Answered step by step

Verified Expert Solution

Question

1 Approved Answer

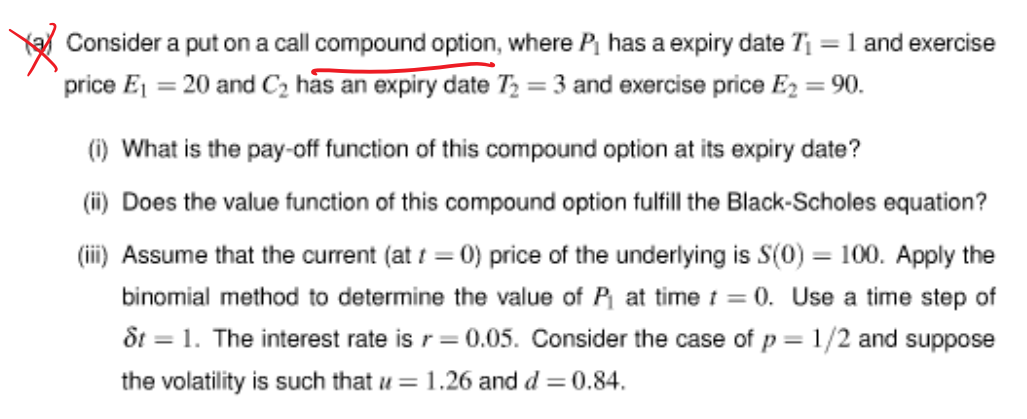

Consider a put on a call compound option, where P, has a expiry date Ti = 1 and exercise price E1 = 20 and C

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

An Environmental Audit Primer Student Guide

Authors: Velsoft Training Materials, Inc.

1st Edition

1774550393, 978-1774550397