Question: Consider a classical multiple regression model given by: y = XB+u. (1) where y is n x 1 vector containing n realizations of the dependent

Consider a classical multiple regression model given by:

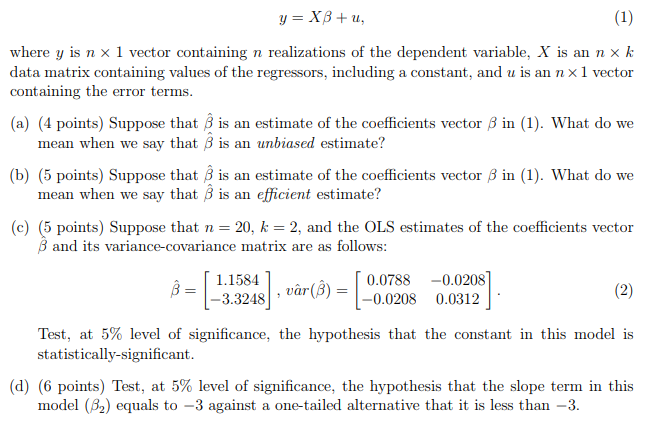

y = XB+u. (1) where y is n x 1 vector containing n realizations of the dependent variable, X is an n x k data matrix containing values of the regressors, including a constant, and u is an n x 1 vector containing the error terms. (a) (4 points) Suppose that 8 is an estimate of the coefficients vector B in (1). What do we mean when we say that S is an unbiased estimate? (b) (5 points) Suppose that 8 is an estimate of the coefficients vector B in (1). What do we mean when we say that S is an efficient estimate? (c) (5 points) Suppose that n = 20, k = 2, and the OLS estimates of the coefficients vector B and its variance-covariance matrix are as follows: 1.1584 -3.3248 , var(B) = 0.0788 -0.0208 -0.0208 0.0312 (2) Test, at 5% level of significance, the hypothesis that the constant in this model is statistically-significant. (d) (6 points) Test, at 5% level of significance, the hypothesis that the slope term in this model (82) equals to -3 against a one-tailed alternative that it is less than -3

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts