Answered step by step

Verified Expert Solution

Question

1 Approved Answer

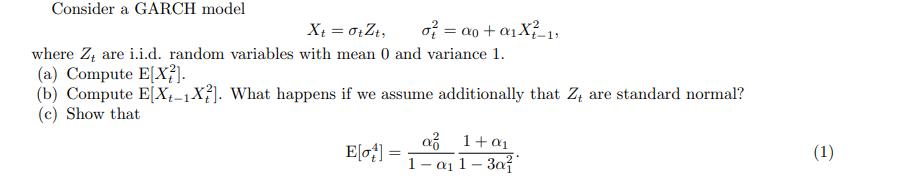

Consider a GARCH model Xt = 0tZt; where Z are i.i.d. random variables with mean 0 and variance 1. (a) Compute E[X]. (b) Compute

Consider a GARCH model Xt = 0tZt; where Z are i.i.d. random variables with mean 0 and variance 1. (a) Compute E[X]. (b) Compute E[X-1X2]. What happens if we assume additionally that Z, are standard normal? (c) Show that o = a0 + X-12 E[ot] = a 1+0 1- 01-30 (1)

Step by Step Solution

★★★★★

3.45 Rating (161 Votes )

There are 3 Steps involved in it

Step: 1

The detailed ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

An Introduction to the Mathematics of Financial Derivatives

Authors: Ali Hirsa, Salih N. Neftci

3rd edition

012384682X, 978-0123846822