Answered step by step

Verified Expert Solution

Question

1 Approved Answer

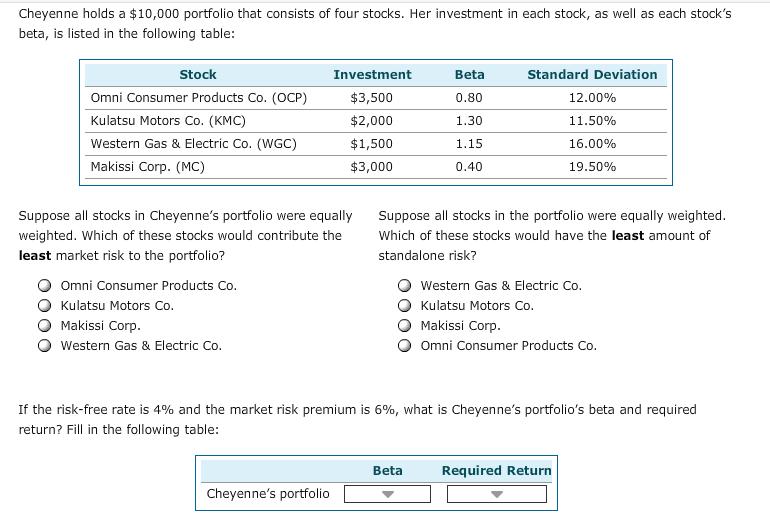

Cheyenne holds a $10,000 portfolio that consists of four stocks. Her investment in each stock, as well as each stock's beta, is listed in

Cheyenne holds a $10,000 portfolio that consists of four stocks. Her investment in each stock, as well as each stock's beta, is listed in the following table: Stock Investment Beta Standard Deviation Omni Consumer Products Co. (OCP) $3,500 0.80 12.00% Kulatsu Motors Co. (KMC) $2,000 1.30 11.50% $1,500 1.15. 16.00% Western Gas & Electric Co. (WGC) Makissi Corp. (MC) $3,000 0.40 19.50% Suppose all stocks in Cheyenne's portfolio were equally weighted. Which of these stocks would contribute the least market risk to the portfolio? Suppose all stocks in the portfolio were equally weighted. Which of these stocks would have the least amount of standalone risk? Omni Consumer Products Co. Western Gas & Electric Co. Kulatsu Motors Co. Kulatsu Motors Co. Makissi Corp. Makissi Corp. Western Gas & Electric Co. Omni Consumer Products Co. If the risk-free rate is 4% and the market risk premium is 6%, what is Cheyenne's portfolio's beta and required return? Fill in the following table: Beta Required Return Cheyenne's portfolio

Step by Step Solution

★★★★★

3.33 Rating (156 Votes )

There are 3 Steps involved in it

Step: 1

a Least market risk is the lowest beta Makissi Corp b Lea...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Data Analysis And Decision Making

Authors: Christian Albright, Wayne Winston, Christopher Zappe

4th Edition

538476125, 978-0538476126