Answered step by step

Verified Expert Solution

Question

1 Approved Answer

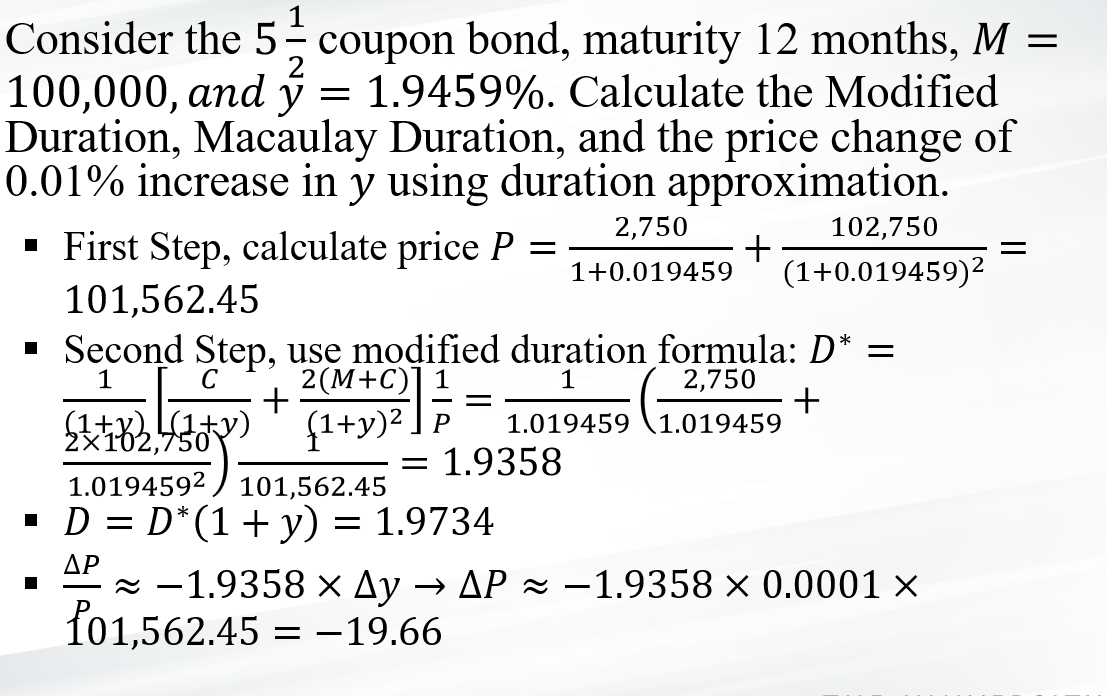

Consider the 521 coupon bond, maturity 12 months, M= 100,000 , and 2=1.9459%. Calculate the Modified Duration, Macaulay Duration, and the price change of 0.01%

Consider the 521 coupon bond, maturity 12 months, M= 100,000 , and 2=1.9459%. Calculate the Modified Duration, Macaulay Duration, and the price change of 0.01% increase in y using duration approximation. - First Step, calculate price P=1+0.0194592,750+(1+0.019459)2102,750= 101,562.45 - Second Step, use modified duration formula: D= (1+y)1[(1+y)C+(1+y)22(M+C)]P1=1.0194591(1.0194592,750+ - D=D(1+y)=1.9734 - PP1.9358yP1.93580.0001

Consider the 521 coupon bond, maturity 12 months, M= 100,000 , and 2=1.9459%. Calculate the Modified Duration, Macaulay Duration, and the price change of 0.01% increase in y using duration approximation. - First Step, calculate price P=1+0.0194592,750+(1+0.019459)2102,750= 101,562.45 - Second Step, use modified duration formula: D= (1+y)1[(1+y)C+(1+y)22(M+C)]P1=1.0194591(1.0194592,750+ - D=D(1+y)=1.9734 - PP1.9358yP1.93580.0001 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance With Monte Carlo

Authors: Ronald W. Shonkwiler

2013th Edition

146148510X, 978-1461485100