Answered step by step

Verified Expert Solution

Question

1 Approved Answer

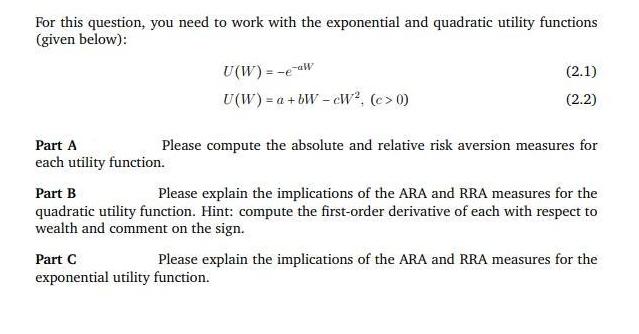

For this question, you need to work with the exponential and quadratic utility functions (given below): Part A each utility function. U(W) = -e-aw

For this question, you need to work with the exponential and quadratic utility functions (given below): Part A each utility function. U(W) = -e-aw U(W) = a + bWcW, (c> 0) Please compute the absolute and relative risk aversion measures for (2.1) (2.2) Part B Please explain the implications of the ARA and RRA measures for the quadratic utility function. Hint: compute the first-order derivative of each with respect to wealth and comment on the sign. Part C exponential utility function. Please explain the implications of the ARA and RRA measures for the

Step by Step Solution

★★★★★

3.29 Rating (149 Votes )

There are 3 Steps involved in it

Step: 1

Part A For the exponential utility function UW e aW by taking detivative dUdW d eaW dUdW a e aW double derivating d 2 UdW 2 da e aW d 2 UdW 2 a de aW d 2 UdW 2 a a e aW a 2 e aW i The absolute risk av...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Calculus Early Transcendentals

Authors: William L. Briggs, Lyle Cochran, Bernard Gillett

2nd edition

321954428, 321954424, 978-0321947345