Answered step by step

Verified Expert Solution

Question

1 Approved Answer

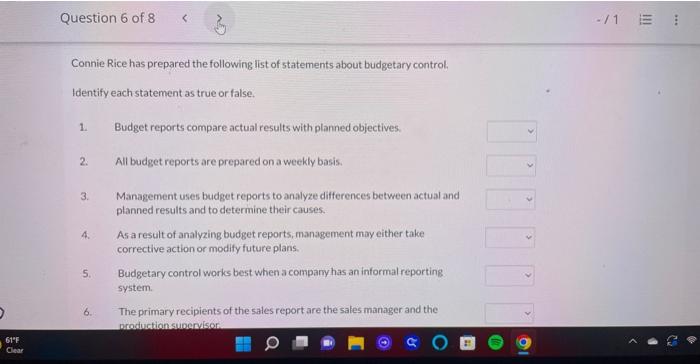

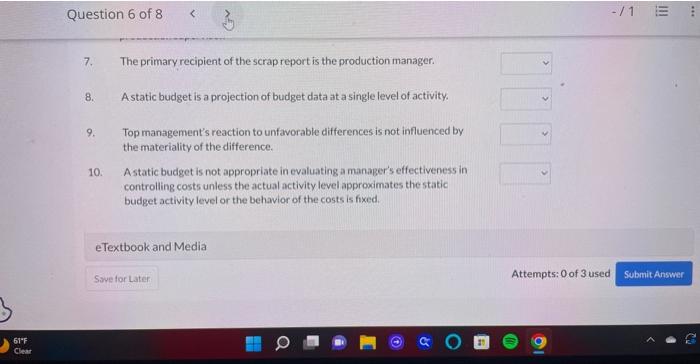

Connie Rice has prepared the following list of statements about budgetary control. Identify each statement as true or false. 1. Budget reports compare actual results

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cryptocurrency 101 The Millennials Guide To Understanding And Investing In Crypto

Authors: Candide Ahouandjinou, Jamal Modica

979-8387066771