Answered step by step

Verified Expert Solution

Question

1 Approved Answer

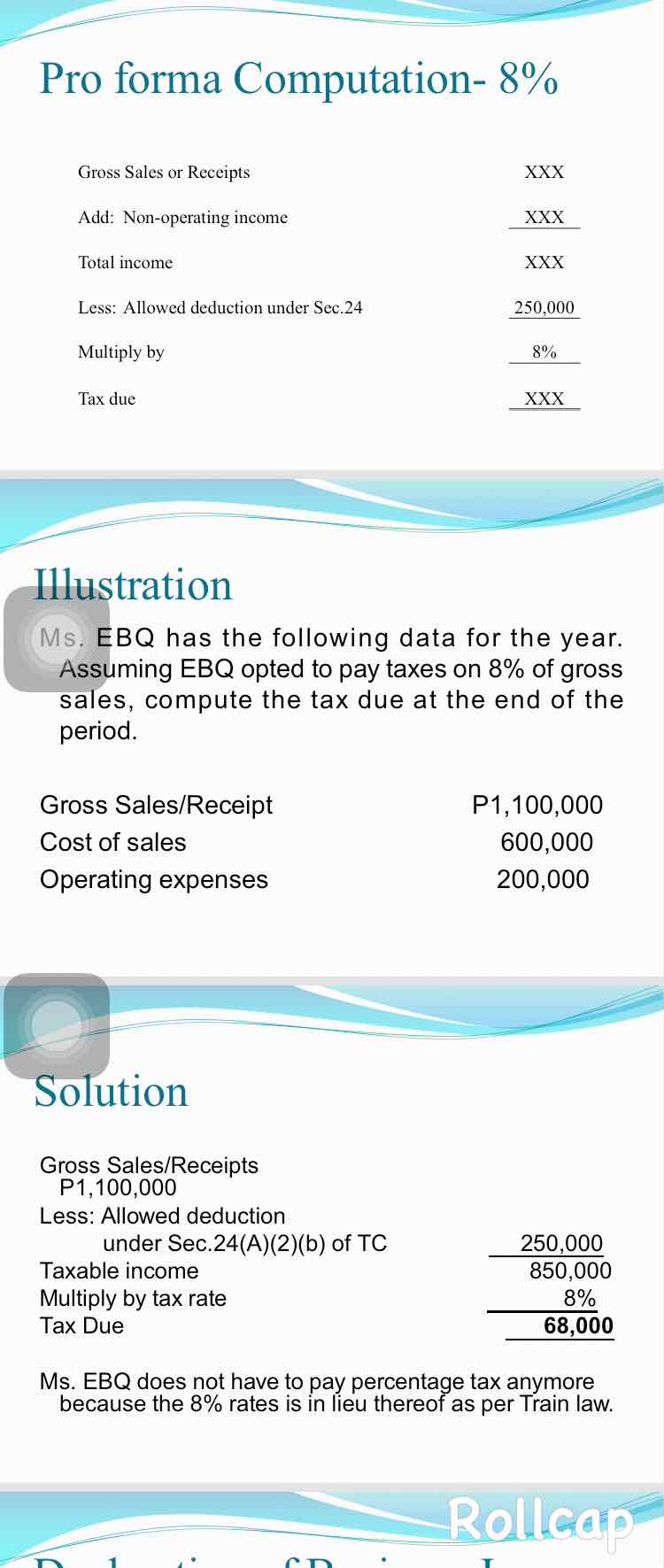

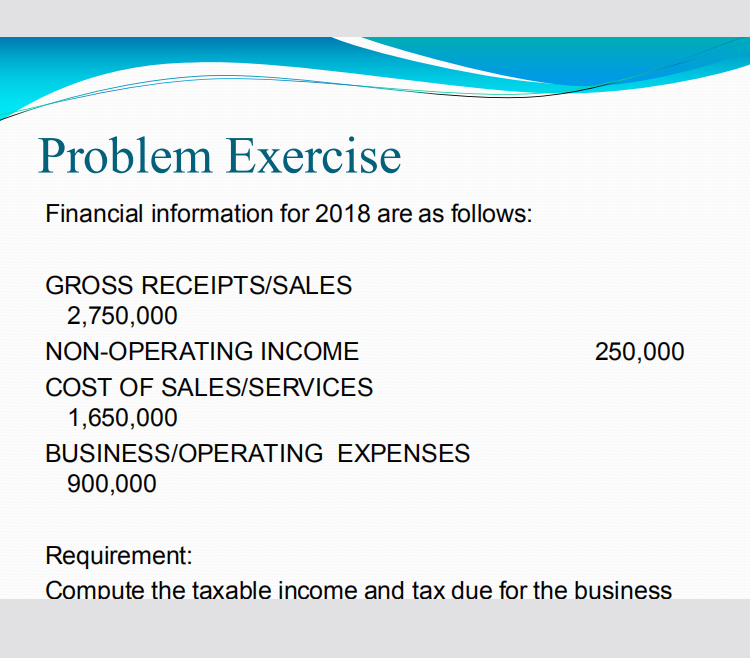

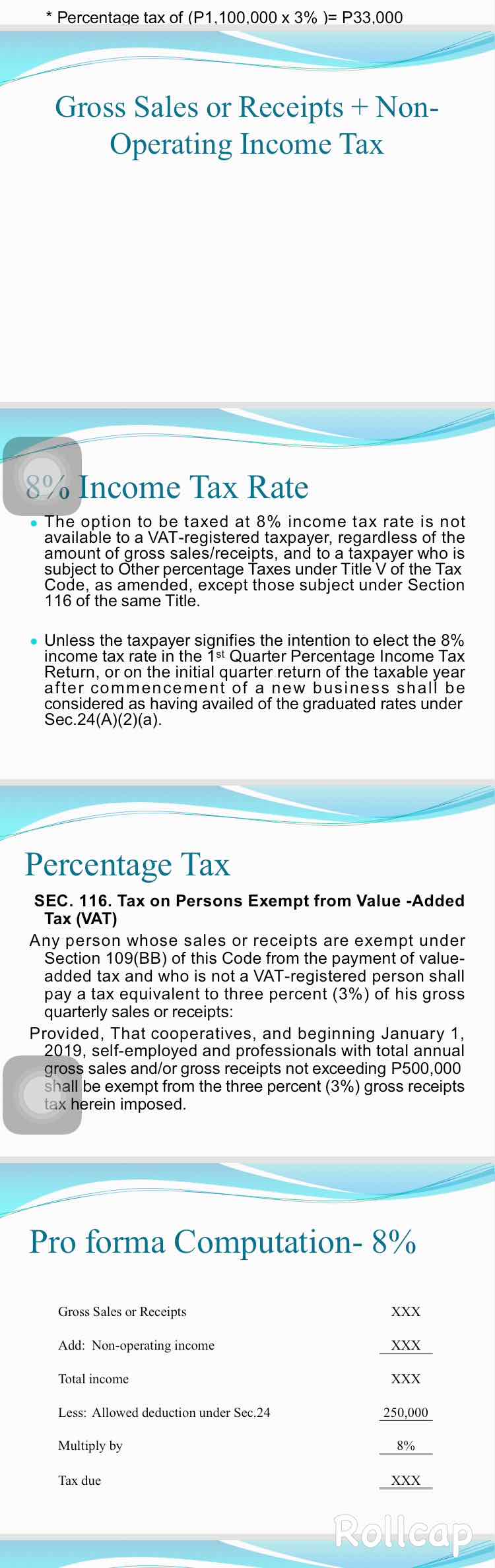

COMPUTE THE TAXABLE INCOME AND TAX DUE FOR THE BUSINESS USING 8% INCOME TAX RATE USE THE TAX TABLE OF 2018 PHILIPPINES Pro forma Computation-

COMPUTE THE TAXABLE INCOME AND TAX DUE FOR THE BUSINESS USING 8% INCOME TAX RATE

USE THE TAX TABLE OF 2018 PHILIPPINES

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial accounting

Authors: Walter T. Harrison, Charles T. Horngren, William Bill Thomas

8th Edition

9780135114933, 136108865, 978-0136108863