant amount of his original loan. He has also enjoyed a nice appreciation in the value of his home. Indeed, life is good. :) Pablo has now decided to take out a second mortgage in the amount of $65,000. An appraisal was required for the loan application. It is provided below. The interest rate is 6.75%. He chose to amortize it over 15 years. Original Purchase Price: Existing Mortgage: 312 Prescott Street......$165,000 Original Loan: $125,000 7.0% for 30 years Monthly payment: $831.63 Current Appraisal: Current Mortgage Balance: $99,000 Estimated fair market value for the property located at 312 Prescott Street.....$285,000 See questions on next page. 8a. What was Pablo's equity in his house on the date of purchase? NOK Show work here: Page 12 of 13 Chapter 18 - Packet Sb. What is his current equity (before taking the second mortgage)? $ Show work here: 8c. How much equity will he have in the house after taking out the second mortgage? Show work here: Page 13 of 13