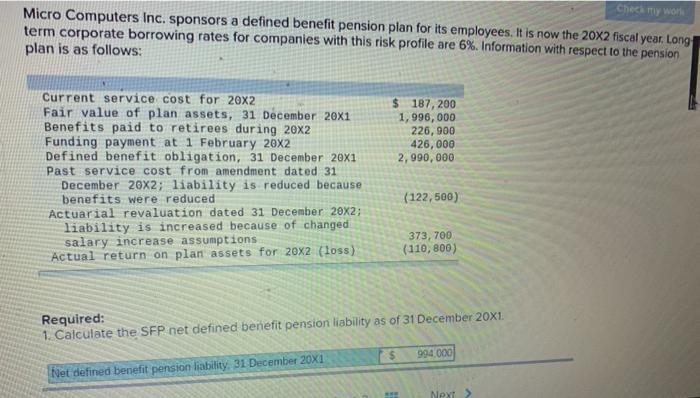

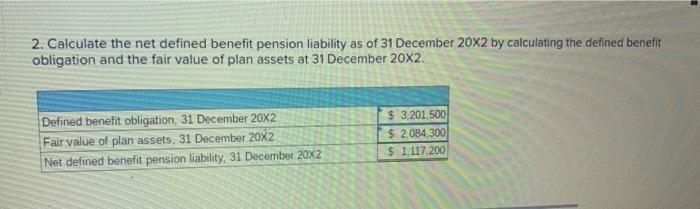

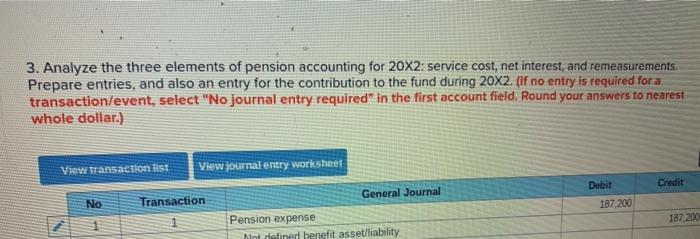

Check my word Micro Computers Inc. sponsors a defined benefit pension plan for its employees. It is now the 20x2 fiscal year, Long term corporate borrowing rates for companies with this risk profile are 6%. Information with respect to the pension plan is as follows: $ 187,200 1,990,000 226, 900 426,000 2,990,000 Current service cost for 20x2 Fair value of plan assets, 31 December 20x1 Benefits paid to retirees during 20x2 Funding payment at 1 February 20X2 Defined benefit obligation, 31 December 20x1 Past service cost from amendment dated 31 December 20X2; liability is reduced because benefits were reduced Actuarial revaluation dated 31 December 20X2; liability is increased because of changed salary increase assumptions Actual return on plan assets for 20x2 (loss) (122,500) 373, 700 (110,800) Required: 1. Calculate the SFP net defined benefit pension liability as of 31 December 20X1. 15 994.000 Net defined benefit pension liability. 31 December 20X1 Next 2. Calculate the net defined benefit pension liability as of 31 December 20X2 by calculating the defined benefit obligation and the fair value of plan assets at 31 December 20x2. Defined benefit obligation, 31 December 20X2 Fair value of plan assets, 31 December 20X2 Net defined benefit pension liability, 31 December 20X2 $ 3.201 500 $ 2,084,300 $ 1.117 200 3. Analyze the three elements of pension accounting for 20X2: service cost, net interest, and remeasurements. Prepare entries, and also an entry for the contribution to the fund during 20X2. (if no entry is required for a transactionlevent, select "No journal entry required" in the first account field. Round your answers to nearest whole dollar.) View transaction list View journal entry worksheet Credit General Journal Debit 187 200 No Transaction 187,200 Pension expense Mint rafiner benefit asset/liability Check my word Micro Computers Inc. sponsors a defined benefit pension plan for its employees. It is now the 20x2 fiscal year, Long term corporate borrowing rates for companies with this risk profile are 6%. Information with respect to the pension plan is as follows: $ 187,200 1,990,000 226, 900 426,000 2,990,000 Current service cost for 20x2 Fair value of plan assets, 31 December 20x1 Benefits paid to retirees during 20x2 Funding payment at 1 February 20X2 Defined benefit obligation, 31 December 20x1 Past service cost from amendment dated 31 December 20X2; liability is reduced because benefits were reduced Actuarial revaluation dated 31 December 20X2; liability is increased because of changed salary increase assumptions Actual return on plan assets for 20x2 (loss) (122,500) 373, 700 (110,800) Required: 1. Calculate the SFP net defined benefit pension liability as of 31 December 20X1. 15 994.000 Net defined benefit pension liability. 31 December 20X1 Next 2. Calculate the net defined benefit pension liability as of 31 December 20X2 by calculating the defined benefit obligation and the fair value of plan assets at 31 December 20x2. Defined benefit obligation, 31 December 20X2 Fair value of plan assets, 31 December 20X2 Net defined benefit pension liability, 31 December 20X2 $ 3.201 500 $ 2,084,300 $ 1.117 200 3. Analyze the three elements of pension accounting for 20X2: service cost, net interest, and remeasurements. Prepare entries, and also an entry for the contribution to the fund during 20X2. (if no entry is required for a transactionlevent, select "No journal entry required" in the first account field. Round your answers to nearest whole dollar.) View transaction list View journal entry worksheet Credit General Journal Debit 187 200 No Transaction 187,200 Pension expense Mint rafiner benefit asset/liability