Answered step by step

Verified Expert Solution

Question

1 Approved Answer

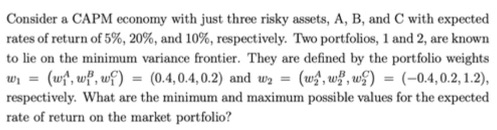

Consider a CAPM economy with just three risky assets, A , B , and C with expected rates of return of 5 % , 2

Consider a CAPM economy with just three risky assets, A B and C with expected

rates of return of and respectively. Two portfolios, and are known

to lie on the minimum variance frontier. They are defined by the portfolio weights

and

respectively. What are the minimum and maximum possible values for the expected

rate of return on the market portfolio?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Port Infrastructure Finance

Authors: Hilde Meersman, Eddy Van De Voorde, Thierry Vanelslander

1st Edition

0415720060, 978-0415720069