Answered step by step

Verified Expert Solution

Question

1 Approved Answer

compute the global minimum variance protfolio (gmvp) using the sample variance-covariance matrix 10 BISA . DES . C18 G H 1 BP 100% S .00

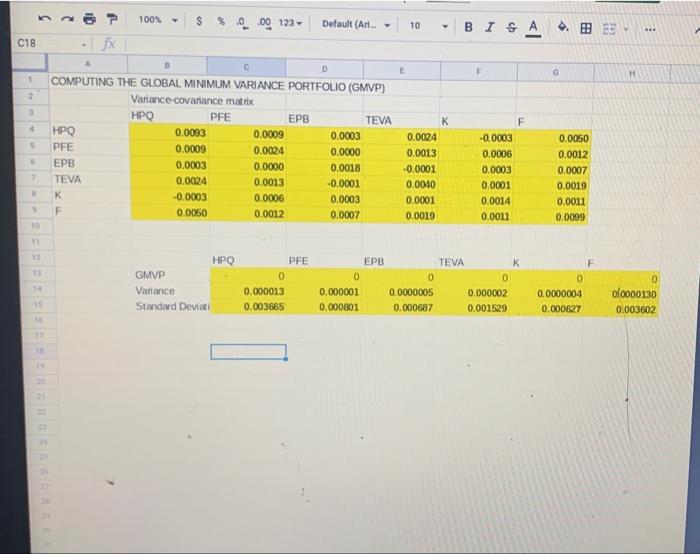

compute the global minimum variance protfolio (gmvp) using the sample variance-covariance matrix

10 BISA . DES . C18 G H 1 BP 100% S .00 123 Default (Art. fx D COMPUTING THE GLOBAL MINIMUM VARIANCE PORTFOLIO (GMVP) Variance covariance matrix HPO PFE EPB TEVA HPO 0.0093 0.0009 0.0003 PFE 0.0009 0.0024 0.0000 EPB 0.0003 0.0000 0.0018 TEVA 0.0024 0.0013 -0.0001 K -0.0003 0.0006 0.0003 0.0050 0.0012 0.0007 5 K 0.0024 0.0013 -0.0001 0.0040 0.0001 0.0019 F -0.0003 0.0006 0.0003 0.0001 0.0014 0.0011 7 0.0050 0.0012 0.0007 0.0019 0.0011 0.0099 m 10 11 13 1 PFE 0 HPO GMVP Variance Standard Deviat EPB TEVA 0 0 0 0.000001 0.0000005 0.000002 0.000801 0.000687 0.001529 0.000013 0.003665 0 0.0000004 0.000627 0 0.0000130 0.003602 10 BISA . DES . C18 G H 1 BP 100% S .00 123 Default (Art. fx D COMPUTING THE GLOBAL MINIMUM VARIANCE PORTFOLIO (GMVP) Variance covariance matrix HPO PFE EPB TEVA HPO 0.0093 0.0009 0.0003 PFE 0.0009 0.0024 0.0000 EPB 0.0003 0.0000 0.0018 TEVA 0.0024 0.0013 -0.0001 K -0.0003 0.0006 0.0003 0.0050 0.0012 0.0007 5 K 0.0024 0.0013 -0.0001 0.0040 0.0001 0.0019 F -0.0003 0.0006 0.0003 0.0001 0.0014 0.0011 7 0.0050 0.0012 0.0007 0.0019 0.0011 0.0099 m 10 11 13 1 PFE 0 HPO GMVP Variance Standard Deviat EPB TEVA 0 0 0 0.000001 0.0000005 0.000002 0.000801 0.000687 0.001529 0.000013 0.003665 0 0.0000004 0.000627 0 0.0000130 0.003602 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of Post Crisis Financial Modelling

Authors: Emmanuel Haven, Philip Molyneux, John Wilson, Sergei Fedotov, Meryem Duygun

1st Edition

1137494484, 978-1137494481