Answered step by step

Verified Expert Solution

Question

1 Approved Answer

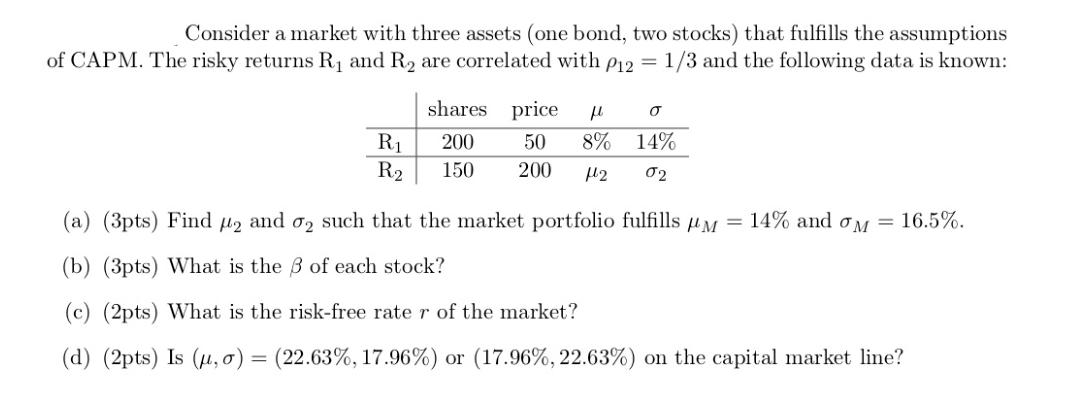

Consider a market with three assets (one bond, two stocks) that fulfills the assumptions of CAPM. The risky returns R and R2 are correlated

Consider a market with three assets (one bond, two stocks) that fulfills the assumptions of CAPM. The risky returns R and R2 are correlated with P12 1/3 and the following data is known: = R 200 R2 150 shares price 50 8% 14% 200 12 02 (a) (3pts) Find 2 and such that the market portfolio fulfills M = 14% and M = 16.5%. (b) (3pts) What is the of each stock? (c) (2pts) What is the risk-free rate r of the market? (d) (2pts) Is (u, 0) = (22.63%, 17.96%) or (17.96%, 22.63%) on the capital market line?

Step by Step Solution

★★★★★

3.45 Rating (168 Votes )

There are 3 Steps involved in it

Step: 1

a To find the weights w1 and w2 such that the market portfolio fulfills muM 14 and sigmaM 165 we can use the formula for the expected return and standard deviation of a twoasset portfolio muM w1 mu1 w...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Microeconomics

Authors: Hal R. Varian

9th edition

978-0393123975, 393123979, 393123960, 978-0393919677, 393919676, 978-0393123968