Answered step by step

Verified Expert Solution

Question

1 Approved Answer

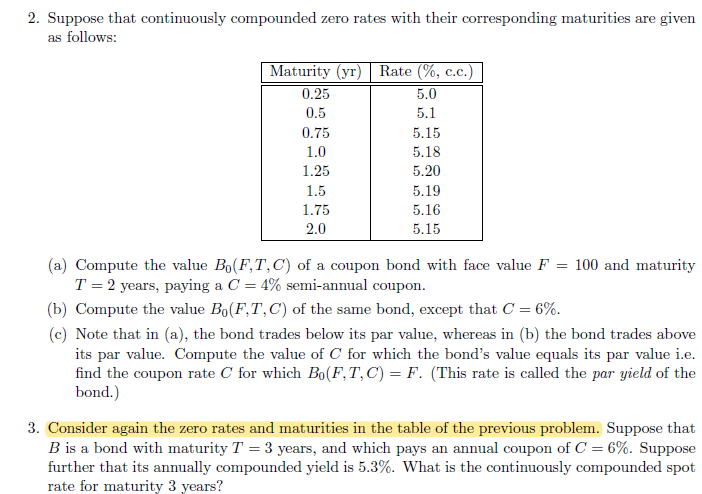

Consider again the zero rates and maturities in the table of the previous problem. Suppose that B is a bond with maturity T = 3

Consider again the zero rates and maturities in the table of the previous problem. Suppose that

is a bond with maturity years, and which pays an annual coupon of Suppose

further that its annually compounded yield is What is the continuously compounded spot

rate for maturity years?

Please do Question

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Course In Derivative Securities

Authors: Kerry Back

2005th Edition

3540253734, 978-3540253730