Answered step by step

Verified Expert Solution

Question

1 Approved Answer

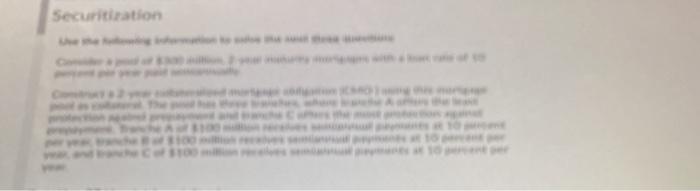

Consider a pool of $300 million, 2-year maturity percent per year paid semiannually. Construct a 2-year collateralized mortgage obligation mortgage pool as collateral. The pool

Consider a pool of $300 million, 2-year maturity percent per year paid semiannually. Construct a 2-year collateralized mortgage obligation mortgage pool as collateral. The pool has three tranches, where tranche A offers the least protection against prepayment and tranche C offers the most protection against prepayment. $100 million receives semiannual payments at 10 percent per year, tranche B of $100 million receives semiannual payments at 10 percent per year, and tranche C of $100 million receives semiannual payments at 10 percent per year.

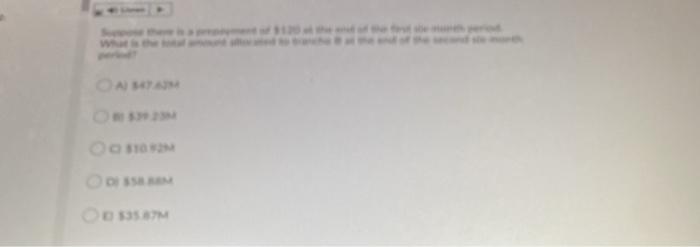

A Securitiration A Securitiration Q: Suppose there is a prepayment of $120 at the end of the first six-month period. What is the total amount allocated to tranche B at the end of the second six-month period? A) $35.87M B) $39.23M C) $10.92M D) $58.88M E) $47.62M

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Sterling Bonds And Fixed Income Handbook

Authors: Mark Glowrey

1st Edition

0857190423, 978-0857190420