Answered step by step

Verified Expert Solution

Question

1 Approved Answer

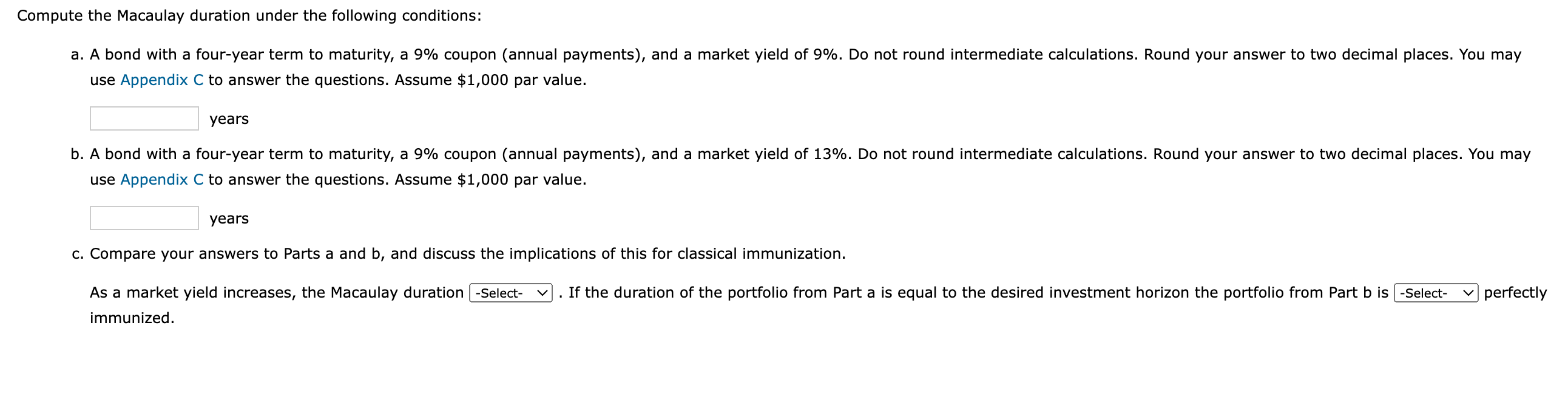

Compute the Macaulay duration under the following conditions: a . A bond with a four - year term to maturity, a 9 % coupon (

Compute the Macaulay duration under the following conditions:

a A bond with a fouryear term to maturity, a coupon annual payments and a market yield of Do not round intermediate calculations. Round your answer to two decimal places. You may

use Appendix to answer the questions. Assume $ par value.

years

b A bond with a fouryear term to maturity, a coupon annual payments and a market yield of Do not round intermediate calculations. Round your answer to two decimal places. You may

use Appendix to answer the questions. Assume $ par value.

years

c Compare your answers to Parts a and and discuss the implications of this for classical immunization.

As a market yield increases, the Macaulay duration

immunized.

If the duration of the portfolio from Part is equal to the desired investment horizon the portfolio from Part is

perfectly

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Oxford Handbook Of Private Equity

Authors: Douglas Cumming

1st Edition

0195391586, 978-0195391589