Answered step by step

Verified Expert Solution

Question

1 Approved Answer

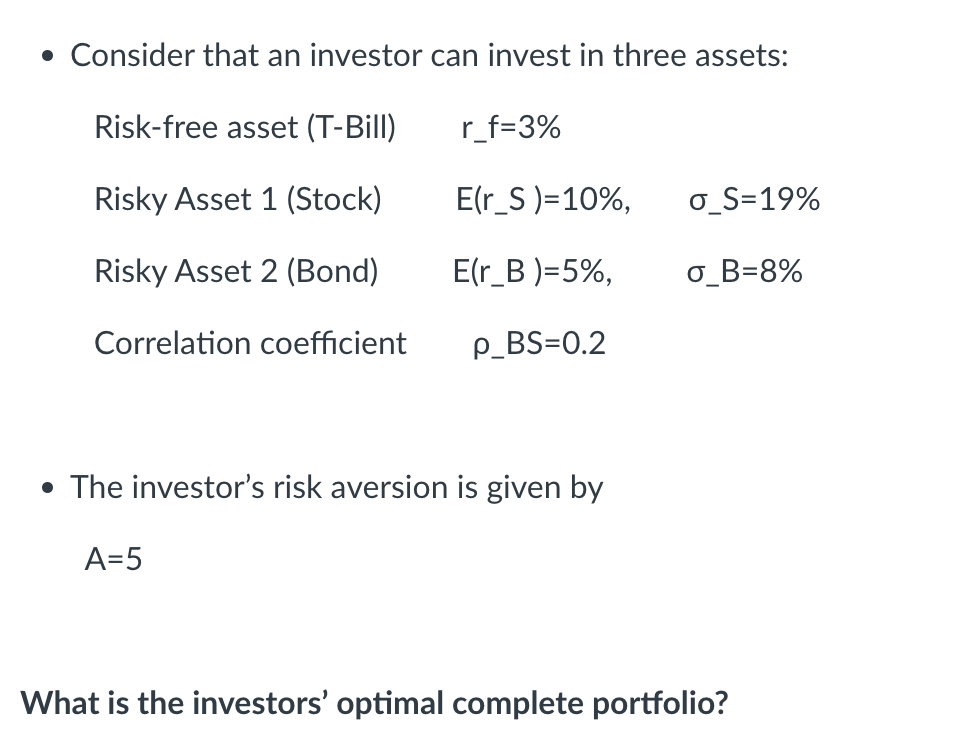

- Consider that an investor can invest in three assets: Risk-free asset (T-Bill) rf=3% Risky Asset 1 (Stock) E(rS)=10%,S=19% Risky Asset 2 (Bond) E(rB)=5%,B=8% Correlation

- Consider that an investor can invest in three assets: Risk-free asset (T-Bill) rf=3% Risky Asset 1 (Stock) E(rS)=10%,S=19% Risky Asset 2 (Bond) E(rB)=5%,B=8% Correlation coefficient _BS=0.2 - The investor's risk aversion is given by A=5 What is the investors' optimal complete portfolio

- Consider that an investor can invest in three assets: Risk-free asset (T-Bill) rf=3% Risky Asset 1 (Stock) E(rS)=10%,S=19% Risky Asset 2 (Bond) E(rB)=5%,B=8% Correlation coefficient _BS=0.2 - The investor's risk aversion is given by A=5 What is the investors' optimal complete portfolio Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance Principles And Practice

Authors: Denzil Watson, Tony Head

1st Edition

0273630083, 978-0273630081