Question

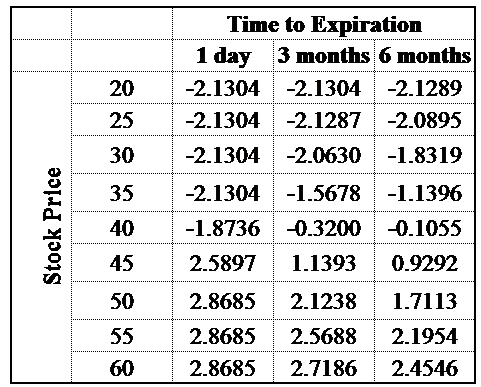

Consider a bull spread where you buy a 40-strike call and sell a 45-strike call. Suppose S=$40, =0.30, r =0.08, =0, and T =0.5.Drawagraphwithstock prices

"Consider a bull spread where you buy a 40-strike call and sell a 45-strike call. Suppose S=$40, =0.30, r =0.08, =0, and T =0.5.Drawagraphwithstock prices ranging from $20 to $60 depicting the prot on the bull spread after 1 day, 3 months, and 6 months " I know what are the answers (i attached the answer in a photo), but how do you get to that result? Using BS i get that the initial investment is 2.025, but then how do i get the spread?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding financial statements

Authors: Lyn M. Fraser, Aileen Ormiston

9th Edition

136086241, 978-0136086246