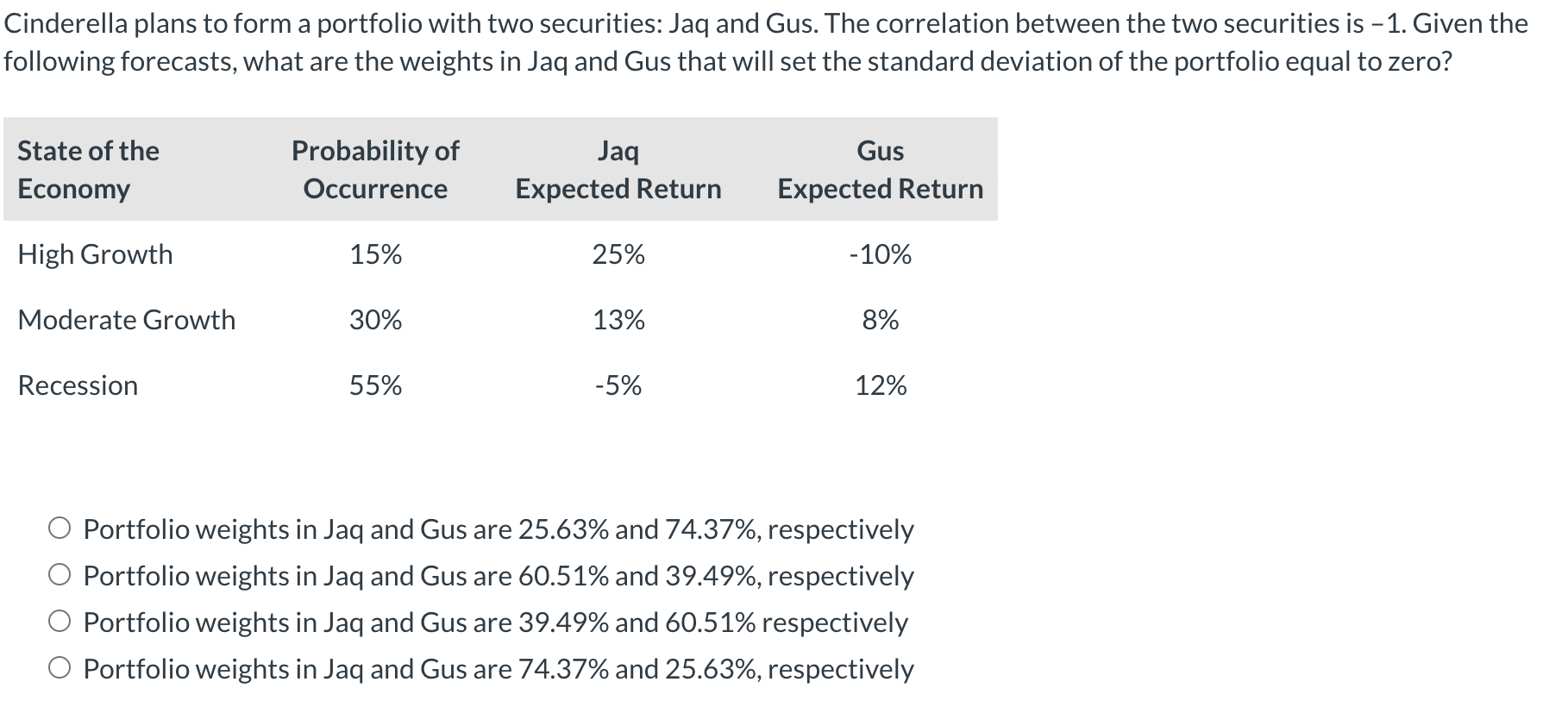

Cinderella plans to form a portfolio with two securities: Jaq and Gus. The correlation between the two securities is -1. Given the following forecasts,

Cinderella plans to form a portfolio with two securities: Jaq and Gus. The correlation between the two securities is -1. Given the following forecasts, what are the weights in Jaq and Gus that will set the standard deviation of the portfolio equal to zero? State of the Economy Probability of Occurrence Jaq Expected Return Gus Expected Return High Growth 15% 25% -10% Moderate Growth 30% 13% 8% Recession 55% -5% 12% Portfolio weights in Jaq and Gus are 25.63% and 74.37%, respectively Portfolio weights in Jaq and Gus are 60.51% and 39.49%, respectively Portfolio weights in Jaq and Gus are 39.49% and 60.51% respectively Portfolio weights in Jaq and Gus are 74.37% and 25.63%, respectively

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To make the standard deviation of a portfolio zero with two perfectly negatively correlated securiti...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Damu Winston Mba

1st Edition

1734182512, 978-1734182514