Answered step by step

Verified Expert Solution

Question

1 Approved Answer

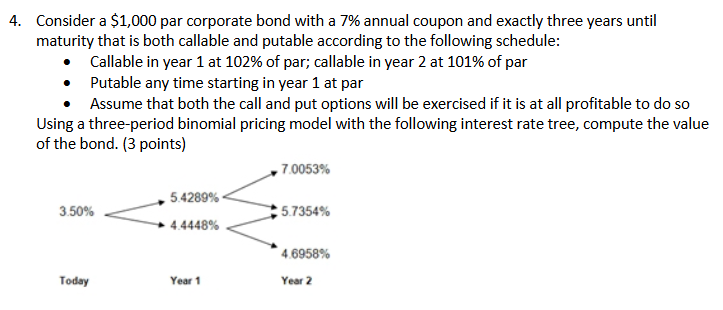

Consider a $ 1 , 0 0 0 par corporate bond with a 7 % annual coupon and exactly three years until maturity that is

Consider a $ par corporate bond with a annual coupon and exactly three years until

maturity that is both callable and putable according to the following schedule:

Callable in year at of par; callable in year at of par

Putable any time starting in year at par

Assume that both the call and put options will be exercised if it is at all profitable to do so

Using a threeperiod binomial pricing model with the following interest rate tree, compute the value

of the bond. pointsConsider a $ par corporate bond with a annual coupon and exactly three years until

maturity that is both callable and putable according to the following schedule:

Callable in year at of par; callable in year at of par

Putable any time starting in year at par

Assume that both the call and put options will be exercised if it is at all profitable to do so

Using a threeperiod binomial pricing model with the following interest rate tree, compute the value

of the bond. points

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Intelligence

Authors: Income Mastery

1st Edition

1647773210, 978-1647773212