Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Consider a market model with four scenarios and two risky assets with rates of return Ri and R2, respectively. Let the distribution of the

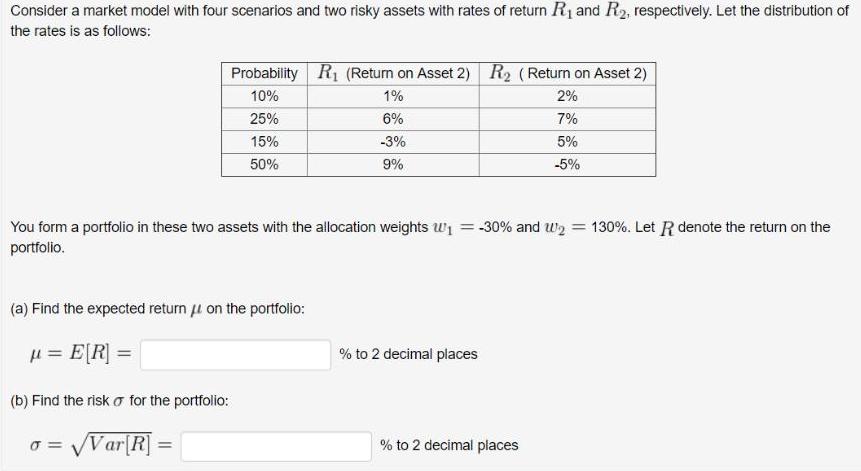

Consider a market model with four scenarios and two risky assets with rates of return Ri and R2, respectively. Let the distribution of the rates is as follows: Probability R1 (Retum on Asset 2) R2 (Return on Asset 2) 10% 1% 2% 25% 6% 7% 15% -3% 5% 50% 9% -5% You form a portfolio in these two assets with the allocation weights wi = -30% and wz = 130%. Let R denote the return on the portfolio. (a) Find the expected return i on the portfolio: u = E[R] = % to 2 decimal places (b) Find the risk o for the portfolio: o = VVar[R] % to 2 decimal places %3D

Step by Step Solution

★★★★★

3.39 Rating (149 Votes )

There are 3 Steps involved in it

Step: 1

Solution Consider the Scenazios ond Rekuens R4 fr ass...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Theory and Corporate Policy

Authors: Thomas E. Copeland, J. Fred Weston, Kuldeep Shastri

4th edition

321127218, 978-0321179548, 321179544, 978-0321127211