Comprehensive Accounting Cycle Review 11-1 (Part Level Submission)

Culver Corporations balance sheet at December 31, 2016, is presented below.

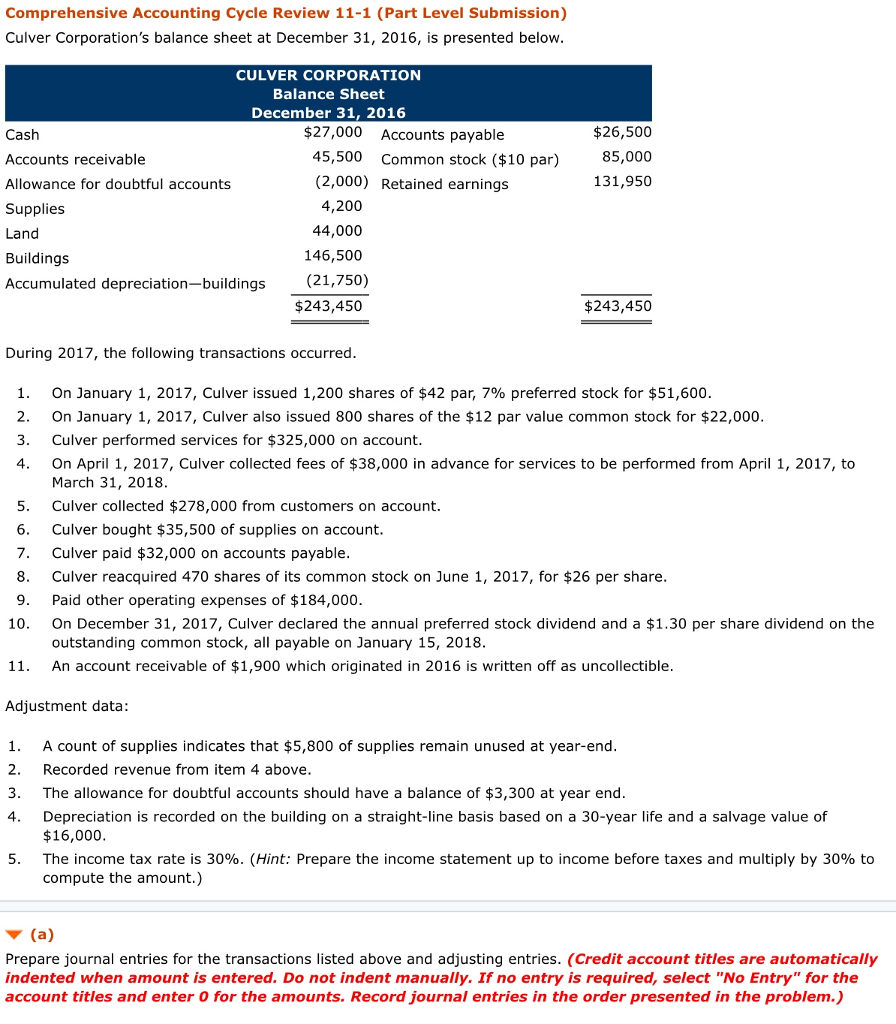

Comprehensive Accounting Cycle Review 11-1 (Part Level Submission) Culver Corporation's balance sheet at December 31, 2016, is presented below CULVER CORPORATION Balance Sheet December 31, 2016 $27,000 Accounts payable $26,500 85,000 131,950 Cash Accounts receivable Allowance for doubtful accounts Supplies Land Buildings 45,500 Common stock ($10 par) (2,000) Retained earnings 4,200 44,000 146,500 Accumulated depreciation-buildings (21,750) $243,450 $243,450 During 2017, the following transactions occurred I. On January 1, 2017, Culver issued 1,200 shares of $42 par, 7% preferred stock for $51,600. 2. On January 1, 2017, Culver also issued 800 shares of the $12 par value common stock for $22,000 3. Culver performed services for $325,000 on account. 4. On April 1, 2017, Culver collected fees of $38,000 in advance for services to be performed from April 1, 2017, teo 5. 6. 7. 8. 9. 10. March 31, 2018 Culver collected $278,000 from customers on account. Culver bought $35,500 of supplies on account Culver paid $32,000 on accounts payable Culver reacquired 470 shares of its common stock on June 1, 2017, for $26 per share Paid other operating expenses of $184,000 On December 31, 2017, Culver declared the annual preferred stock dividend and a $1.30 per share dividend on the outstanding common stock, all payable on January 15, 2018 An account receivable of $1,900 which originated in 2016 is written off as uncollectible 11. Adjustment data 1. A count of supplies indicates that $5,800 of supplies remain unused at year-end 2. Recorded revenue from item 4 above 3. The allowance for doubtful accounts should have a balance of $3,300 at year end 4. Depreciation is recorded on the building on a straight-line basis based on a 30-year life and a salvage value of $16,000 The income tax rate is 30%. (Hint: Prepare the income statement up to income before taxes and multiply by 30% to compute the amount.) 5. Prepare journal entries for the transactions listed above and adjusting entries. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts. Record journal entries in the order presented in the problem.)