Answered step by step

Verified Expert Solution

Question

1 Approved Answer

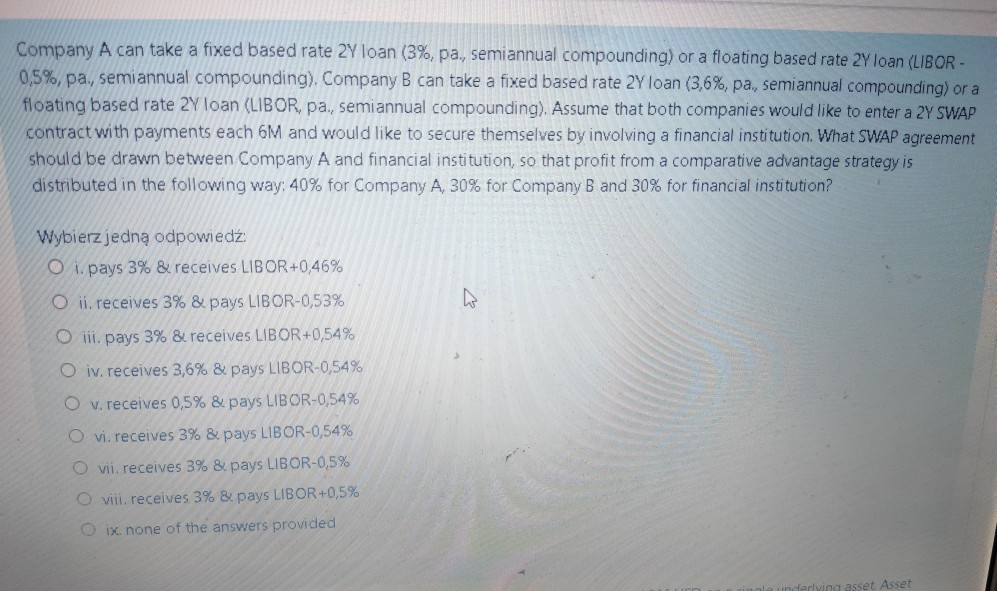

Company A can take a fixed based rate 2Y loan (3%, pa., semiannual compounding) or a floating based rate 2Y loan (LIBOR- 0,5%, pa., semiannual

Company A can take a fixed based rate 2Y loan (3%, pa., semiannual compounding) or a floating based rate 2Y loan (LIBOR- 0,5%, pa., semiannual compounding). Company B can take a fixed based rate 2Y loan (3,6%, pa, semiannual compounding) or a floating based rate 2Y loan (LIBOR, pa, semiannual compounding). Assume that both companies would like to enter a 2Y SWAP contract with payments each 6M and would like to secure themselves by involving a financial institution. What SWAP agreement should be drawn between Company A and financial institution, so that profit from a comparative advantage strategy is distributed in the following way: 40% for Company A, 30% for Company B and 30% for financial institution? Wybierz jedn odpowied: O pays 3% & receives LIBOR+0,46% O ii. receives 3% & pays LIBOR-0,53% O pays 3% & receives LIBOR+0,54% O iv. receives 3,6% & pays LIBOR-0,54% O v. receives 0,5% & pays LIBOR-0,54% O vi. receives 3% & pays LIBOR-0,54% O vii, receives 3% 8 pays LIBOR-0,5% O viii, receives 3% & pays LIBOR +0,5% Oix none of the answers provided asset Asset

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: Robert Libby

6th Edition

0077405641, 978-0077405649