Answered step by step

Verified Expert Solution

Question

1 Approved Answer

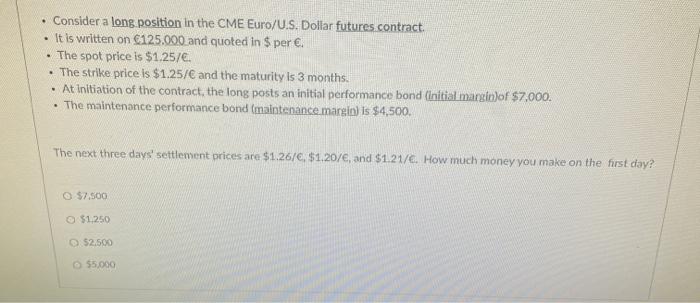

. Consider a long position in the CME Euro/U.S. Dollar futures contract. It is written on 125.000 and quoted in $ per . The spot

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bond Markets Analysis and Strategies

Authors: Frank J.Fabozzi

9th edition

133796779, 978-0133796773