Answered step by step

Verified Expert Solution

Question

1 Approved Answer

COMPLETE IN R , should not be done in chat GPT / use complex code A life insurance company is pricing a new policy to

COMPLETE IN R should not be done in chat GPTuse complex code

A life insurance company is pricing a new policy to sell to a group of yearold male nonsmokers. They determine that the probability that a member of this group will die X years from the day they purchase the policy can be modeled with a Weibull distribution with shape parameter and scale parameter measured in years. The term of the policy is years. At the end of every month, policyholders PH are expected to pay a premium of $ If a PH in good standing dies during the term of the policy, his beneficiaries receive a benefit of $ at the end of that month. Every month there is a chance that the policy holder will let the policy lapse ie he will permanently stop paying premiums and forfeit his right to the benefit The insurance company calculates cost of funds using a rate of compounding monthly.

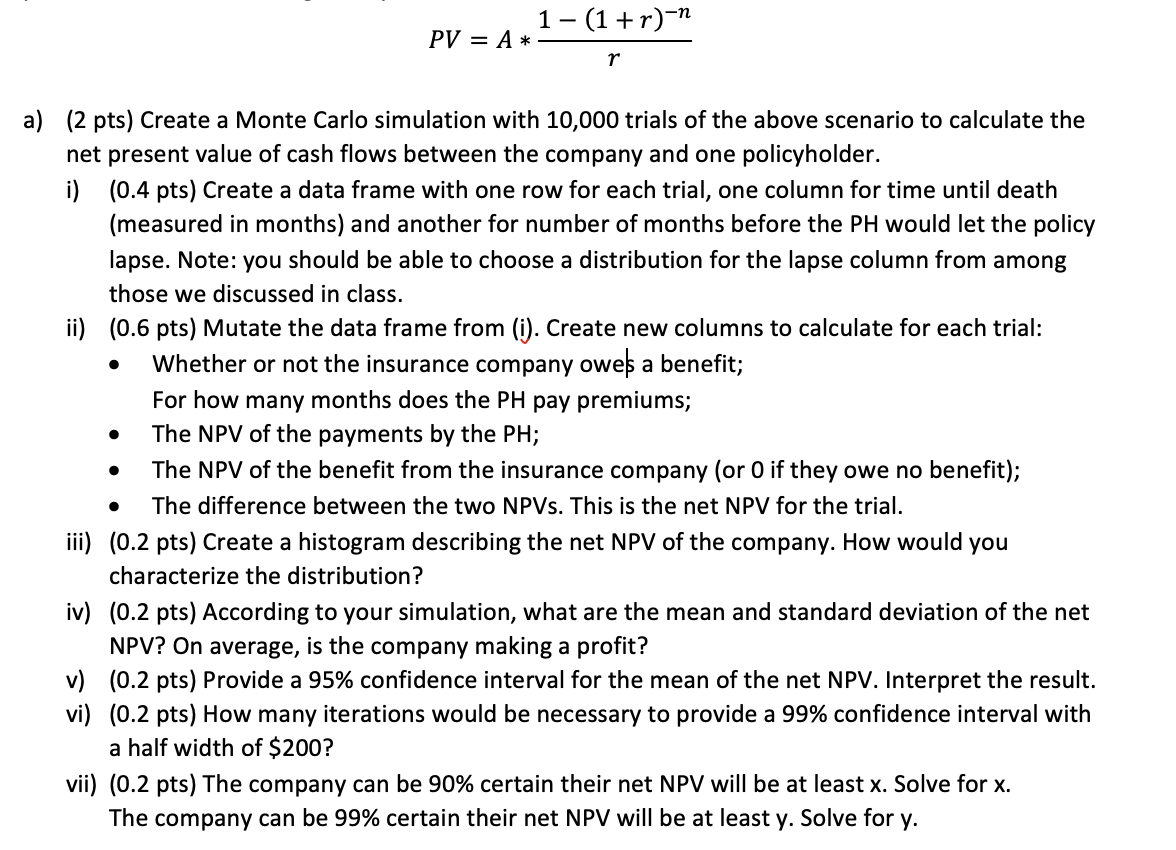

Hint: The formula for the present value of n payments of size A at the end of each period with a per period interest rate of r is given by

PVArnr

a pts Create a Monte Carlo simulation with trials of the above scenario to calculate the

net present value of cash flows between the company and one policyholder.

i pts Create a data frame with one row for each trial, one column for time until death

measured in months and another for number of months before the PH would let the policy

lapse. Note: you should be able to choose a distribution for the lapse column from among

those we discussed in class.

ii pts Mutate the data frame from i Create new columns to calculate for each trial:

Whether or not the insurance company owes a benefit;

For how many months does the pay premiums;

The NPV of the payments by the PH;

The NPV of the benefit from the insurance company or if they owe no benefit;

The difference between the two NPVs This is the net NPV for the trial.

iii pts Create a histogram describing the net NPV of the company. How would you

characterize the distribution?

iv pts According to your simulation, what are the mean and standard deviation of the net

NPV On average, is the company making a profit?

v pts Provide a confidence interval for the mean of the net NPV Interpret the result.

vi pts How many iterations would be necessary to provide a confidence interval with

a half width of $

vii pts The company can be certain their net NPV will be at least Solve for

The company can be certain their net NPV will be at least Solve for

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Financial Management

Authors: Don Cyr, Alfred Kahl, William Rentz, R. Moyer

1st Edition

017616992X, 978-0176169923