Answered step by step

Verified Expert Solution

Question

1 Approved Answer

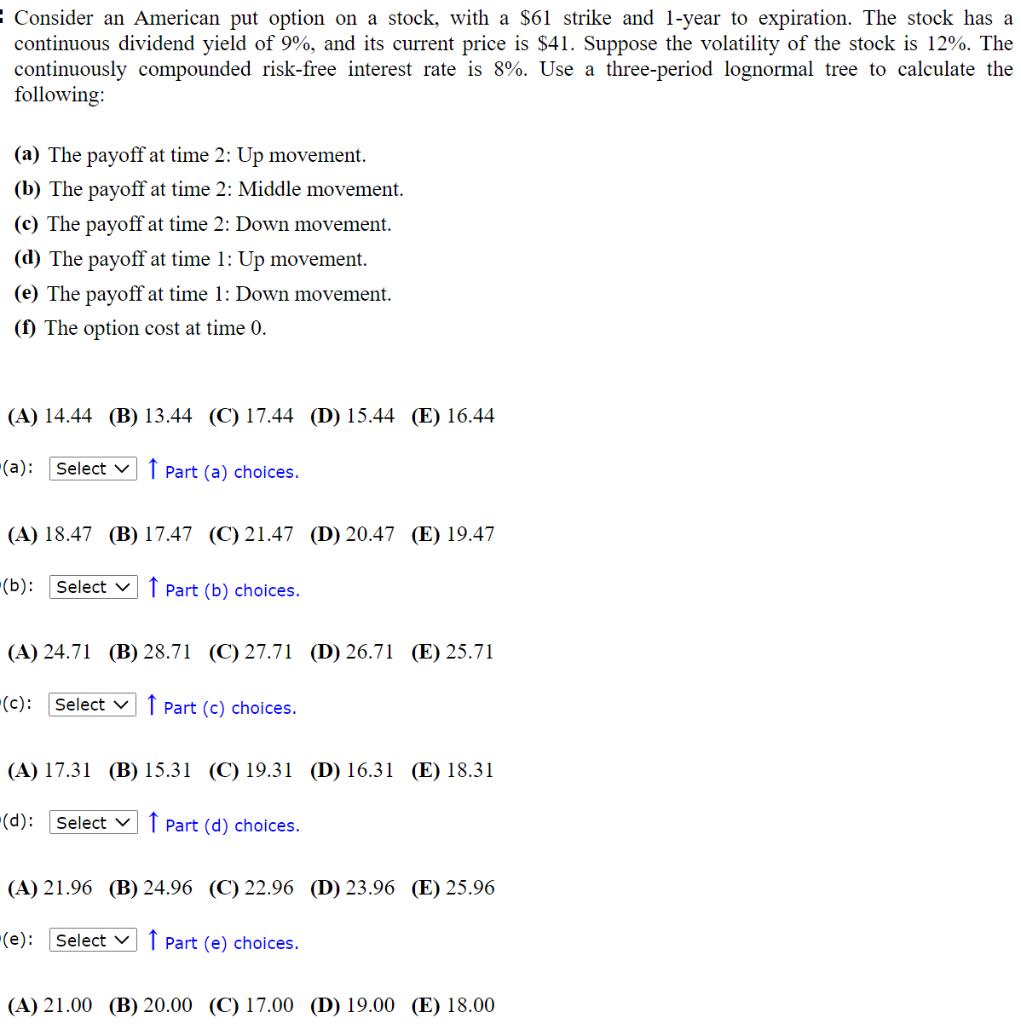

Consider an American put option on a stock, with a $61 strike and 1-year to expiration. The stock has a continuous dividend yield of

Consider an American put option on a stock, with a $61 strike and 1-year to expiration. The stock has a continuous dividend yield of 9%, and its current price is $41. Suppose the volatility of the stock is 12%. The continuously compounded risk-free interest rate is 8%. Use a three-period lognormal tree to calculate the following: (a) The payoff at time 2: Up movement. (b) The payoff at time 2: Middle movement. (c) The payoff at time 2: Down movement. (d) The payoff at time 1: Up movement. (e) The payoff at time 1: Down movement. (f) The option cost at time 0. (A) 14.44 (B) 13.44 (C) 17.44 (D) 15.44 (E) 16.44 (a): Select Part (a) choices. (A) 18.47 (B) 17.47 (C) 21.47 (D) 20.47 (E) 19.47 (b): Select v Part (b) choices. (A) 24.71 (B) 28.71 (C) 27.71 (D) 26.71 (E) 25.71 (c): Select Part (c) choices. (A) 17.31 (B) 15.31 (C) 19.31 (D) 16.31 (E) 18.31 (d): Select Part (d) choices. (A) 21.96 (B) 24.96 (C) 22.96 (D) 23.96 (E) 25.96 -(e): Select 1 Part (e) choices. (A) 21.00 (B) 20.00 (C) 17.00 (D) 19.00 (E) 18.00

Step by Step Solution

★★★★★

3.56 Rating (156 Votes )

There are 3 Steps involved in it

Step: 1

a The payoff at time 2 Up movement The payoff at time 2 for an up movement is calculated using a threeperiod lognormal tree First we need to calculate the upmovement probability which is calculated by ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance

Authors: Jonathan Berk, Peter DeMarzo

4th edition

013408327X, 978-0134083278