Answered step by step

Verified Expert Solution

Question

1 Approved Answer

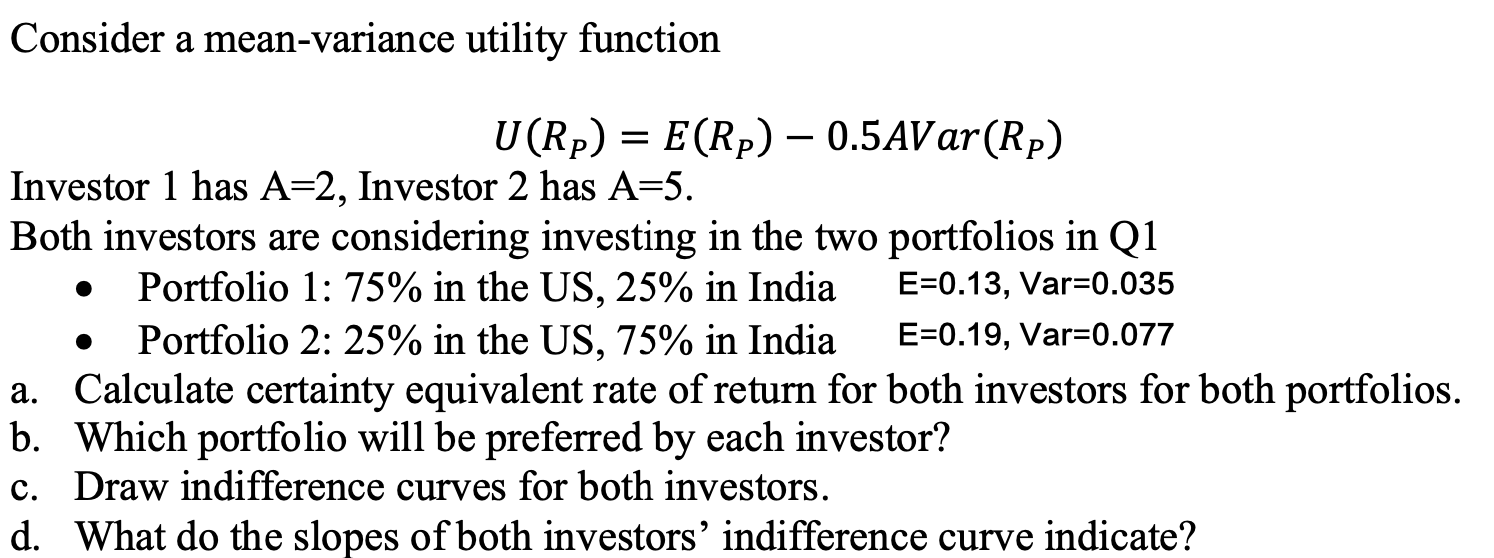

Consider a mean-variance utility function U(RP)=E(RP)0.5AVar(RP) Investor 1 has A=2, Investor 2 has A=5. Both investors are considering investing in the two portfolios in Q1

Consider a mean-variance utility function U(RP)=E(RP)0.5AVar(RP) Investor 1 has A=2, Investor 2 has A=5. Both investors are considering investing in the two portfolios in Q1 - Portfolio 1: 75% in the US, 25% in India E=0.13, Var =0.035 - Portfolio 2: 25% in the US, 75% in India E=0.19, Var =0.077 a. Calculate certainty equivalent rate of return for both investors for both portfolios. b. Which portfolio will be preferred by each investor? c. Draw indifference curves for both investors. d. What do the slopes of both investors' indifference curve indicate

Consider a mean-variance utility function U(RP)=E(RP)0.5AVar(RP) Investor 1 has A=2, Investor 2 has A=5. Both investors are considering investing in the two portfolios in Q1 - Portfolio 1: 75% in the US, 25% in India E=0.13, Var =0.035 - Portfolio 2: 25% in the US, 75% in India E=0.19, Var =0.077 a. Calculate certainty equivalent rate of return for both investors for both portfolios. b. Which portfolio will be preferred by each investor? c. Draw indifference curves for both investors. d. What do the slopes of both investors' indifference curve indicate Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Trade Finance

Authors: Indian Institute Of Banking & Finance

1st Edition

9386394723, 978-9386394729