Answered step by step

Verified Expert Solution

Question

1 Approved Answer

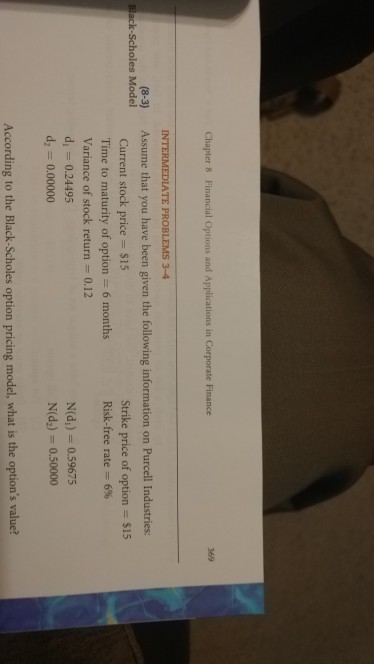

Chapter 8 Financial Options and Applications in Corporate Finance 369 INTERMEDIATE PROBLEMS 3-4 (8-3) Assume that you have been given the following information on Purcell

Chapter 8 Financial Options and Applications in Corporate Finance 369 INTERMEDIATE PROBLEMS 3-4 (8-3) Assume that you have been given the following information on Purcell Industries: ack-Scholes Model Current stock price $15 Time to maturity of option = 6 months Variance of stock return = 0.12 d, 0.24495 Strike price of option Risk-free rate = 6% $15 N(d) = 0.59675 N(d) = 0.50000 0.00000 According to the Black-Scholes option pricing model, what is the option's value

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management for Public, Health and Not-for-Profit Organizations

Authors: Steven A. Finkler, Daniel L. Smith, Thad D. Calabrese, Robert M. Purtell

5th edition

1506326846, 9781506326863, 1506326862, 978-1506326849