Answered step by step

Verified Expert Solution

Question

1 Approved Answer

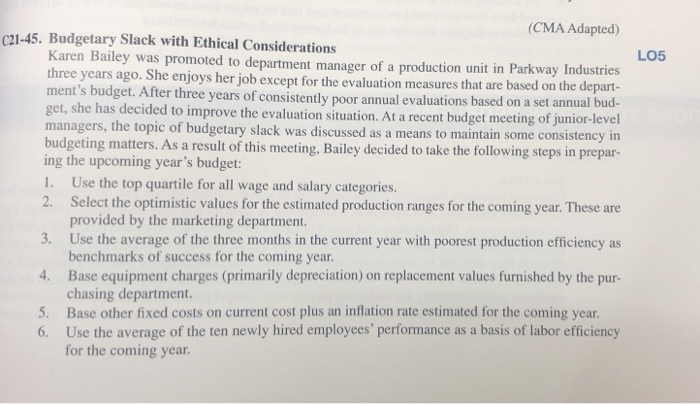

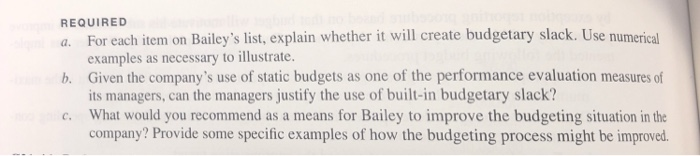

(CMA Adapted) C21-45. Budgetary Slack with Ethical Considerations Karen Bailey was promoted to department manager of a production unit in Parkway Indus three years ago.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Electronic Working Papers For Needles Powers Crossons Financial And Managerial Accounting 9th And Crosson Needles Managerial Accounting

Authors: Susan V. Crosson, Belverd E. Needles

9th Edition

0538791918, 978-0538791915