Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Consider an arbitrary random variable X and let Y = aX + b for constants a > 0 and b R . Show that VaR

Consider an arbitrary random variable X and let Y aX b for constants a and b R Show that VaRX Y VaRX VaRY for Exercise VaR and ES for a discrete distribution

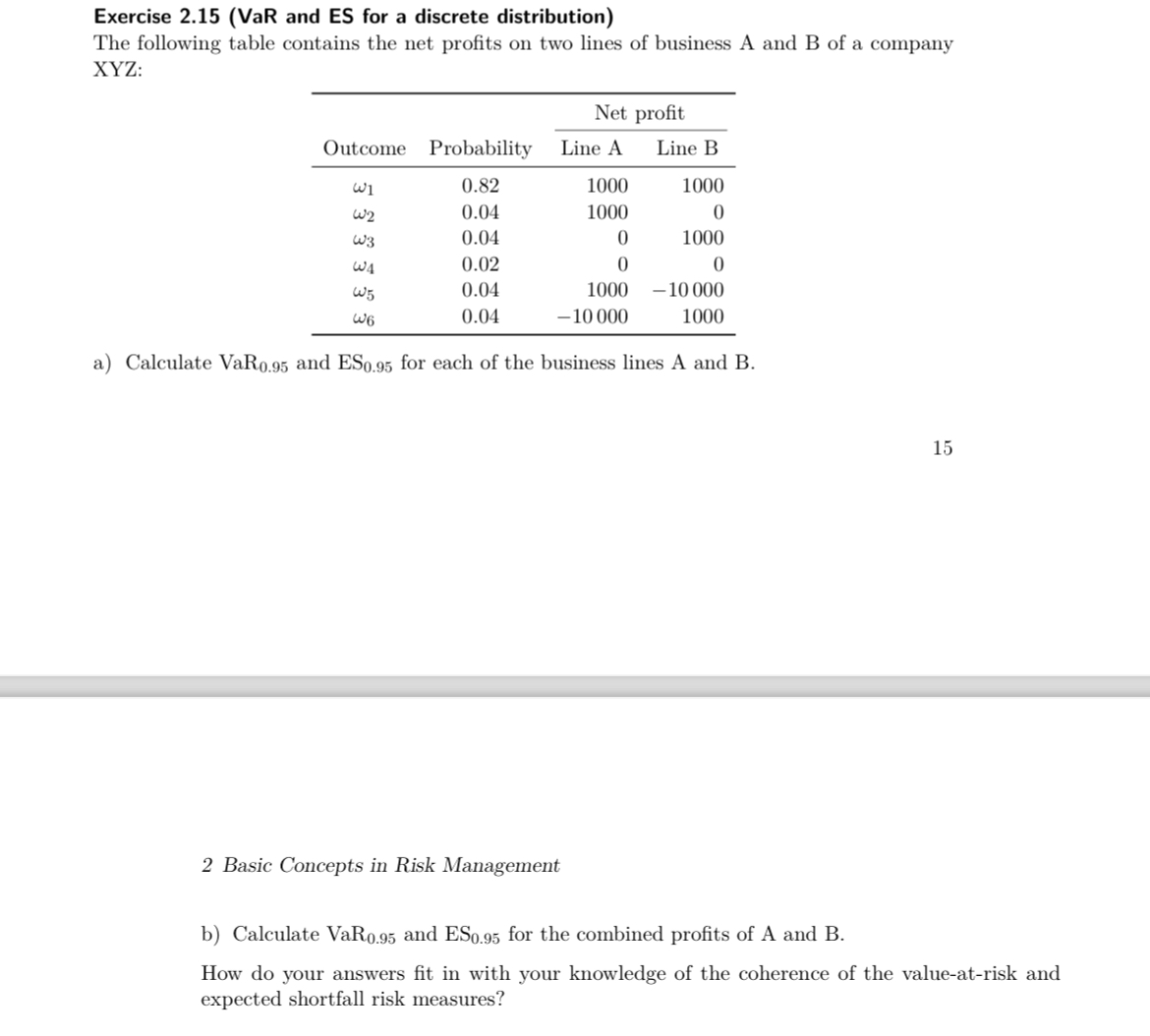

The following table contains the net profits on two lines of business A and B of a company

:

a Calculate and for each of the business lines A and

Basic Concepts in Risk Management

b Calculate and for the combined profits of A and

How do your answers fit in with your knowledge of the coherence of the valueatrisk and

expected shortfall risk measures?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance For Dummies

Authors: Michael Taillard

2nd Edition

1119850312, 978-1119850311