Question

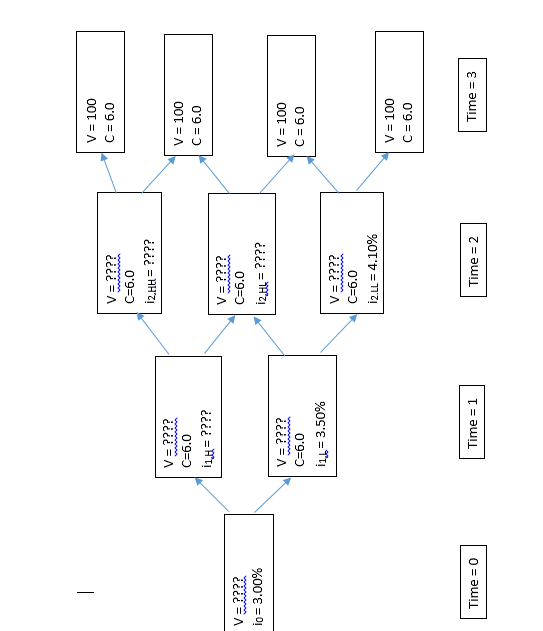

Consider a 3-year, 6.0% annual coupon bond represented by the binomial interest rate tree on the following page. The one-year implied forward rates are provided

Consider a 3-year, 6.0% annual coupon bond represented by the binomial interest rate tree on the following page. The one-year implied forward rates are provided for one node of each year of the bond. Assume that the interest rate volatility = 20%. Please complete the tree, filling in the other interest rates and the value of the bond at each node (wherever a ???? occurs, fill in an answer). Note that each node except the one at time=0 represents the payment of a 6.0% coupon, so be sure to include that in the valuation. Show your supporting work in the space below.

1 V = 100 C = 6.0 V = ???? C=6.0 12.HH = ???? V=???? C=6.0 114=???? V = 100 C = 6.0 VANNA V = ???? io = 3.00% V = ???? C=6.0 12.HL = ???? V = ???? C=6.0 11,6 = 3.50% V = 100 C = 6.0 V=???? C=6.0 12.LL = 4.10% V = 100 C = 6.0 Time = 0 Time = 1 Time = 2 Time = 3 1 V = 100 C = 6.0 V = ???? C=6.0 12.HH = ???? V=???? C=6.0 114=???? V = 100 C = 6.0 VANNA V = ???? io = 3.00% V = ???? C=6.0 12.HL = ???? V = ???? C=6.0 11,6 = 3.50% V = 100 C = 6.0 V=???? C=6.0 12.LL = 4.10% V = 100 C = 6.0 Time = 0 Time = 1 Time = 2 Time = 3Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Market Regulations And Finance

Authors: Ratan Khasnabis, Indrani Chakraborty

2014th Edition

8132217942, 978-8132217947