Answered step by step

Verified Expert Solution

Question

1 Approved Answer

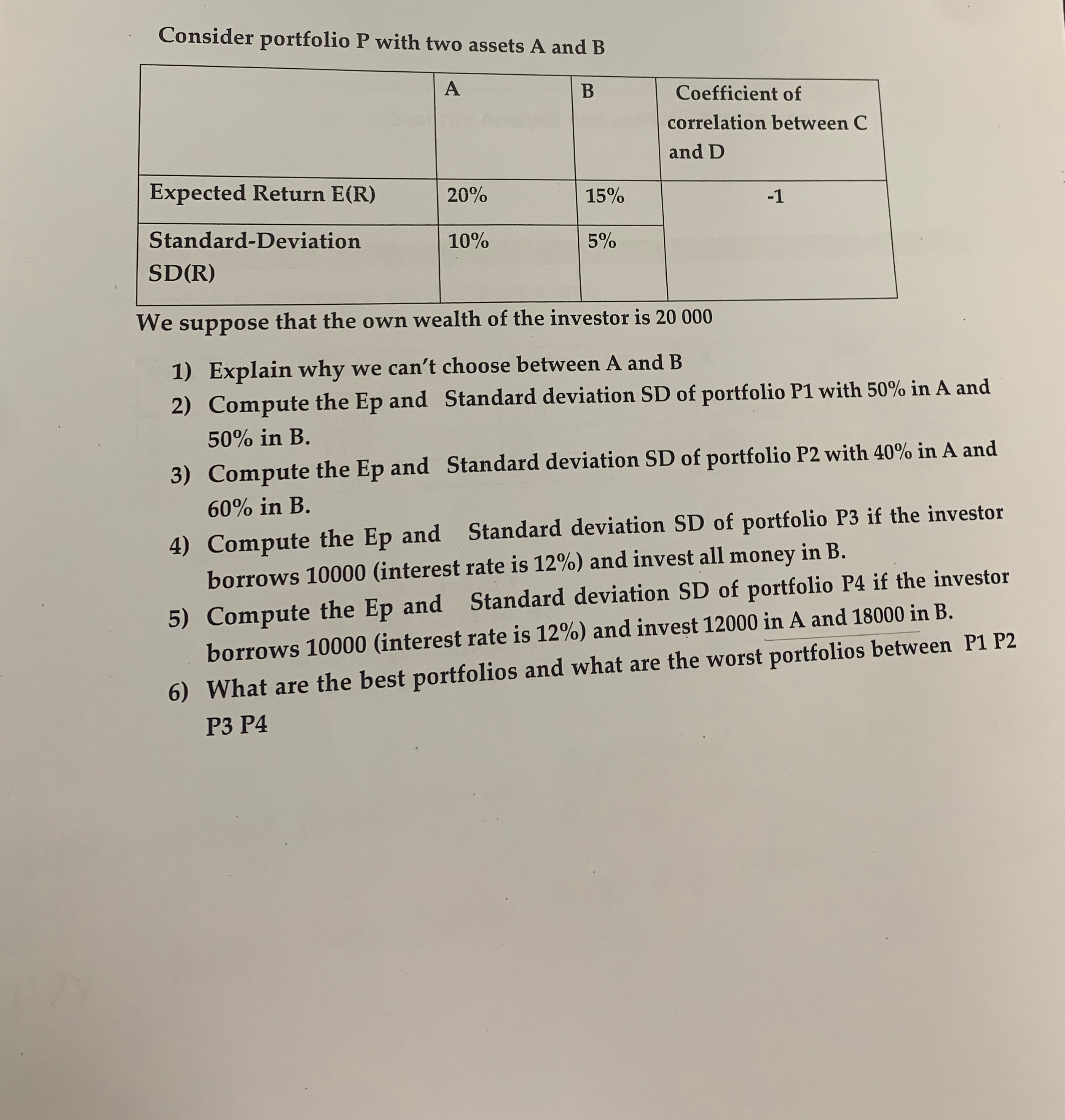

Consider portfolio P with two assets A and B table [ [ , A , B , table [ [ Coefficient of ]

Consider portfolio with two assets A and B

tableABtableCoefficient ofcorrelation between Cand DExpected Return ERtableStandardDeviationSDR

We suppose that the own wealth of the investor is

Explain why we can't choose between A and

Compute the Ep and Standard deviation SD of portfolio with in A and in

Compute the Ep and Standard deviation SD of portfolio with in A and in

Compute the Ep and Standard deviation SD of portfolio P if the investor borrows interest rate is and invest all money in B

Compute the Ep and Standard deviation SD of portfolio if the investor borrows interest rate is and invest in A and in B

What are the best portfolios and what are the worst portfolios between P P P P

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Economics And Personal Finance

Authors: Irvin Tucker, Joan Ryan

1st Edition

1133562108, 978-1133562108