Question

Consider a guaranteed annuity contract issued by a life insurance company with a rate of 3.08% and a term of 20 years. For a $100,000

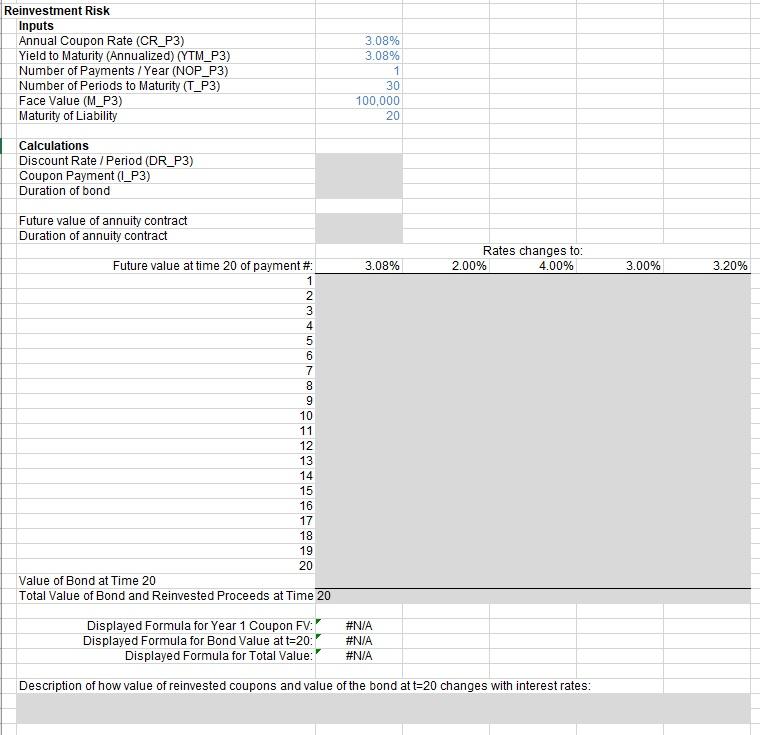

Consider a guaranteed annuity contract issued by a life insurance company with a rate of 3.08% and a term of 20 years. For a $100,000 nominal amount, the insurance company is promising to pay $183,437.53 (=100,000*(1.0308)^20) to the holder of the guaranteed annuity contract in 20 years. (In practice, this lump sum would be spread out over a subsequent period as an annuity; for simplicity, we will assume a lump sum payment.) We want to know the interest rate risk exposure to the company if it funds this liability using a 30-year bond with a coupon rate of 3.08% issued at par. To do so, assume that in the first year, rates change to one of the five possible values in row 18 and then stay constant for the next 20 years. For each rate change, calculate two things: (1) the future value (as of 20 years down the road) of each coupon payment made by the 30-year bond for the next 20 years, and (2) the value at year 20 of the bond used to fund the obligation. For (1), assume the coupons are reinvested at the new prevailing interest rate. The sum of the reinvested coupons and the value of the bond are the total future value of the assets used to finance the annuity contract.

What is the duration of the 30-year bond as of today? What is the duration of the guaranteed annuity contract? Briefly describe how the value of the reinvested coupons and the value of the bond change as a function of interest rate changes. Will the insurance company be able to meet its obligation to the purchaser of the guaranteed annuity contract?

Reinvestment Risk Inputs Annual Coupon Rate (CR_P3) Yield to Maturity (Annualized) (YTM_P3) Number of Payments / Year (NOP_P3) Number of Periods to Maturity (T_P3) Face Value (M_P3) Maturity of Liability Calculations Discount Rate / Period (DR_P3) Coupon Payment (l_P3) Duration of bond Future value of annuity contract Duration of annuity contract Rates changes to: 4.00% Value of Bond at Time 20 Total Value of Bond and Reinvested Proceeds at Time 20 #N/A Displayed Formula for Year 1 Coupon FV: Displayed Formula for Bond Value at t=20: #N/A Displayed Formula for Total Value: #N/A Description of how value of reinvested coupons and value of the bond at t=20 changes with interest rates: Future value at time 20 of payment #: 1 2 3 4 5 6 3.08% 3.08% 1 30 100,000 20 3.08% u789 10 1112 131415 16 17 18 19 20 2.00% 3.00% 3.20% Reinvestment Risk Inputs Annual Coupon Rate (CR_P3) Yield to Maturity (Annualized) (YTM_P3) Number of Payments / Year (NOP_P3) Number of Periods to Maturity (T_P3) Face Value (M_P3) Maturity of Liability Calculations Discount Rate / Period (DR_P3) Coupon Payment (l_P3) Duration of bond Future value of annuity contract Duration of annuity contract Rates changes to: 4.00% Value of Bond at Time 20 Total Value of Bond and Reinvested Proceeds at Time 20 #N/A Displayed Formula for Year 1 Coupon FV: Displayed Formula for Bond Value at t=20: #N/A Displayed Formula for Total Value: #N/A Description of how value of reinvested coupons and value of the bond at t=20 changes with interest rates: Future value at time 20 of payment #: 1 2 3 4 5 6 3.08% 3.08% 1 30 100,000 20 3.08% u789 10 1112 131415 16 17 18 19 20 2.00% 3.00% 3.20%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Repo Handbook

Authors: Moorad Choudhry

1st Edition

0750651628, 978-0750651622