Answered step by step

Verified Expert Solution

Question

1 Approved Answer

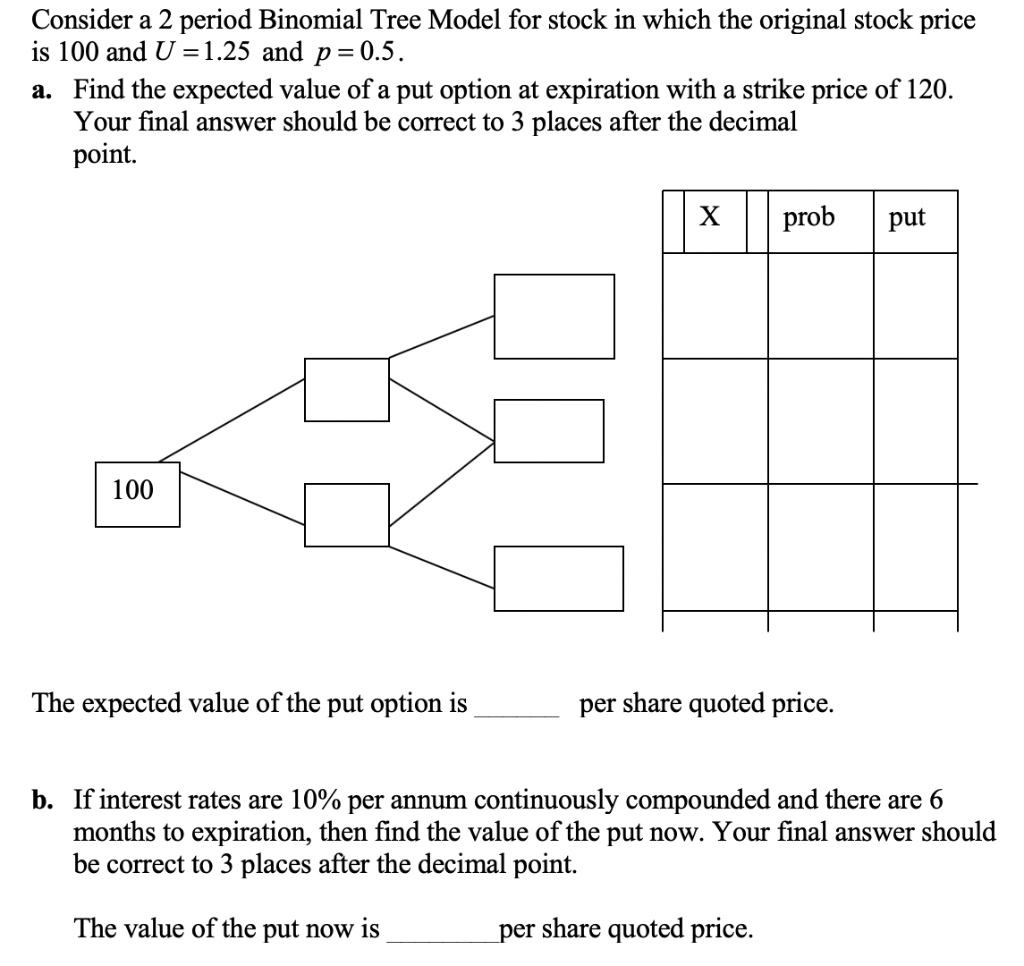

Consider a 2 period Binomial Tree Model for stock in which the original stock price is 100 and U =1.25 and p=0.5. a. Find the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Confessions Of A Scholarship Winner The Secrets That Helped Me Win $b 500000 In Free Money For College How You Can Too

Authors: Kristina Ellis

1st Edition

1617951579,1617951730