Answered step by step

Verified Expert Solution

Question

1 Approved Answer

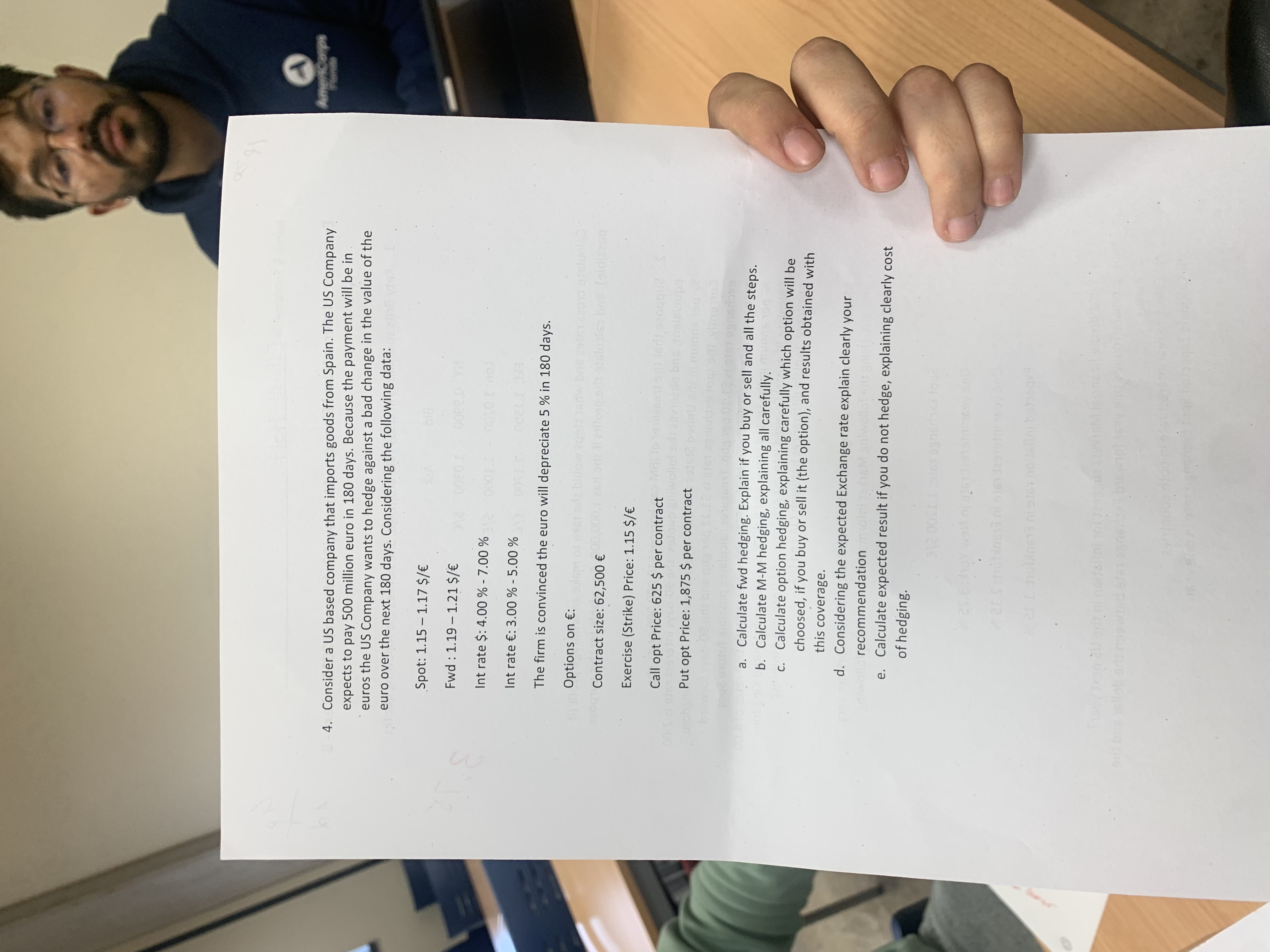

Consider a US based company that imports goods from Spain. The US Company expects to pay 500 million euro in 180 days. Because the payment

Consider a US based company that imports goods from Spain. The US Company expects to pay 500 million euro in 180 days. Because the payment will be in euros the US Company wants to hedge against a bad change in the value of the euro over the next 180 days. Considering the following data: Spot: 1.151.17$/ Fwd : 1.191.21$/ Int rate $:4.00%7.00% Int rate :3.00%5.00% The firm is convinced the euro will depreciate 5% in 180 days. Options on : Contract size: 62,500 Exercise (Strike) Price: 1.15$/ Call opt Price: 625 \$ per contract Put opt Price: 1,875$ per contract a. Calculate fwd hedging. Explain if you buy or sell and all the steps. b. Calculate M-M hedging, explaining all carefully. c. Calculate option hedging, explaining carefully which option will be choosed, if you buy or sell it (the option), and results obtained with this coverage. d. Considering the expected Exchange rate explain clearly your recommendation e. Calculate expected result if you do not hedge, explaining clearly cost of hedging

Consider a US based company that imports goods from Spain. The US Company expects to pay 500 million euro in 180 days. Because the payment will be in euros the US Company wants to hedge against a bad change in the value of the euro over the next 180 days. Considering the following data: Spot: 1.151.17$/ Fwd : 1.191.21$/ Int rate $:4.00%7.00% Int rate :3.00%5.00% The firm is convinced the euro will depreciate 5% in 180 days. Options on : Contract size: 62,500 Exercise (Strike) Price: 1.15$/ Call opt Price: 625 \$ per contract Put opt Price: 1,875$ per contract a. Calculate fwd hedging. Explain if you buy or sell and all the steps. b. Calculate M-M hedging, explaining all carefully. c. Calculate option hedging, explaining carefully which option will be choosed, if you buy or sell it (the option), and results obtained with this coverage. d. Considering the expected Exchange rate explain clearly your recommendation e. Calculate expected result if you do not hedge, explaining clearly cost of hedging Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started