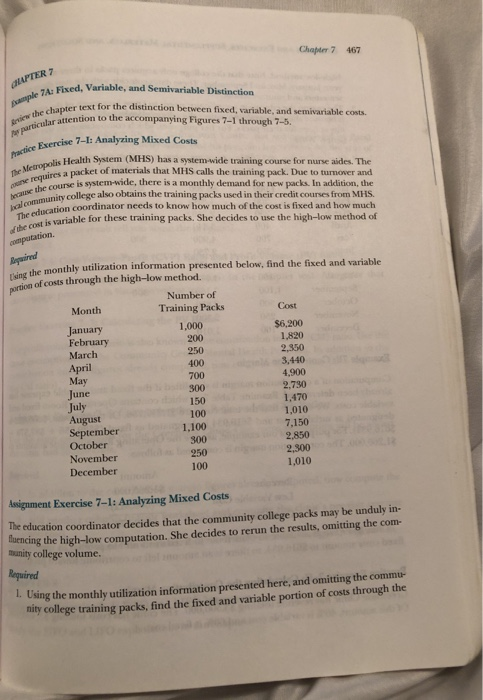

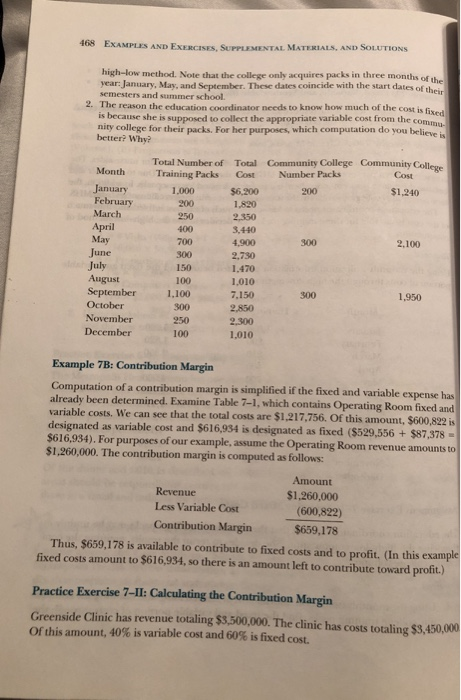

Chapter 7467 CHAPTER 7 ed, Variable, and Semivariable Distinction pample 7A: Fixed, text for the distinction between fixed, variable, and semivariable costs. Arview the r ho lar attention to the accompanying Figures 7-1 through 7-5. Exercise 7-I: Analyzing Mixed Costs Health System (MHS) has a system-wide training course for nurse aides. The eres a packet of materials that MHS calls the training pack. Due to turnover and bal community nmunity college also obtains the training packs used in their credit courses from MHS. The education Th cost is variable for these training packs. She decides to use the high-low method of coordinator needs to know how much of the cost is fixed and how much af the Using the monthly utilization information ion information presented below, find the fixed and variable Number of Month Training Packs Cost January February March 1,000 200 1,820 2,350 250 April May 400 3,440 4,900 2,730 1,470 1,010 7,150 700 June ul 300 150 100 1,100 300 250 100 September October November December 2,850 2,300 1,010 Asignment Exercise 7-1: Analyzing Mixed Costs The education coordinator decides that the community college packs may be unduly in- uencing the high-low computation. She decides to rerun the results, omitting the com- munity college volume. L. Using the monthly utilization information presented here, and omitting the commu- y college training packs, find the fixed and variable portion of costs through the Using the 468 EXAMPLES AND EXERCISES SUPPLEMENTAL MATERIALS AND SOLUTIONS high-low method. Note that the college only acquires packs in three months of the year: January, May, and September. These dates coincide with the start dates of the semesters and summer school ir 2. The reason the education coordinator needs to know how much of the cost is fixed is because she is supposed to collect the appropriate variable cost from the commu nity college for their packs. For her purposes, which computation do you believeis better? Why? Total Number of Total Community College Community Colleve Training Packs Cost Number Packs Cost Month $1,240 200 January 1,000 1,820 200 March 2,350 3,440 2,100 300 May 700 4,900 June July August September 00 300 2,730 1.470 100 1,010 1,950 300 7.150 2,850 November 250 2.300 December 100 1,010 Example 7B: Contribution Margin Computation of a contribution margin is simplified if the fixed and variable already been determined. Examine Table 7-1, which contains Operating Room fixed and variable costs. We can see that the total costs are $1,217.756. Of this amount, $600,822 is designated as variable cost and $616,934 is designated as fixed ($529,556+$87,378 $616,934). For purposes of our example, assume the Operating Room revenue amounts to $1,260,000. The contribution margin is computed as follows: expense has Amount Revenue $1,260,000 (600,822) Less Variable Cost Contribution Margin $659,178 Thus, $659,178 is available to contribute to fixed costs and to profit. (In this example fixed costs amount to $616,934, so there is an amount left to contribute toward profit.) Practice Exercise 7-II: Calculating the Contribution Margin Greenside Clinic has revenue totaling $3,500,000. The clinic has costs totaling $3,450,00 Of this amount, 40% is variable cost and 60% is fixed cost. Chapler 8 469 e the contribution margin for Greenside Clinic. compute t Exercise 7-2: Calculating the Contribution Margin Mental Health program for the l The program director determines that his program has revenue for the Community Center The has just completed its fiscal r n,000. believes his variable expense amounts to $205,000 and he knows his fixed expense amounts to $1,100,000 Required mpute the contribution margin for the Community Center Mental Health Program 2. What does the result tell you about the program? e-Profit (CVP) Ratio and Profit-Volume (PV) Ratio Example 7-3: Cost-Volum Closely review the examples of ratio calculations in the chapter text. Also note that examples are presented in visuals as well as text. Practice Exercise 7-3: Calculating the PV Ratio The profit-volume (PV) ratio is also known as the contribution margin (CM) ratio. Use the same assumptions for the Community Center Mental Health Program. In addition to the contribution margin figures already computed, now compute the PV ratio (also known as the CM ratio). Assignment Exercise 7-3: Calculating the PV Ratio and the CVP Ratio Use the same assumptions for the Greenside Clinic. One more assumption will be added: the clinic had 35,000 visits. Required 1. In addition to the contribution margin figures already computed, now compute the PV ratio (also known as the CM ratio). 2. Add another column to your worksheet and compute the clinic's per-visit revenue and costs 3. Create a Cost-Volume-Profit chart. Refer to the chapter text along with Figure 7-6