Question

Consider a 4-year leveraged inverse floating rate bond with the following coupon rate: c(t) = 24%-2.4*r(t-0.5). This coupon is paid semi-annually, in arrears. So, the

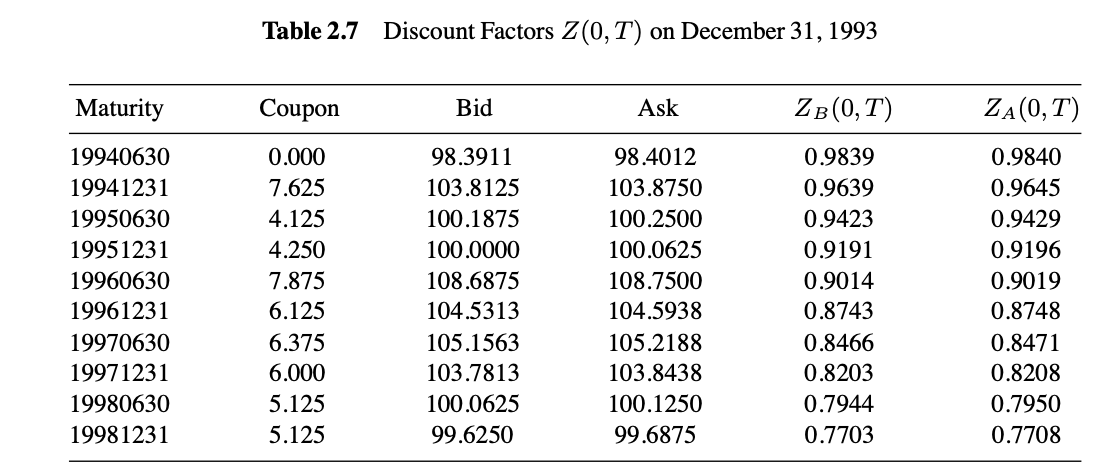

Consider a 4-year leveraged inverse floating rate bond with the following coupon rate: c(t) = 24%-2.4*r(t-0.5). This coupon is paid semi-annually, in arrears. So, the dollar coupon at each payment date is given by: $coupon = c(t) / 2 * 100. Assume it is Dec. 31, 1993 and use the average of the bid and ask discount factors given in the table below. What is the value of this inverse floater?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Trading The Future A Step By Step Guide To Futures Market Mastery

Authors: Axel Stevens

1st Edition

979-8857010327