Answered step by step

Verified Expert Solution

Question

1 Approved Answer

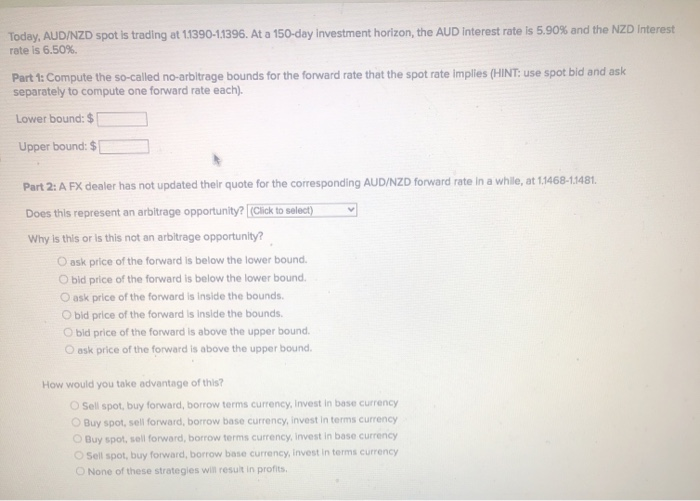

click to select option (Yes,no, not enough info) Today, AUD/NZD spot is trading at 11390-11396. At a 150-day Investment horizon, the AUD Interest rate is

click to select option (Yes,no, not enough info)

click to select option (Yes,no, not enough info)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Financial Planning And Control

Authors: Robert P. Greenwood

3rd Edition

0566083728, 978-0566083723