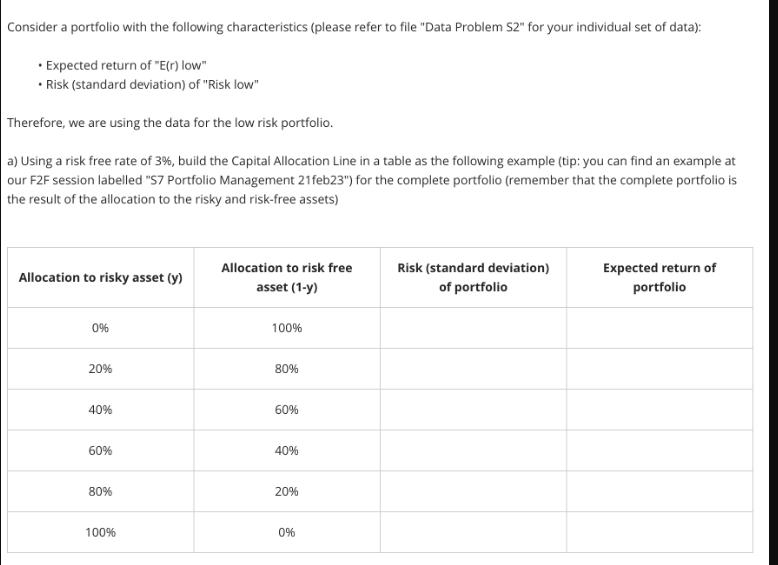

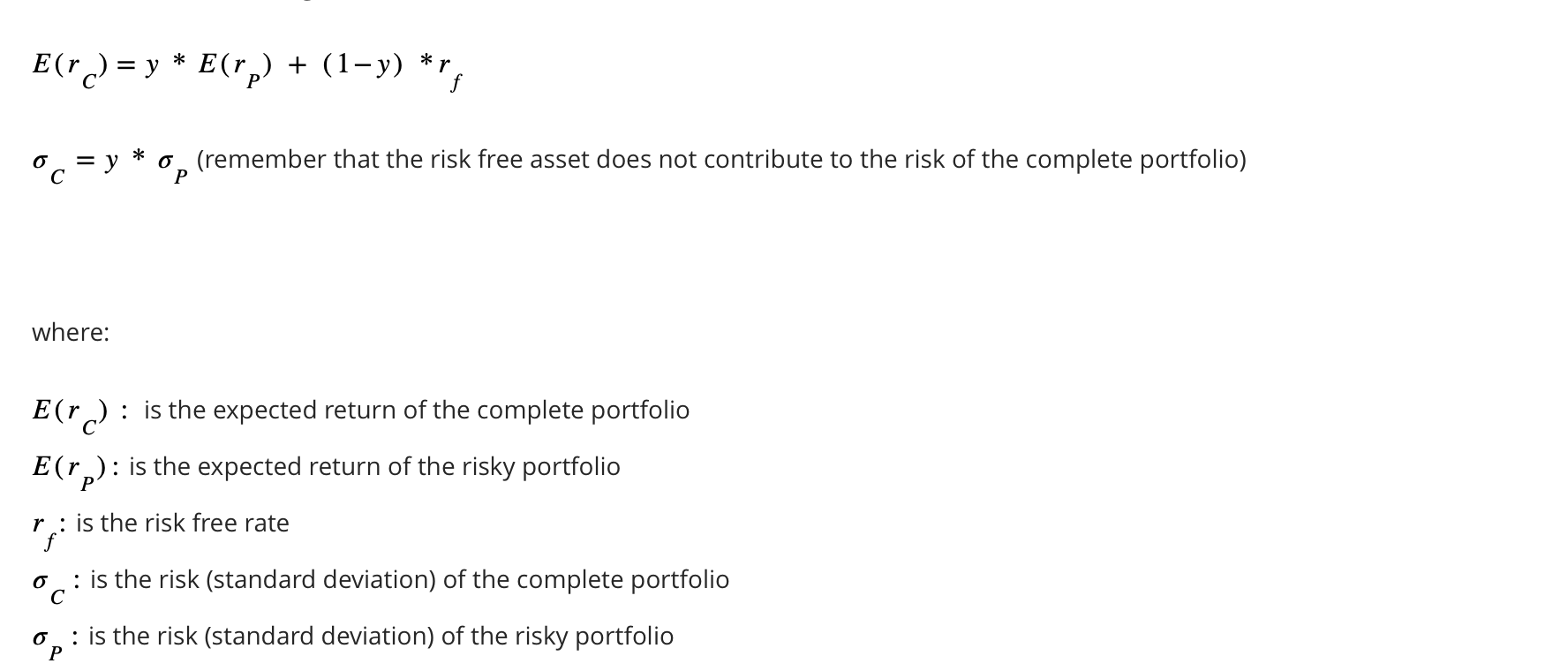

Consider a portfolio with the following characteristics (please refer to file Data Problem S2 for your...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Posted Date: