Answered step by step

Verified Expert Solution

Question

1 Approved Answer

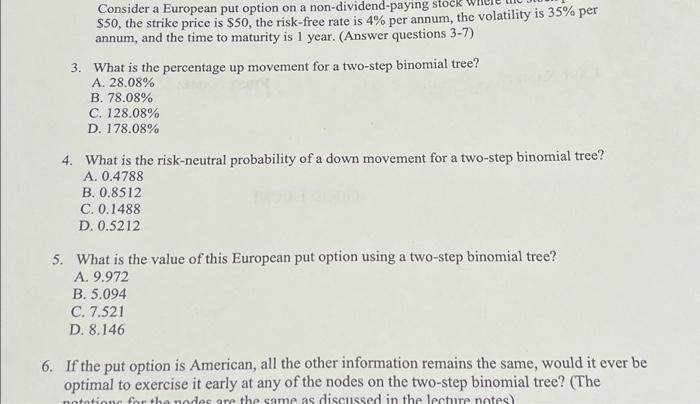

Consider a European put option on a non-dividend-paying stock $50, the strike price is $50, the risk-free rate is 4% per annum, the volatility is

Consider a European put option on a non-dividend-paying stock $50, the strike price is $50, the risk-free rate is 4% per annum, the volatility is 35% per annum, and the time to maturity is 1 year. (Answer questions 3-7) 3. What is the percentage up movement for a two-step binomial tree? A. 28.08% B. 78.08% C. 128.08% D. 178.08% 4. What is the risk-neutral probability of a down movement for a two-step binomial tree? A. 0.4788 B. 0.8512 C. 0.1488 D. 0.5212 5. What is the value of this European put option using a two-step binomial tree? A. 9.972 B. 5.094 C. 7.521 D. 8.146 6. If the put option is American, all the other information remains the same, would it ever be optimal to exercise it early at any of the nodes on the two-step binomial tree? (The notations for the nodes are the same as discussed in the lecture notes)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Gold And Debt An American Hand Book Of Finance With Over Eighty Tables And Diagrams Illustrative Of The Following Subjects The Dollar And Other Units Paper Money In The United States And Europe Gold And Silver In The United States And Europe

Authors: Fawcett William Lyman

1st Edition

1313124508, 9781313124508