Answered step by step

Verified Expert Solution

Question

1 Approved Answer

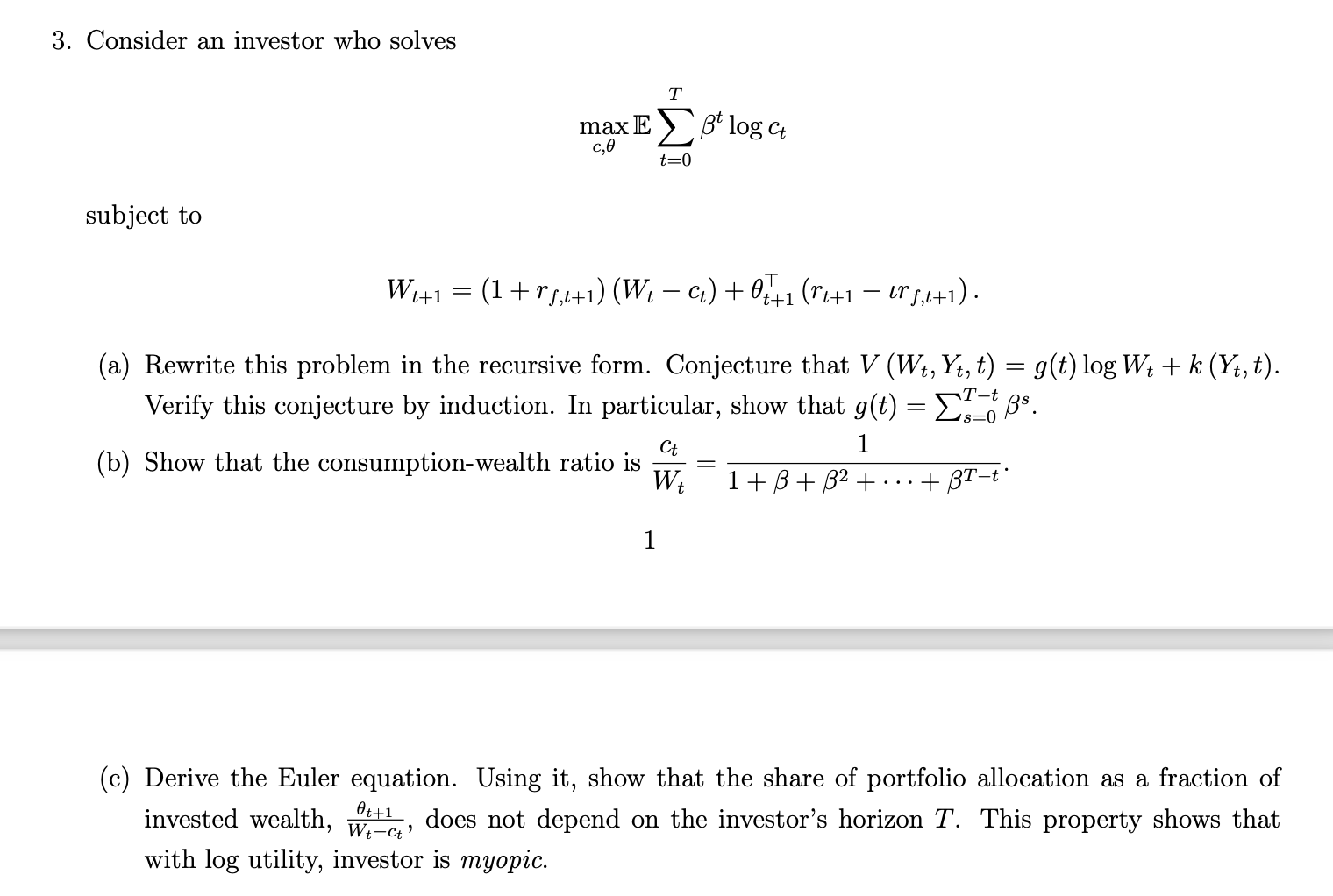

Consider an investor who solves m a x c , E t = 0 T t l o g c t subject to W t

Consider an investor who solves

subject to

a Rewrite this problem in the recursive form. Conjecture that

Verify this conjecture by induction. In particular, show that

b Show that the consumptionwealth ratio is

c Derive the Euler equation. Using it show that the share of portfolio allocation as a fraction of

invested wealth, does not depend on the investor's horizon This property shows that

with utility, investor is myopic.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Renewable Energy Finance Funding The Future Of Energy

Authors: Charles W Donovan

2nd Edition

1786348594, 9781786348593