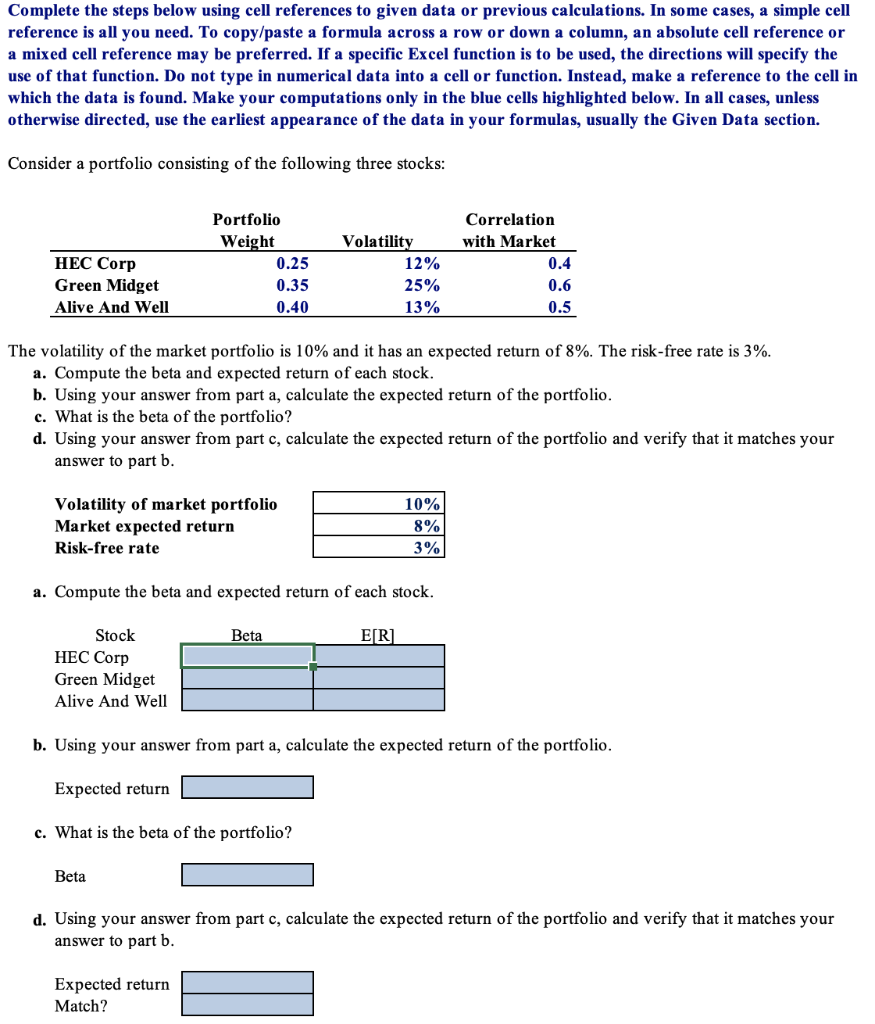

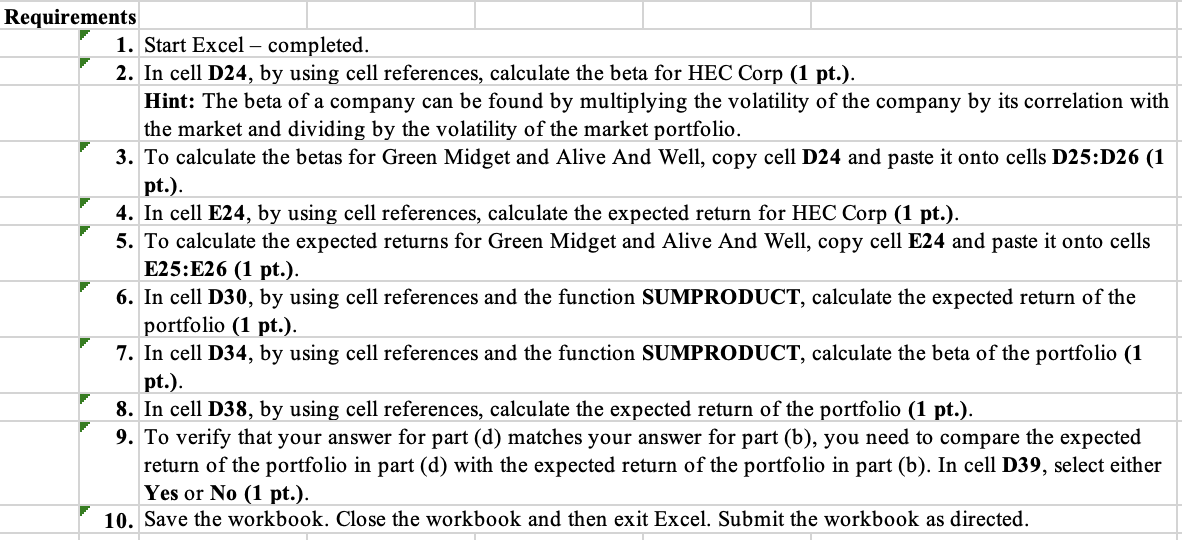

Complete the steps below using cell references to given data or previous calculations. In some cases, a simple cell reference is all you need. To copy/paste a formula across a row or down a column, an absolute cell reference or a mixed cell reference may be preferred. If a specific Excel function is to be used, the directions will specify the use of that function. Do not type in numerical data into a cell or function. Instead, make a reference to the cell in which the data is found. Make your computations only in the blue cells highlighted below. In all cases, unless otherwise directed, use the earliest appearance of the data in your formulas, usually the Given Data section. Consider a portfolio consisting of the following three stocks: HEC Corp Green Midget Alive And Well Portfolio Weight 0.25 0.35 0.40 Volatility 12% 25% 13% Correlation with Market 0.4 0.6 0.5 The volatility of the market portfolio is 10% and it has an expected return of 8%. The risk-free rate is 3%. a. Compute the beta and expected return of each stock. b. Using your answer from part a, calculate the expected return of the portfolio. c. What is the beta of the portfolio? d. Using your answer from part c, calculate the expected return of the portfolio and verify that it matches your answer to part b. Volatility of market portfolio Market expected return Risk-free rate 10% 8% 3% a. Compute the beta and expected return of each stock. Beta E[R] Stock HEC Corp Green Midget Alive And Well b. Using your answer from part a, calculate the expected return of the portfolio. Expected return c. What is the beta of the portfolio? Beta d. Using your answer from part c, calculate the expected return of the portfolio and verify that it matches your answer to part b. Expected return Match? Requirements 1. Start Excel - completed. 2. In cell D24, by using cell references, calculate the beta for HEC Corp (1 pt.). Hint: The beta of a company can be found by multiplying the volatility of the company by its correlation with the market and dividing by the volatility of the market portfolio. 3. To calculate the betas for Green Midget and Alive And Well, copy cell D24 and paste it onto cells D25:D26 (1 pt.). 4. In cell E24, by using cell references, calculate the expected return for HEC Corp (1 pt.). 5. To calculate the expected returns for Green Midget and Alive And Well, copy cell E24 and paste it onto cells E25:E26 (1 pt.). 6. In cell D30, by using cell references and the function SUMPRODUCT, calculate the expected return of the portfolio (1 pt.). 7. In cell D34, by using cell references and the function SUMPRODUCT, calculate the beta of the portfolio (1 pt.). 8. In cell D38, by using cell references, calculate the expected return of the portfolio (1 pt.). 9. To verify that your answer for part (d) matches your answer for part (b), you need to compare the expected return of the portfolio in part (d) with the expected return of the portfolio in part (b). In cell D39, select either Yes or No (1 pt.). 10. Save the workbook. Close the workbook and then exit Excel. Submit the workbook as directed